Payments choice is the key to unlocking more transactions for more merchants and brands both online and in-store, and choice means trying new digital experiences — the forté of adventurous millennials, a group with the highest payments diversification of all.

For the “Digital Economy Payments June 2022 U.S. Edition: Payment Method Diversification,” PYMNTS surveyed over 2,770 U.S. consumers to explore payments diversification among various demographic groups to gain insights into how merchants must innovate accordingly.

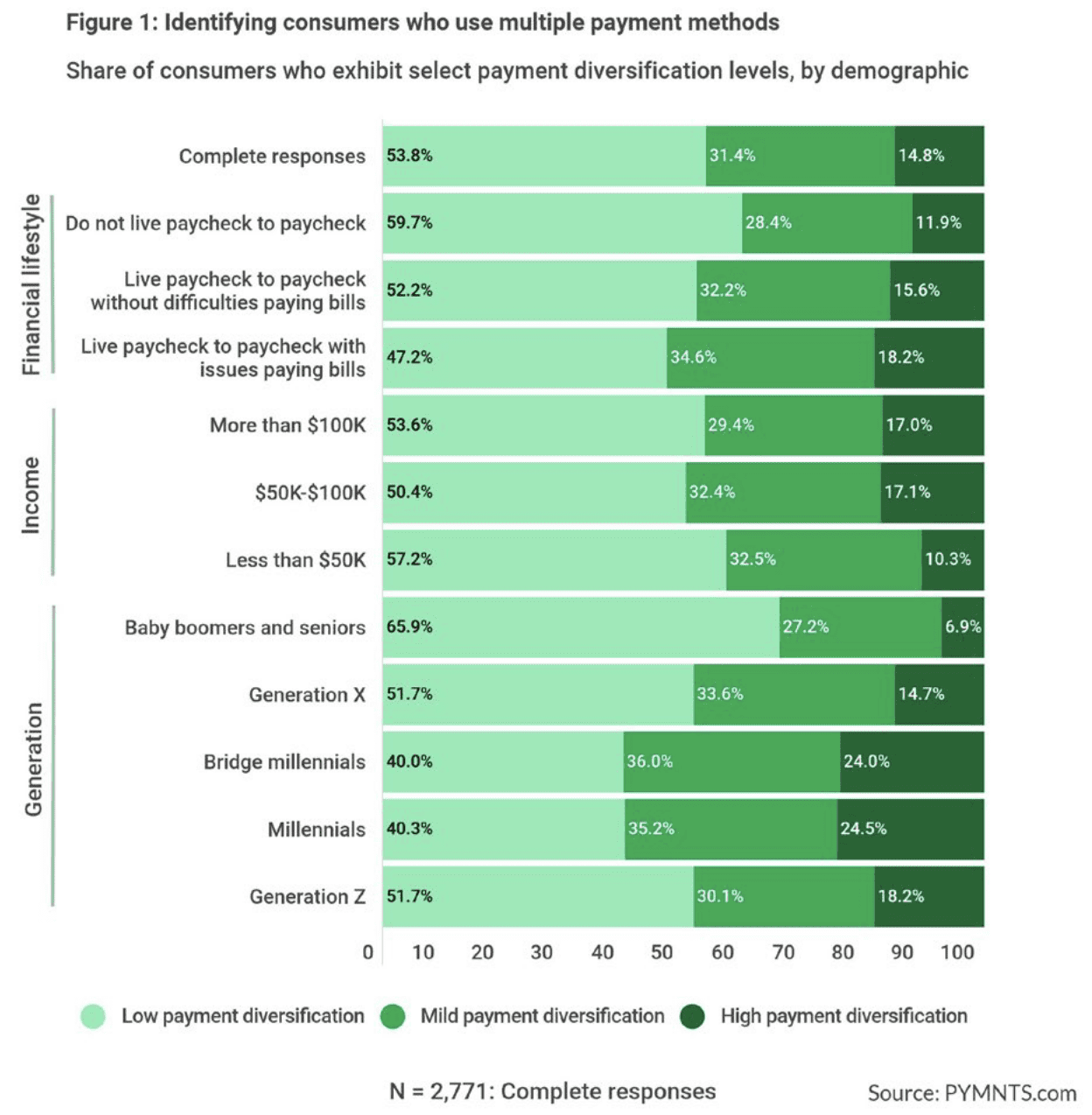

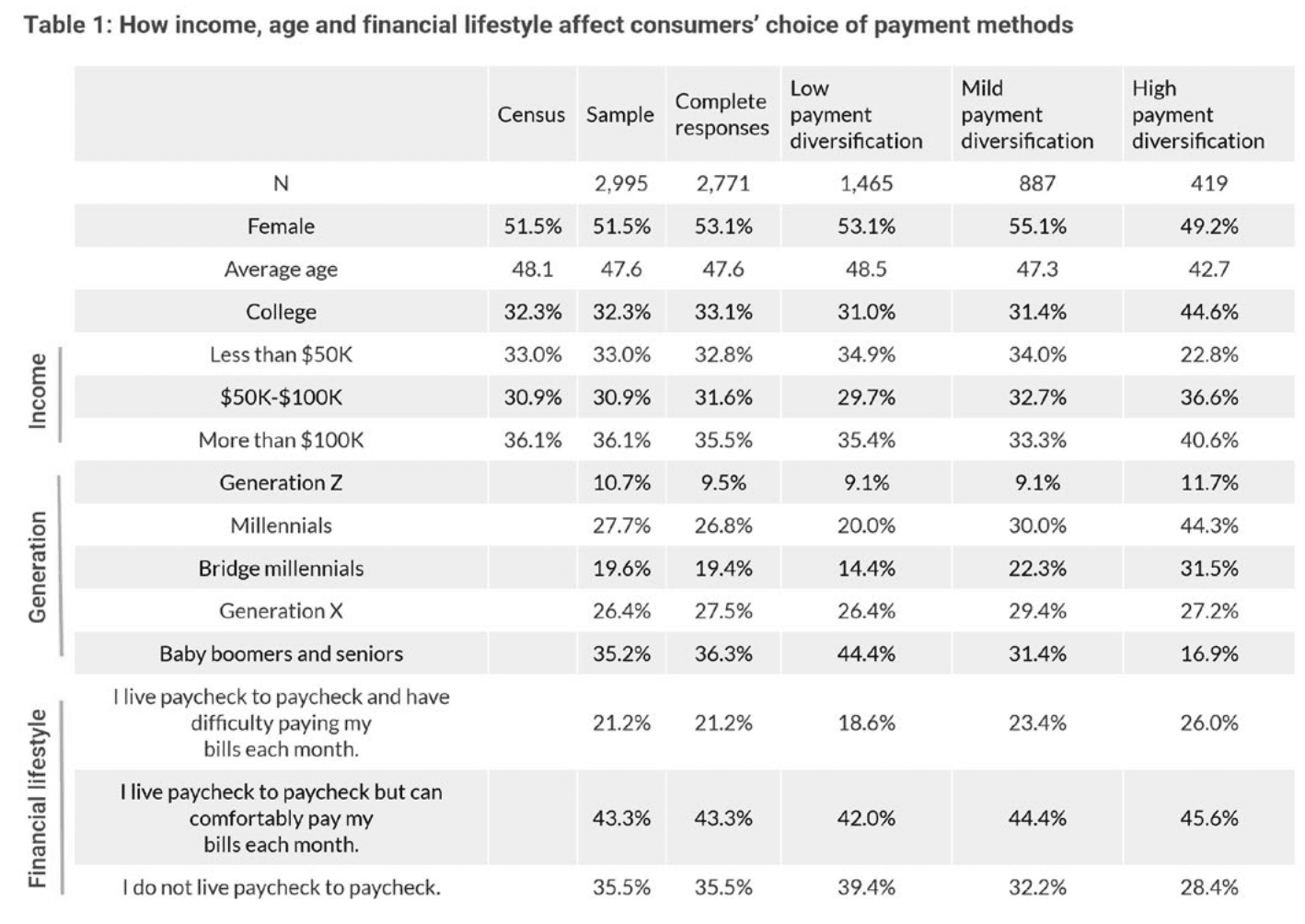

To understand how different demographics define “payments diversification,” we categorized respondents based on the number of payment types used, ending up with three groupings.

High Payments Diversification (HPD) consumers are using at least three payment types, two of those being nontraditional forms like digital wallets, crypto or buy now, pay later (BNPL). Moderate Payments Diversification (MPD) consumers are using at least two payment methods, at least one of which is nontraditional, and Low Payments Diversification (LPD) consumers are generally using one payment method, “even if it is a nontraditional method such as PayPal.”

We found a strong correlation between age group and HPD. Per the study, “With 25% of millennials having HPD, they have the most payment diversification of any age group. Just 15% of overall consumers are considered HPD.”

“PYMNTS’ data shows that a consumer’s age and financial lifestyle are the strongest factors influencing their level of payment method diversification,” per the study. “After the 25% of millennials who exhibit HPD, Generation Z and Generation X have the next highest concentration of HPD consumers, at 18% and 15%, respectively. Just 6.9% of baby boomers and seniors are HPD consumers.”

Get your copy: Digital Economy Payments June 2022 U.S. Edition

Mobile Markers

Setting HPD consumers apart from cohorts using fewer payment types in their daily lives is their mobile shopping behavior, which is well ahead of other groupings we studied.

The research shows that 26% of HPD consumers made a mobile online purchase during their most recent non-grocery retail shopping excursion, as compared to 17% of MPD consumers and 10% of LPD consumers who did the same.

An interesting (though not unexpected) finding is that “HPD consumers also tend to purchase a greater variety of products when shopping with retailers for goods other than groceries,” with 47% of HPD consumers shopping across two or more product categories, “significantly exceeding the 26% of MPD consumers and 21% of LPD consumers that do the same.”

The Issues of HPD

The Issues of HPD

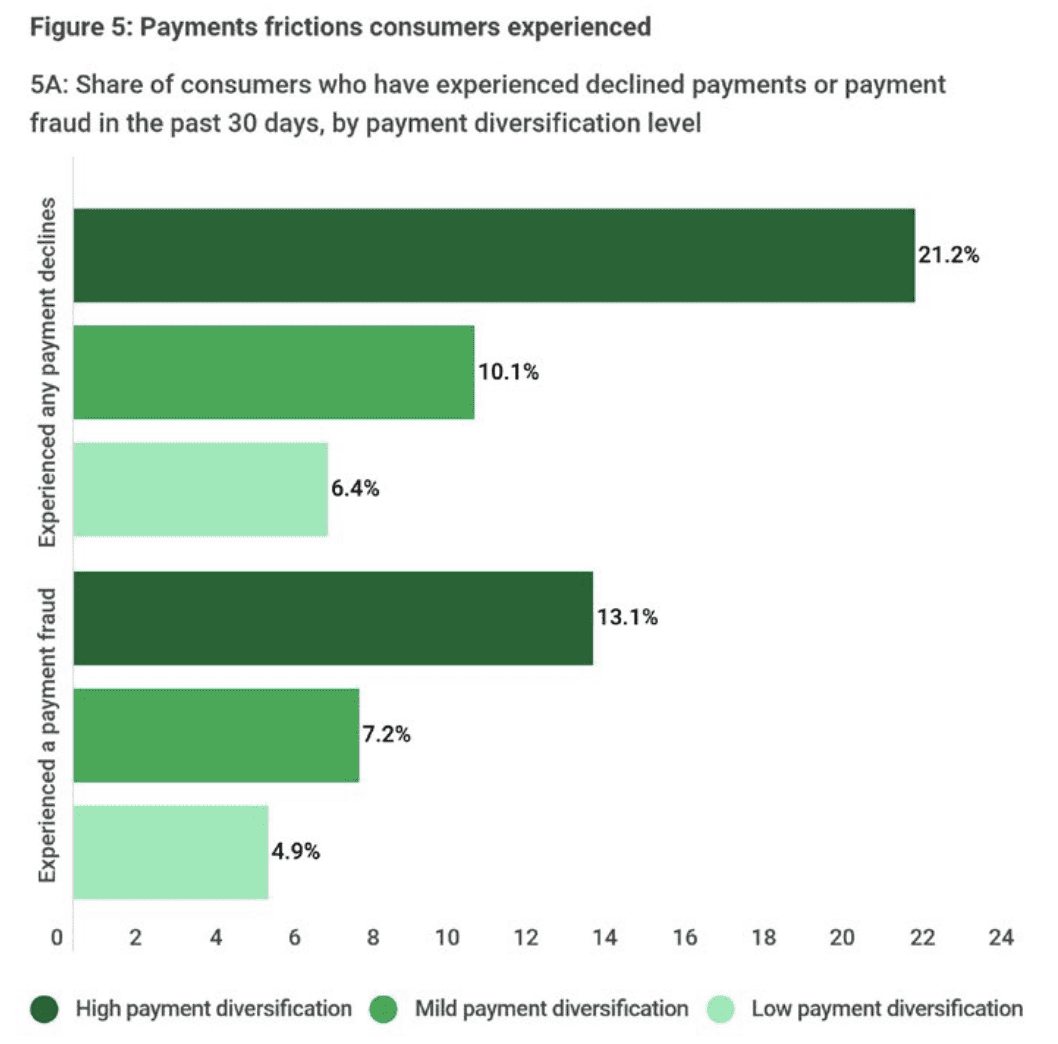

If there’s a downside to payments diversification, it’s that the more methods one uses to pay, the more likely they are to encounter declines that attend every payment type.

The study found that 21% of HPD consumers had payments declined in the past 30 days, and that 13% victims of payments fraud, although these were not the overriding reasons for HPD declines.

Reasons tend to be more pedestrian, as the study stated that “36% of HPD consumers had a payment declined because incorrect information was entered at the checkout, yet just 14% of MPD consumers and 16% of LPD consumers had this happen.”

See it now: Digital Economy Payments June 2022 U.S. Edition

See it now: Digital Economy Payments June 2022 U.S. Edition

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More