Account-to-account (A2A) payments do just what the name implies: transfer funds between bank accounts in near real time. These payments have gained traction in recent years — used by 36% of consumers in the past quarter — but have yet to fully disrupt the wider payments landscape.

Our data reveals that peer-to-peer (P2P) payments account for most A2A transactions. P2P payments, such as those conducted on Venmo, predominate across the A2A landscape for U.S. consumers. However, additional use cases, such as merchant transactions and bill payments, should not be ignored. With 14% of respondents using A2A methods to pay bills and subscriptions, A2A payments are emerging as a versatile financial option. Notably, 40% of survey respondents expressed a willingness to adopt A2A payments, suggesting opportunities for further market penetration.

Our data reveals that peer-to-peer (P2P) payments account for most A2A transactions. P2P payments, such as those conducted on Venmo, predominate across the A2A landscape for U.S. consumers. However, additional use cases, such as merchant transactions and bill payments, should not be ignored. With 14% of respondents using A2A methods to pay bills and subscriptions, A2A payments are emerging as a versatile financial option. Notably, 40% of survey respondents expressed a willingness to adopt A2A payments, suggesting opportunities for further market penetration.

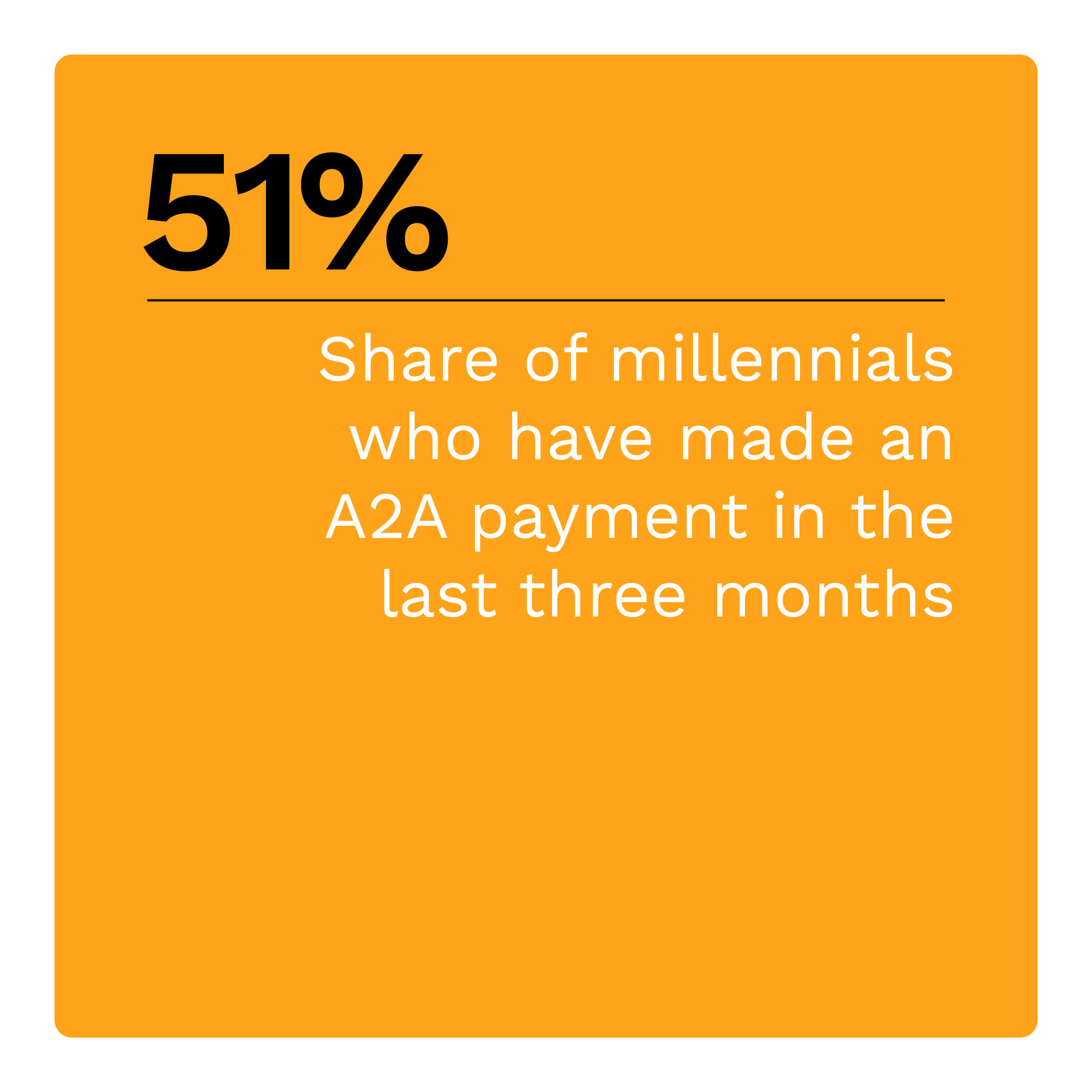

Understanding consumer preferences and barriers is crucial for the payments industry as digital payments continue to evolve. A2A providers need to be particularly sensitive to generational preferences.

These are some of the key findings in “Tracking the Digital Payments Takeover: Consumer Familiarity Controls Account-to-Account Payment Growth,” a PYMNTS Intelligence and AWS collaboration. In this edition we surveyed 3,331 U.S. consumers between Aug. 25 and Aug. 31 to discover how they use A2A payments and what drives them to choose this method over others.

Other key findings from the report include:

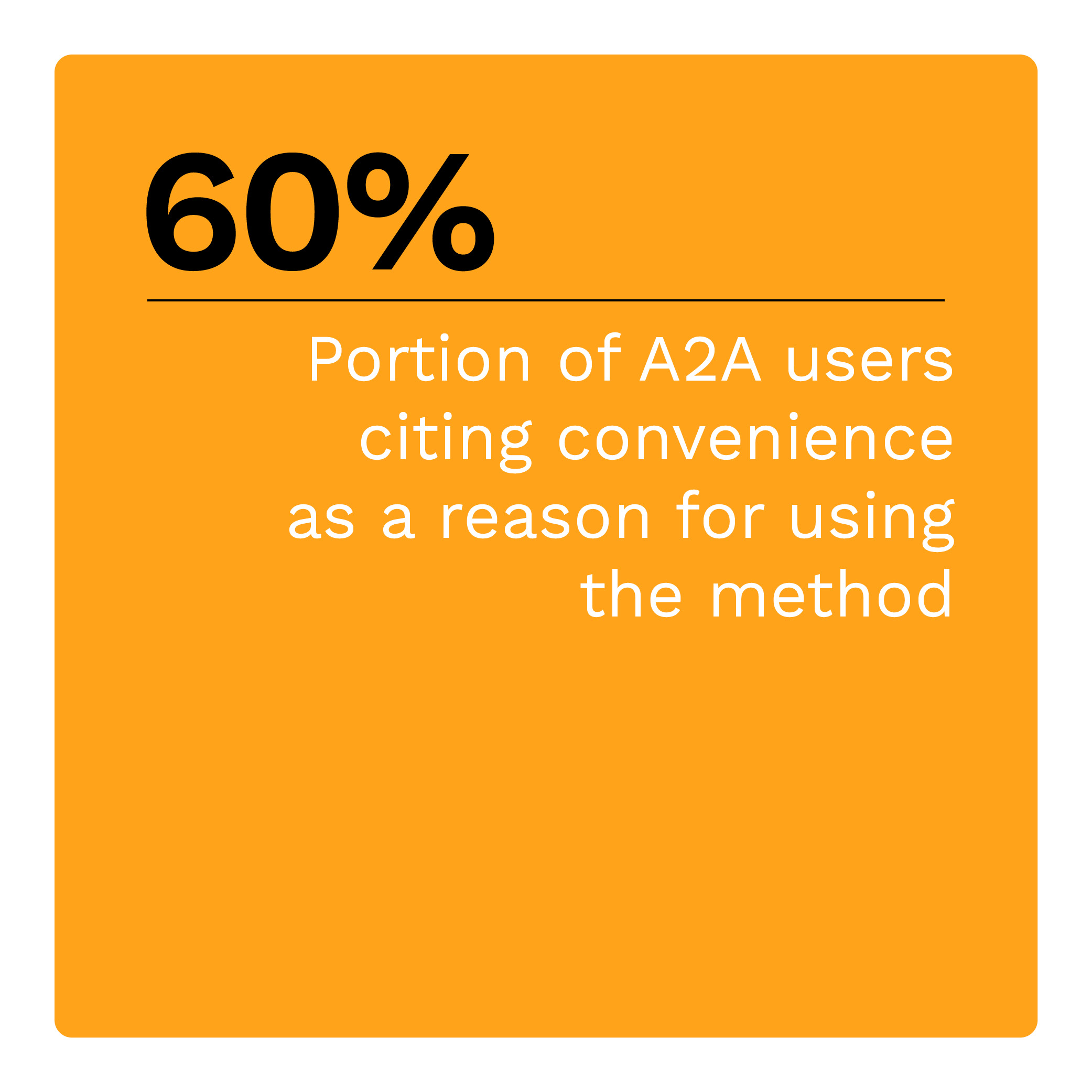

Consumer Satisfaction With A2A Payments is Sky-High

Ease of use and convenience drive remarkably high satisfaction levels with A2A payments, particularly for P2P transactions. At least 8 in 10 A2A users express satisfaction with their go-to A2A platform. More than 60% cite “convenience” as a key factor. These platforms’ success in making the payment experience seamless and part of an ecosystem where users frequently interact and transact helps explain these high satisfaction levels.

Consumer Knowledge Gap Hinders Adoption

Despite consumer enthusiasm, lack of familiarity with A2A payments remains the primary obstacle to wider adoption. Thirty-six percent of consumers admit they do not know how these payments work. Another 24% are unaware these options exist. This knowledge gap is particularly pronounced among baby boomers and seniors — though a sizeable portion of Generation Z consumers say the same. These facts offer a clear avenue for targeted educational campaigns.

Despite consumer enthusiasm, lack of familiarity with A2A payments remains the primary obstacle to wider adoption. Thirty-six percent of consumers admit they do not know how these payments work. Another 24% are unaware these options exist. This knowledge gap is particularly pronounced among baby boomers and seniors — though a sizeable portion of Generation Z consumers say the same. These facts offer a clear avenue for targeted educational campaigns.

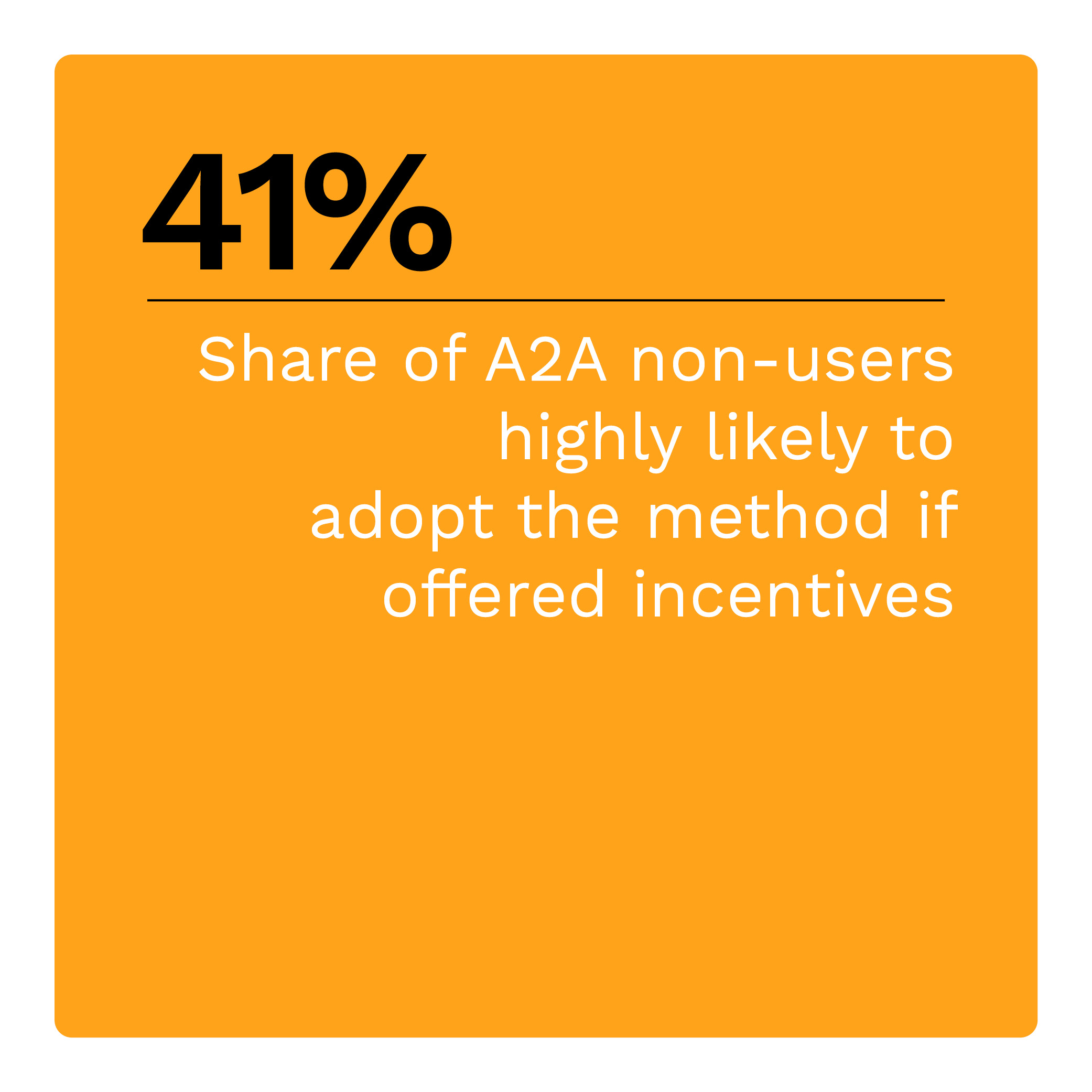

Incentives Could Be a Game Changer for A2A Payments

The potential for incentive-driven adoption is significant. About 41% of consumers who have not used A2A payments in the last 90 days are open to trying them if offered incentive programs. Cashback, discounts and rewards top the list of most desirable incentives, offering FinTechs and financial institutions a strategic lever to encourage A2A adoption.

Despite the convenience and speed that A2A payments can provide, adoption and use are relatively low. To drive additional adoption, A2A providers still need to overcome hurdles, in particularly the knowledge gap, to continue to drive adoption. Download the report to learn more about how and why U.S. consumers use A2A payments and what providers need to know to continue to drive adoption.