Agnostic is a word that European Payments Council (EPC) Director General Etienne Goosse often uses to describe the mandate of the payments association that counts 2,343 payments services providers, representing about 59% of all EU payment service providers (PSPs), as members.

It is also why he pushes back against repeated calls to regulate adherence to the SEPA Instant Credit Transfer (SCT Inst), he told Karen Webster in an interview. SCT Inst is one of the four distinct payment schemes that the EPC manages, the one that allows payments of up to 100,000 euros (about $117,600) to be made 24/7/365 and received within seconds.

See also: EU Banking Trade Group Presses the Issue on Instant Payments

“[SCT Inst] is an investment that is not insignificant, and for some niche players, there is no business case and there will probably never be a business case,” he said.

That’s in part because other payments schemes work very well for consumers and merchants, including direct debit which EPC also manages, and cards which currently account for 41% of transactions across the EU.

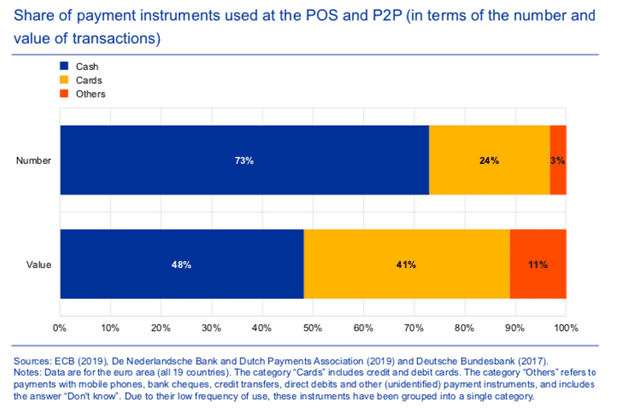

And where cash surprisingly accounts for 78% of all transactions at the point of sale (POS) in an era of digital payments and mobile wallets and nearly half (48%) of the value of those transactions, according to the data published by the European Central Bank in 2020.

Read more: Study on the payment attitudes of consumers in the euro area (SPACE)

In countries like Germany, Spain and Italy, cash remains a popular instrument for in-person retail payments, which hints at the dual challenge of moving consumers to digital payments of any kind at the POS, when cash is also a form of instant payment that consumers trust and use, particularly when paying other people.

Cash Is Still King in Europe

Goosse concurs, pointing to more recent statistics that show that ATM usage is going down as consumers move away from cash for health reasons but also hoard it due to the pandemic’s uncertainty and the tangible store of value that cash represents.

In some countries, Goosse said, consumers aren’t interested in instant payments except if they must make a payment urgently and digital rails are more accessible and convenient. With greater value also comes the potential to monetize instant by those banks and PSPs.

He acknowledged that banks have been implementing SCT Inst differently depending on the opportunity to monetize instant payments.

See also: European Payments Council Seeks Help in Tracking Fraud

Goose said since SCT Inst requires both a technology (from batch to instant) and process change for banks and their business customers, not everyone can or will want to invest to support it unless and until there is evidence that more consumers will embrace it and want to use it. Currently, Goosse said that nearly 10% of EU transactions are done over SCT Inst rails.

Beyond the Ivory Tower

Goosse said in the past, the EPC has been accused of operating in “an ivory tower,” directing the way payments should be made. But “like war, it’s important it’s left to generals,” which is what the association has done to carry out its mandate successfully.

“[The EPC] does things that we believe have market value and provide value to the players and the end users at the end, but they choose, the banks choose, and the PSPs choose,” he said.

Goosse emphasized that the EPC has no intention to pit two instruments against one another —direct debit and SCT Inst — because “that’s not our role; it’s for the market to decide what they use.”

Getting more merchants to see the need for a centralized instant payment solution can help move closer to the goal, and involving these small businesses up front in the entire process will be key. It’s also where he said that the EPC and the European Payments Initiative (EPI) can learn from open banking regulations, compliance with which has been pushed out several times, now to March 2022.

Banks had to develop PSD2 base functionalities without being remunerated, so they need a business case beyond PSD2, Goosse said. And with remuneration on the table, developing a harmonized scheme for functionality requirements beyond PSD2 is within reach.

“That’s why it’s in the interest of both third-party payment service providers (TPPs) and traditional PSP banks to agree on, which hasn’t been the case for PSD2,” he said.

The EPC has also been active in tackling fraud, after noticing a rise in payments fraud and scams. In April, it issued a request for proposals seeking “a reliable independent service provider” to whom it will outsource the maintenance and management of a new malware information sharing system (MISP) for the SEPA. The MISP is scheduled to go online by February 2022 after three months of pilot testing.

Not Taking Sides

Goosse said the EPC has an informal relationship with the EPI, an initiative launched by eurozone banks to create a unified Europe-wide payments system that can take on card networks like Mastercard and Visa.

Some of the schemes created by the EPC, like SCT Inst and the SEPA Request-to-Pay (SRTP) Scheme, could be of interest to the EPI, “but we are agnostic again,” he noted, adding that the EPI is a solution like any of the several others already using SCT Inst on the market.

“We don’t want to be seen siding with one,” he said. “We are already universal; we have no preference toward anyone, only [toward] the market. We want to listen to the market and satisfy the market, but not one specific market player.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More