Powered By Dosh is a solution that enables financial services companies to provide card-linked, cash-back experiences to customers. It is executed via a software development kit (SDK), web application and personalization engine.

According to the company, several financial services companies will launch with Dosh this fall. Venmo is already live, and the neobank Jelli will launch later in August.

“As consumers turn to the brands and payment options that provide the biggest rewards, financial institutions, neobanks and payment providers want to stay top-of-wallet by providing a world-class, frictionless, cash-back program,” said Ryan Wuerch, CEO and founder of Dosh. “The Dosh platform has found the sweet spot for merchants, financial services companies and consumers alike. Since launch, the demand for the Powered by Dosh technology from financial services companies, both big and small, has been incredible. We will announce new partners over the coming months, which will expand our user base to over 60 million.”

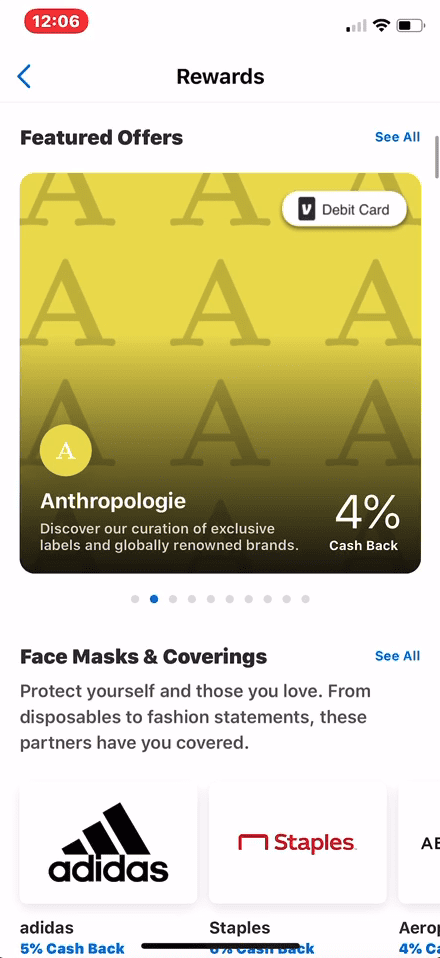

As Wuerch told PYMNTS, the Dosh app-based solution has been in use by many retailers, including Walmart, Sephora, Dunkin and Finish Line. Here’s how it works for a retail purchase from a consumer perspective. Suppose a 30-something woman in Austin, Texas has downloaded the Dosh app, which she has linked to a Mastercard. She’s shopping for eye makeup. Checking the app, she sees that Sephora is a participating retailer, because Sephora has contracted with Dosh to advertise the location within the app. She goes to Sephora and pays for her $30 purchase with the card. Sephora, which is funding the cash-back offer, sends $5 to her Dosh mobile wallet. If the shopper chooses to make an online purchase from Sephora.com, the same process takes place.

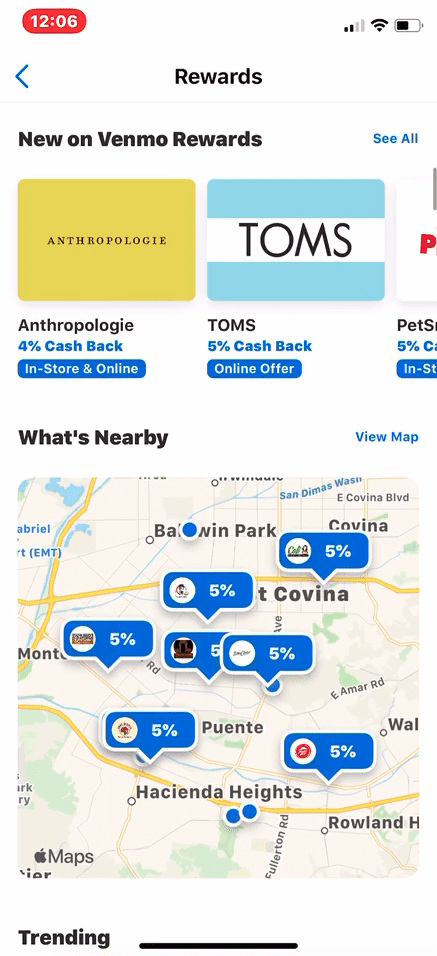

If the shopper was using Venmo, the process would be slightly different. Because Venmo has the arrangement with Dosh instead of the retailers, the shopper would open Venmo and see a map of participating Dosh retailers, and would be served additional personalized offers based on location and purchase history. In this case, if the purchase was made with Venmo at Sephora, the cash-back would go right to Venmo, not the Dosh app.

According to Dosh’s research, 80 percent of consumers say they would visit a store they hadn’t tried before if alerted about cash-back offers. The company also claims that card-linked offers will attract younger consumers. Seventy-four percent of Gen Z and 70 percent of millennials will spend more money if they know they will receive cash-back at checkout, Dosh says.

For the expansion, Wuerch noted that Dosh is already working with PayPal, Mastercard, Visa and American Express on both the retail and financial service sides. While retailers have seen increases in overall engagement and spend, he also feels confident that Dosh will allow them to spend advertising dollars more efficiently, as retailers can tie their ads and purchases to the app.

“The pandemic has shifted all the norms,” Wuerch said. “It has accelerated the trend of merchants moving to transaction-based advertising. Merchants need results today. In particular, within the in-store environment, merchants need customers coming back with frequency. In an online environment, they need to be able to differentiate themselves, so that the consumer is moving their dollars to their brand versus another.

“To do this, they need to be efficient with their ad spend, and I think that’s what that our platform does,” Wuerch continued. “We have created a transaction-based advertising platform that enables merchants and brands to move those dollars that historically had gone into other media, where there’s hardly any attribution.”

Dosh, the company that bills itself as the fastest-growing cash-back, card-linked offer platform, is expanding its retail-based solution to the financial services business. The announcement represents an ambitious extension for the Austin, Texas-based FinTech, which is launching the new “Powered By Dosh” capability with Venmo as well as other companies.

Dosh, the company that bills itself as the fastest-growing cash-back, card-linked offer platform, is expanding its retail-based solution to the financial services business. The announcement represents an ambitious extension for the Austin, Texas-based FinTech, which is launching the new “Powered By Dosh” capability with Venmo as well as other companies.