The FinTechs are burning through cash.

The capital markets are pulling back.

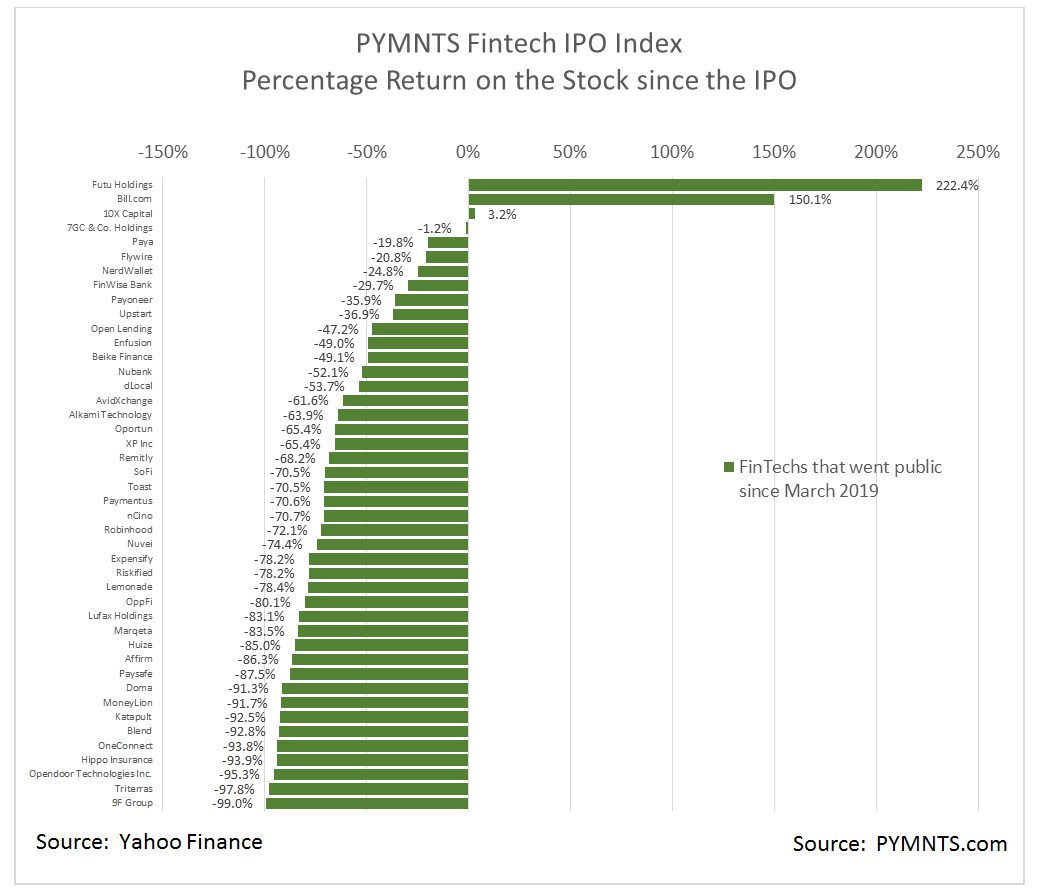

The FinTech IPOs are underwater.

So coming back to Wall Street for more money may be tough sledding.

The FinTechs that have gone public since March 2020, if that is the date — nearly four dozen of them, as tracked each week in the PYMNTS FinTech IPO Index — have had a turbulent time on Wall Street.

If there’s one certainty, it’s that the volatility will continue. And if we look at the “average” metrics of our group — averages are appropriate because the names are equal-weighted — investors are taking a less-than-sanguine view of these would-be disruptors that had promised to ride the wave of the great digital shift.

The average name on our list trades 54% below the offer price. As we have spotlighted before, only two of the names, Futu Holdings (up 222% from the initial offer) and Bill.com (up 150%) are up significantly from their initial public offering. 10x Capital is up 1% from the debut.

We’re also taking the liberty of comparing some other metrics to the general markets. Since many of the names have not recorded net income or don’t have full-year (trailing 12 months) net income under their respective belts, we’ve opted to use price to sales (commonly known on the Street as the P/S ratio). The most appropriate comp here may be the tech-heavy NASDAQ. The NASDAQ, as a whole, sports a P/S ratio of 4.5x as of Tuesday’s trading action. The FinTech IPO group’s P/S ratio is about 3.7x.

The conventional wisdom might be that the FinTech IPO Index and its components are undervalued relative to broader market gauges. But within that discount, we’d note, might be a large dose of investor skepticism over the trajectory of those top lines.

The dollar of market value that investors are willing to pay for a dollar of sales is less, perhaps, because of the perceived risk (it’s the inverse, in a way, of lending: We demand higher interest rates when the perceived risk of the borrower, and the odds of getting our capital back, is less-than-crystal clear).

As for earnings ratios: Only 12 of our names have earnings, and the average is skewed because some names, like Nuvei, have a TTM eps ratio of 75, and others have low single-digit ratios.

Price to sales seems the most apple-to-apples comp here.

The muted valuations may make sense given the fact that, as relayed here, many of the FinTech companies that have gone to the public markets in recent years have been burning through cash — more than $12 billion in last year alone.

Capital has become more expensive amid soaring interest rates. Stripe may be a cautionary tale here, as its valuation declined as it raised capital (reportedly to cover a $3.5 billion tax bill). Its business is notably healthy (i.e., the capital raise is not driven by any operational pressure), and valuations may be less forgiving for FinTechs that have been less tested by the markets and that don’t (like Stripe) process hundreds of billions of dollars in payments volume or generate billions of dollars in top line.

The IPO markets are uncertain at best, so secondary stock listings may be no sure bet.

Our own proprietary data shows that “launched” traditional IPOs year to date in the payments sphere and banking are in the low single digits.

For the FinTech IPO Index, times have been tough, to say the least — and there may not be much relief in the cards.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More