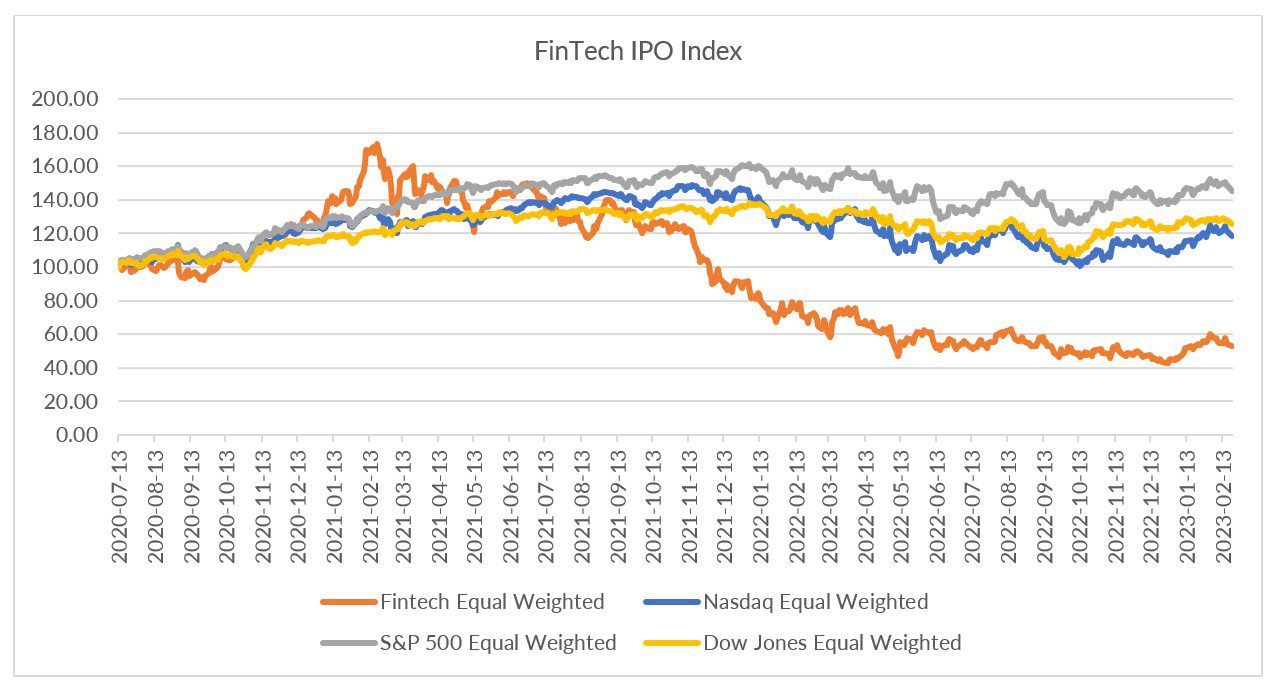

For the FinTech IPO Index, it’s been a long journey — down.

On a day that saw Nasdaq plunge 2.5%, and in a month that brings COVID-19 near the three-year anniversary of being termed a pandemic, it’s worth taking the pulse of how various FinTech “vintages” have done.

No matter how one slices it, it’s been rough sledding. Of the 46 names we track — and even against 2023’s gains of 19% year to date — only three names trade above their offering price.

That means that, loosely speaking, 6.5% of the names have “paid off” in absolute terms if you’d created a basket of equal-weighted holdings.

The flip side of the coin: The vast majority of holdings are, as of this writing, underwater, trading as busted IPOs.

We’ll start with the pantheon of winners first. As of the close of business Tuesday, the non-busted group included: 10X Capital (roughly flat), Bill.com (up 156%) and Futu Holdings (up 200%).

The average post-IPO performance to date, even with the winners baked in? Down more than 53%.

And with some additional detail into how the “classes” have performed: The companies that went public in 2021 are down an average of 64% since their debut. The names that went public in 2020 — right through the darkest days of the pandemic, are off more than 59%. The companies that debuted in 2019 include Futu and Bill.com, as noted above, so the average return here is 7.7%.

The gains seen by Futu and Bill.com bear discussion, and speak to at least a few long-standing trends that certainly have had legs through the past few years. Futu has seen its shares ebb and flow according to sentiment about companies that are a play on China, on the continued demand for online wealth management and online platforms that streamline wealth management. We’ll see more detail when the company reports earnings in the next few weeks. But as reported for the third quarter, the total number of paying clients surged by 24% year over year, and the company’s user base gained 15.6% year on year to 3.1 million.

Bill.com has soared on continued demand for back-end and business automation. That company’s latest results how that revenues were up 66% in the most recent quarter, as measured year over year. And like many other firms, that’s a slowdown from the triple-digit percentage point top line growth that had been measured in previous periods. Of particular note has been demand for accounts payable solutions. The company said that firms using its cloud-based payments platform grew to 182,700, up 35% year over year.

As PYMNTS data has shown, the opportunity is significant for back-end automation. In the AP/AR Quick Start Guide, we found that 28% of SMBs said they had low visibility into cash flow due to back office inefficiencies.

The roster of declining issues, of course, is wide and varied, and double-digit returns so far this year have retraced some losses, but the climb back to IPO break-even will be a long one. There are names, like MoneyLion, that are down 91% from their offer. Robinhood is down 71% since going public. In the latter case, the meme stock phenomenon had been a rocket ship, and then fell back to earth.

Even the names that show the durability of platforms — especially consumer-facing platforms — have been hit hard. SoFi, which is down 71% since its 2021 market debut, has reported a surge in deposits, up 46%, and said that personal loan originations were up 50%. Separately, Nu Holdings, which is more than 50% lower than its IPO price, reported that Nubank added 4.2 million customers in the fourth quarter that ended Dec. 31, to 74.6 million, up 38%. Deposits were up 55% to $15.8 billion.

And the near-term headwinds confronting institutional lending and capital — and worries about consumer spending — are in evidence. Affirm’s a key example here, where the stock is down more than 86% since its IPO. As noted here, for Affirm, a deceleration in consumer demand, and in some cases outright declines in spending on discretionary items, slowed gross merchandise volumes growth rates to 27% in the FY 2023’s second quarter, whereas a year ago, that rate had been 115%. As CEO Max Levchin said on the conference call with analysts, “merchants, and Affirm, are keen on more volume. … We are fundamentally governed by yield and risk management. So we must maintain the risk frameworks that we’ve signed up with our capital partners.”

And as the CEO told investors about what lies ahead, “These are not transactions that will disappear forever, but they’re probably going to remain muted for what we expect is at least a few quarters.”

For FinTech IPO investors, patience is both a virtue — and, perhaps, necessity.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More