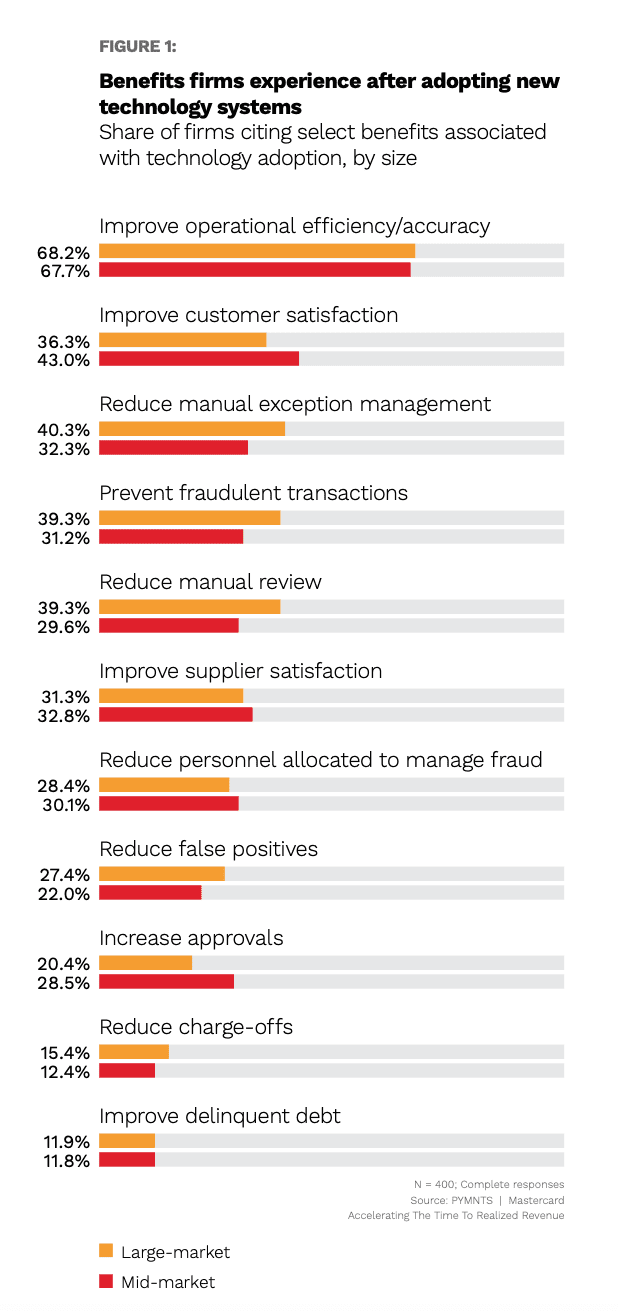

Adopting the latest digital payments innovations can help firms keep their businesses operating smoothly while also benefiting business relationships. Not only do 68% of firms say that digital payments innovations have improved their operational efficiency, but 40% say it has improved customer satisfaction and 32% say it has improved supplier satisfaction, according to Accelerating The Time To Realized Revenue, a PYMNTS and Mastercard collaboration.

Get the report: Accelerating The Time To Realized Revenue

While both large and mid-size firms benefit from digital innovation, they expect different key benefits from adoption of digital payments innovations.

Mid-market firms say digital innovation has had an especially marked impact on their relationships with their buyers and suppliers. Among these firms, 43% say innovation has improved their customer satisfaction, and 33% say it has improved their supplier satisfaction.

Large-market firms tend to report more improvement in their anti-fraud operations than mid-market firms. For example, 39% of large-market firms report observing fewer fraudulent transactions after adopting digital innovations, and 27% said they see fewer false positives.

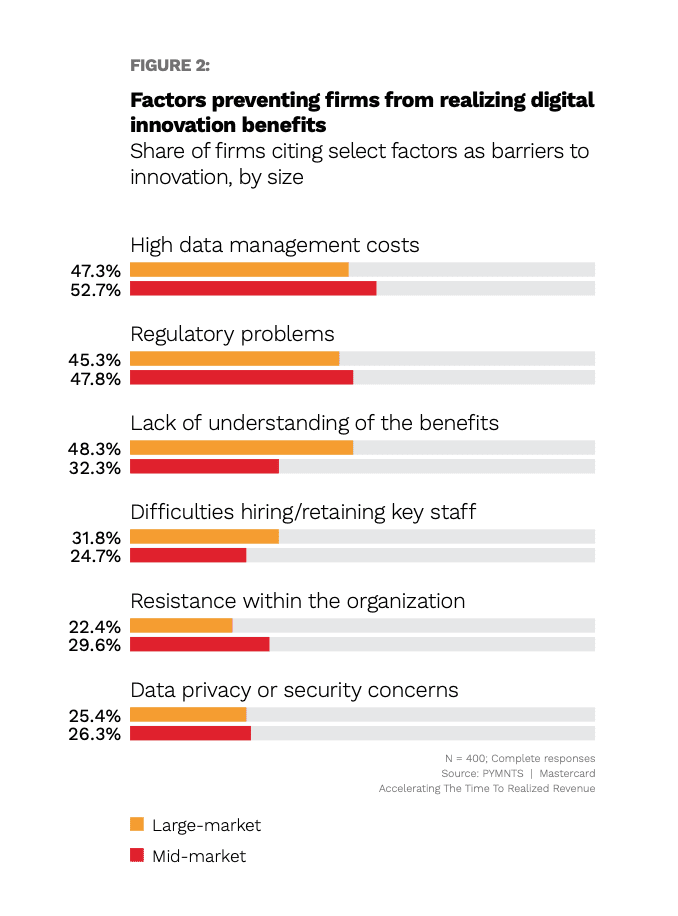

Despite the benefits digital innovation has to offer, several key factors stop firms from embracing digital payment innovations.

Higher data management costs and regulatory barriers are at the very top of the list of factors holding back the innovation efforts of mid-market firms. Fifty-three percent and 48% of mid-market firms say data management costs and regulatory barriers are hindering their innovation efforts, respectively.

For large-market firms, the most pressing issue is a general lack of understanding about how innovating digital payments operations might improve their businesses. Forty-eight percent of large-market firms cite a lack of knowledge about innovations’ benefits and limitations as a key barrier hindering their innovation plans.

Large-market firms also struggle with high data management costs and regulatory problems, though to a slightly lesser degree than mid-market firms.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More