Merchants, card issuers and banks are no strangers to facing off against evolving fraud threats. Debit-related fraud is a particular concern for businesses and banks as failing to thwart such schemes could have significant and costly consequences. Recent studies have found that debit issuers lost approximately $1 billion to fraudsters targeting transactions at the physical POS or ATMs in 2019 — and this was before the ongoing pandemic expanded fraudsters’ opportunities to launch their schemes.

The pandemic has driven consumers to make the bulk of their purchases online, leading many businesses and retailers to struggle with securing their digital infrastructures and payments processes while managing floods of orders. These systems’ overloads have consequently given fraudsters ample opportunities to perpetrate their schemes, with one report finding that 83 percent of the top 30 U.S. retailers have digital oversights that leave them vulnerable to attacks.

This digital shift coincides with consumers’ growing trend toward using debit cards for eCommerce as well as for brick-and-mortar purchases. Eighty percent of consumers now prefer using debit cards for everyday transactions, including those using the mobile wallet and contactless payment solutions that have grown more popular since the pandemic began. One recent PYMNTS study found that 28 percent of millennials now consider themselves debit-centric users, indicating that debit use is also strong among younger generations. Ensuring that robust fraud protections are in place to safeguard debit transactions is thus growing increasingly important for businesses, financial institutions (FIs) and issuers.

The following Deep Dive examines how the ongoing pandemic has affected consumers’ debit use online and in stores as well as how it has altered fraudsters’ strategies when targeting debit transactions. It also analyzes how retailers, debit issuers and other payment players can sharpen the tools they use to keep debit fraud in check.

Debit And The Fraud Catch

The shift to debit has been underway for some time, with one study finding that consumers made roughly 77 billion debit transactions in 2019, for example. The number of debit purchases consumers make monthly is also creeping upward, the report noted, with customers using debit about 25 times each month, on average, during the same year. These habits extended into 2020, but with a pandemic-driven twist: CNP transactions, including those made using contactless payment methods, skyrocketed. One report even found that about 40 percent of consumers’ debit-related goods purchases were made online compared to 32 percent in 2019.

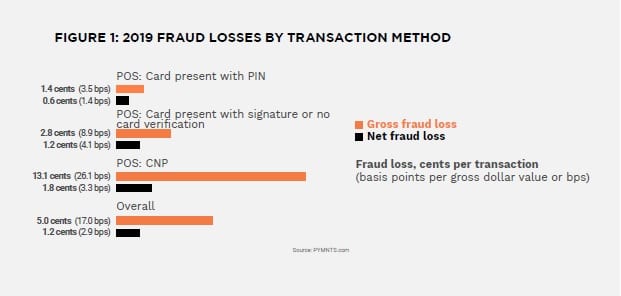

Card-not-present (CNP) transactions can sometimes carry more risks than in-person purchases, however, because they often bypass traditional security measures, such as PINs. Card-present fraud at the physical POS cost businesses about 1 cent in net fraud per transaction in 2019, for example, compared to the 13 cents in net fraud cost for CNP transactions during the same year.

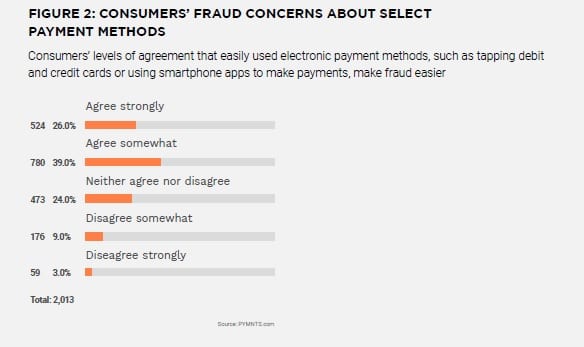

Consumers are continuing to choose debit over credit in higher numbers, but some are also concerned about being adequately protected when making online transactions. Another study found 16 percent of Canadian consumers “strongly” agreed that they would not use their debit cards at unknown merchants due to trepidations regarding potential fraud. The share of those troubled by the prevalence of debit-focused scams is higher when these cards are attached to contactless payment methods, such as tap-and-go cards, with 26 percent of consumers surveyed stating that they “strongly” agreed that being able to use these methods easily could put transactions at risk for fraud. A PYMNTS study on U.S. consumers found a significant number of individuals are interested in digital features that can protect their debit cards from fraud. Seventy-three percent of consumers stated an interest in mobile card apps that allowed them to report lost or stolen debit cards, for example.

This means that retailers, debit issuers and FIs now face a conundrum: Ensuring quick, easy debit payments is becoming key to keeping consumers’ trust and business, but firms must do so without unwittingly exposing payment details to fraudsters. Businesses and payment players must therefore reconfigure or reimagine the anti-fraud strategies they use to protect debit — especially when it comes to online transactions.

New Year, New Fraud Protection Strategies

Consumers’ shift toward debit is likely to continue even after the pandemic ends, and FIs and businesses must adopt fraud protection strategies to safeguard debit to stay competitive in an increasingly crowded eCommerce market. Customers’ evolving shopping and spending behaviors necessitate fraud protection solutions that are flexible enough to dispel fraud across numerous channels.

Adopting new technologies that can give entities holistic looks at the risks associated with new payment solutions or help them more quickly verify consumers’ identities can enable them to keep these transactions safe. Tools such as data analytics and automation that can be broadly applied — and make use of a wider range of data — could be essential to the future of debit-related payments. They could help retailers and banks develop better understandings of how consumers are making transactions. Knowing precisely how legitimate users are tapping debit could allow merchants to build out more robust profiles of legitimate users, making it easier to identify fraudsters and oust bad actors from their platforms.