Revolut — a U.K.-based financial technology firm — said Wednesday that it has applied for a European banking license, making it the latest of several digital-only firms looking to compete more actively with larger, traditional lenders.

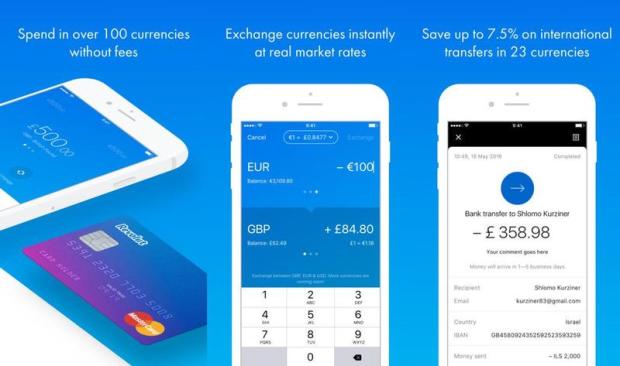

Revolut has been making its prepaid card offering for the last two years. It is now betting on a future in which regulatory changes make it easier for small upstarts like Revolut to compete more actively with more established players. Its playbook resembles that of its fellows in FinTech disruption — customer-friendly apps, lower fees and an instant overview of their finances.

Moreover — coming soon, Britain, as well as a variety of EU players, will see banks forced to open up their vast caches of customer data (something they’ve rather jealously guarded in the past), which startups can leverage to build better targeted products to a more refined customer list.

“Even without a banking license, we have attracted over 950,000 users across Europe, many of whom consider Revolut as their primary current account and spending card,” said Nikolay Storonsky, Revolut’s founder and CEO.

And while Revolut does bill itself as a service “beyond banking,” it has had some difficulty even offering level service with banking — particularly when it comes to current accounts, overdrafts, loans and direct debits. The firm expects it will have a license bestowed in the first half of next year and that it will be able to offer services in select markets straightaway as soon as that certification is granted.

According to the firm, credit will initially be available to users in Lithuania. The service will then travel to Estonia and Latvia as soon as possible — and France, Germany, Italy and the rest of the European Union are all on the menu for the unspecified future.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More