Visa, MasterCard and American Express have had a firm grip on the global commercial card market for years. While they still maintain that control, China UnionPay, which recently overtook Visa as the world’s top debit card network, is seeing fast expansion of its commercial card program, according to a recent report on the global commercial card market. Should the other networks be worried?

Global commercial card purchase volume has grown considerably, but it has not kept pace with overall card growth as nascent markets such as China also have helped build sizable volume growth in traditional cards, according to a recent Packaged Facts report.

But don’t count China out just yet as a key commercial card player. It’s volumes may be small today in comparison to those of its chief international network rivals, but they’re growing very quickly, the report notes.

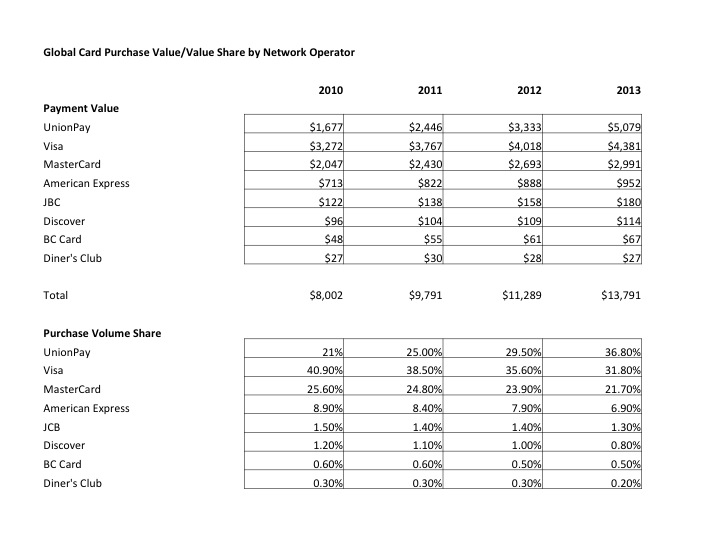

Between 2010 and 2013, global commercial card purchase volume grew 46 percent. Respectable, but not on par with the 72 percent overall card-payment growth during the period. Packaged Facts forecasts global commercial card purchase volume to grow by 13% in 2014 and in 2015, rising to $1.79 trillion from $1.4 trillion in 2013.

The report “Commercial Payment Cards: The U.S. and Global Markets and Trends, 8th Edition” identifies commercial card market size and provides global forecasts through 2015, noting volume share among the leading global networks, which include American Express, BC Card, Diner’s Club, Discover, JCB, MasterCard, UnionPay and Visa.

In many of countries where card programs are nascent, commercial card opportunities are just getting off the ground. Moreover, in China, the market is driven overwhelmingly by consumer debit, the report notes.

Indeed, the combined Visa, American Express and MasterCard commercial card purchase volume comprises 91% of the global total. However, while UnionPay, which has surpassed Visa as the largest global debit card network, is not today a large a commercial card player, its commercial card program is growing rapidly. UnionPay’s commercial payment exploded 263% over just three years, a compound annual growth rate of 53%, and its $61 billion in commercial volume placed it fourth among the world’s major card networks in 2013, according to the report.

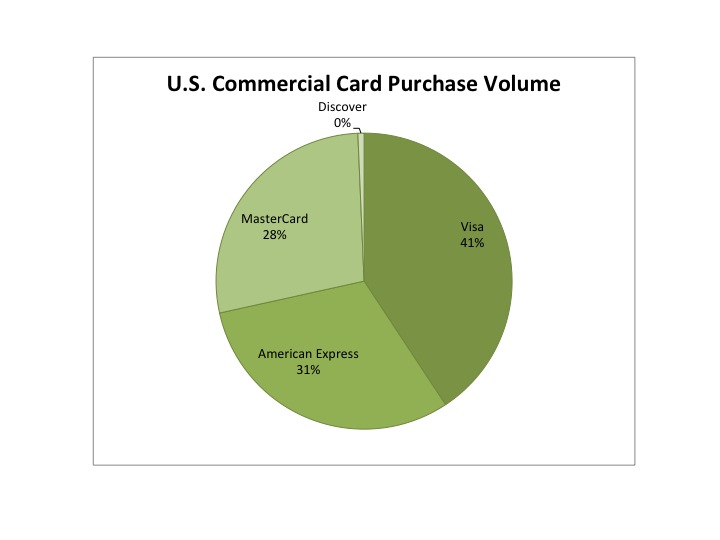

In the U.S., Visa maintains its lead over its three main domestic competitors, as its branded cards generated $362 million in general-purpose commercial card purchase volume in 2013, a 41% share of the U.S. market. MasterCard gained incremental share, as did to a lesser extent American Express.

Debit and prepaid also play important commercial card roles. According to Packaged Facts, in 2013, 18% of the $888 billion in U.S. commercial card purchase volume was generated with debit cards and general-purpose reloadable prepaid debit cards, with debit/prepaid card commercial purchase volume split by an estimated 64% to Visa and 36% to MasterCard.

Visa also is tops in non-U.S. commercial card purchase volume, with a $157 billion 2013 total, representing a 30.4 percent market share. “While its 40 percent 2010-2013 growth put more room between it and American Express, MasterCard closed the gap by growing purchase volume on its network by almost 70 percent,” the report notes.

In 2013, UnionPay had more than $60 billion in commercial card volume, “suggesting that the Chinese market has a growing appetite for this form of payment,” the report noted. Moreover, Diner’s Club maintained volume, as Discover continued to work with Diner’s Club franchisees and upgraded the Diner’s Club network after purchasing it from Citibank.

To address the changing market needs, payments networks and financial institutions must grow along with the world’s large corporations to meet their increasingly global needs, the report points out. “This has undoubtedly caused growing pains, as players struggle to craft solutions sophisticated and robust enough to meet global challenges of many stripes—regulatory and operational hurdles among them,” it notes. “But in plain English, it means expansion—following the arc of global growth and growing products and solutions accordingly.”

As such, major U.S. financial institutions, including Bank of America, Citibank, JPMorgan Chase, Wells Fargo and U.S. Bank appear up to the task, Packaged Facts contends. Moreover, both Visa and MasterCard continue to support such issuers by improving data collection and reporting to meet customers’ requirements.

Besides product and price competition, other key competitive factors in the corporate payments business include global servicing capability, quality of data, and access to additional services, such as reporting and program management tools, the report notes. Other factors include customer experience and the evolution toward payment products that integrate with corporate expense-management tools and support electronic payment methods.

“It also means that payment providers have expanded global issuance footprints and product portfolios by forming partnerships and improving proprietary capabilities,” the report notes.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More