They call it “pig butchering.”

A scammer spends time getting their victim’s confidence and trust to convince them to set up cryptocurrency accounts in an effort to eventually steal their assets.

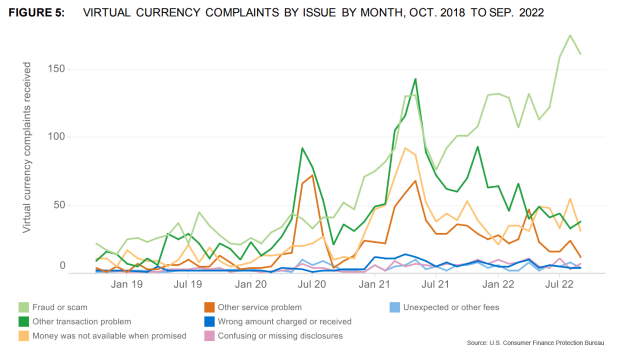

And as the U.S. Consumer Finance Protection Bureau said Thursday (Nov. 10), it’s one of the more notable forms of scams affecting cryptocurrency users.

“Our analysis of consumer complaints suggests that bad actors are leveraging crypto-assets to perpetrate fraud on the public,” said CFPB Director Rohit Chopra. “Americans are also reporting transaction problems, frozen accounts, and lost savings when it comes to crypto-assets. People should be wary of anyone seeking upfront payment in crypto-assets, since this may be a scam.”

Between October 2018 and September 2022, the CFPB received more than 8,300 complaints related to crypto-assets, most of them in the last two years. In about 40% of crypto-asset complaints handled since 2018, consumers said frauds and scams were the main issues.

“Hacks by malicious actors have marred crypto-assets, and led to significant financial loss by consumers with no recourse for recovering stolen funds,” the CFPB said.

Beyond hacks, the bureau pointed to other risks, such as romance scams, fraudulent transactions and greater market volatility.

PYMNTS wrote recently that crypto hacks have cost users $3 billion in the first 10 months of 2022, with hackers stealing $730 million in October alone.

With decentralized finance or DeFi, as these hackers’ prime target, it’s becoming a big enough threat that Chainalysis, which monitors cryptocurrencies, might have jumped the gun in calling 2021 “The Year of the Hack.”

“What is unique that’s happening lately in the crypto space is the rate at which hacking is growing,” said Kim Grauer, head of research for Chainalysis, told PYMNTS’ Karen Webster.

“It was the fastest growing subtype of crime out there of any type of crime we track — and we track many — and we had predicted that that was going to subside in the short term to medium term because it simply had to, to build trust in the industry.”

However, Grauer added, “that’s not what we’ve been seeing,” with this year on track to surpass 2021’s record $3.2 billion in stolen crypto funds.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More