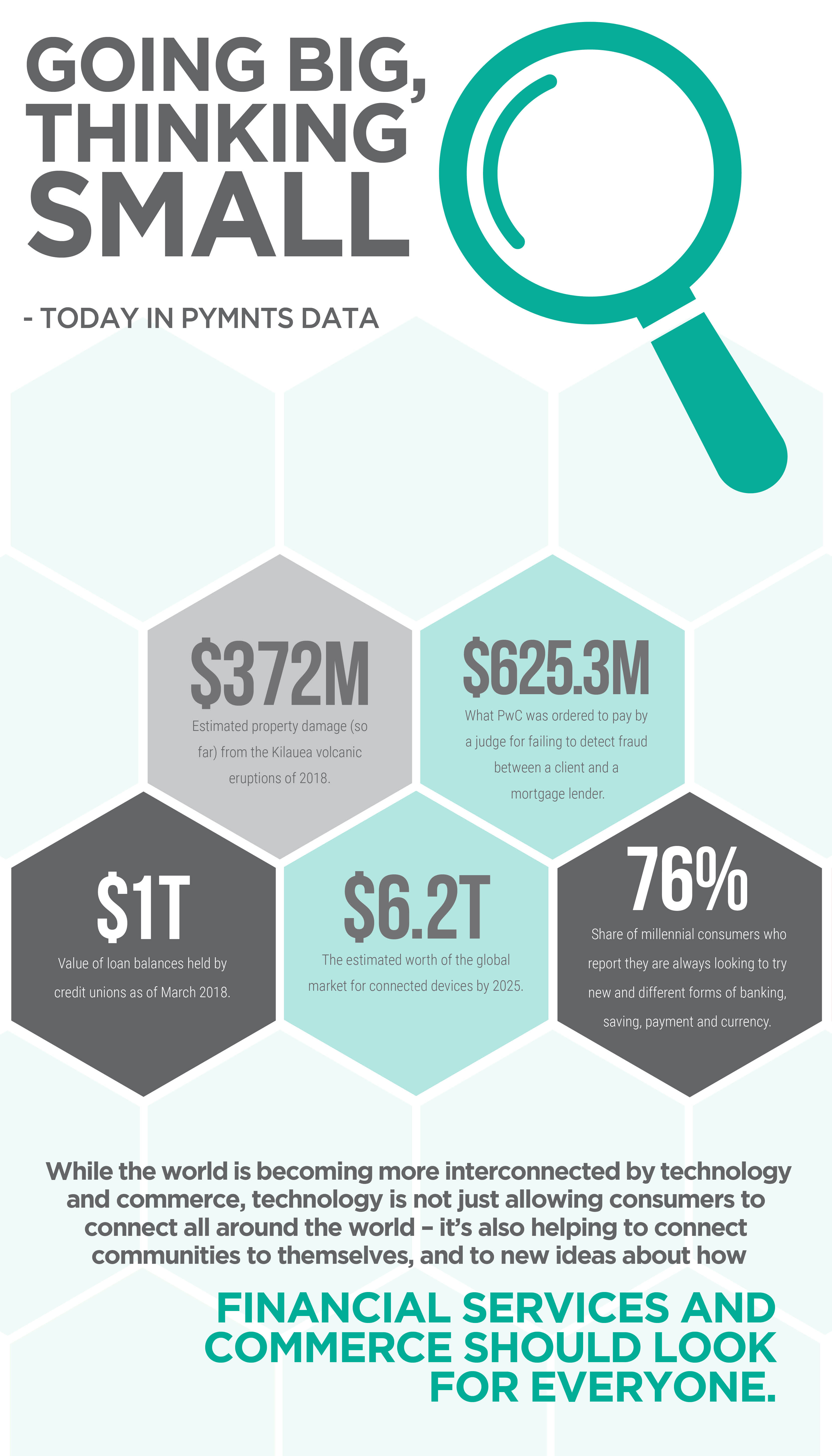

Today In Data: Going Big, Thinking Small

The marketplace of 2018 and its many opportunities are the favored fodder for optimists in the digital age. But a fast-growing world is a challenging one – particularly with fraudsters always waiting in the wings to make the costs of failure very high for those who fail to upgrade adequately. And as the world gets more connected – which it will – the opportunities for fraudsters to break into those connections only become more numerous. But for all the undeniable risks, the rewards are numerous and perhaps unexpected, as a more connected world is also allowing community-based organizations like credit unions to connect more closely and credibly with their growing consumer base.