The PYMNTS Intelligence report “What Credit Card Outsiders Want — and How FIs Can Bring Them Back” explored the financial products that appeal to “credit card outsiders” — those who have never owned a credit card or have let their cards lapse. The report showed how financial institutions (FIs) can re-engage these groups by providing personalized solutions, particularly secured cards, to rebuild trust and accessibility in the credit market.

Understanding the Credit Needs of Outsiders

According to the report, 62% of credit card outsiders used at least one type of credit product, and store cards and buy now, pay later (BNPL) plans were the most popular. These alternatives to traditional credit cards suggest outsiders prefer accessible, short-term credit solutions. Among outsiders, the most prevalent groups — second chancers (those who previously had a credit card and wish to re-enter the market) and the credit curious (those interested in credit cards but have never had one) — were inclined toward store cards and BNPL.

The preference for these products indicates a demand for flexible, low-commitment credit options. Additionally, outsiders with low credit scores were more likely to rely on these alternative products, suggesting a need for FIs to develop offerings that accommodate various levels of creditworthiness.

Identifying the Most Attractive Credit Solutions

Secured cards were the most sought-after product among credit card outsiders, with 29% expressing interest. Traditional credit cards followed closely behind at 28%. BNPL services, which appeal to those looking for immediate access to credit without long-term commitments, checked in at 27%. These findings show a preference for products that provide immediate use and flexibility.

Secured cards were the most sought-after product among credit card outsiders, with 29% expressing interest. Traditional credit cards followed closely behind at 28%. BNPL services, which appeal to those looking for immediate access to credit without long-term commitments, checked in at 27%. These findings show a preference for products that provide immediate use and flexibility.

The interest in secured credit cards among second chancers and the credit curious shows that these groups are open to re-engaging with traditional credit products, provided they can meet their short-term needs. For financial institutions, prioritizing short-term credit solutions like secured cards or BNPL could prove effective in drawing these consumers back into the credit market.

Overcoming Obstacles to Credit Access

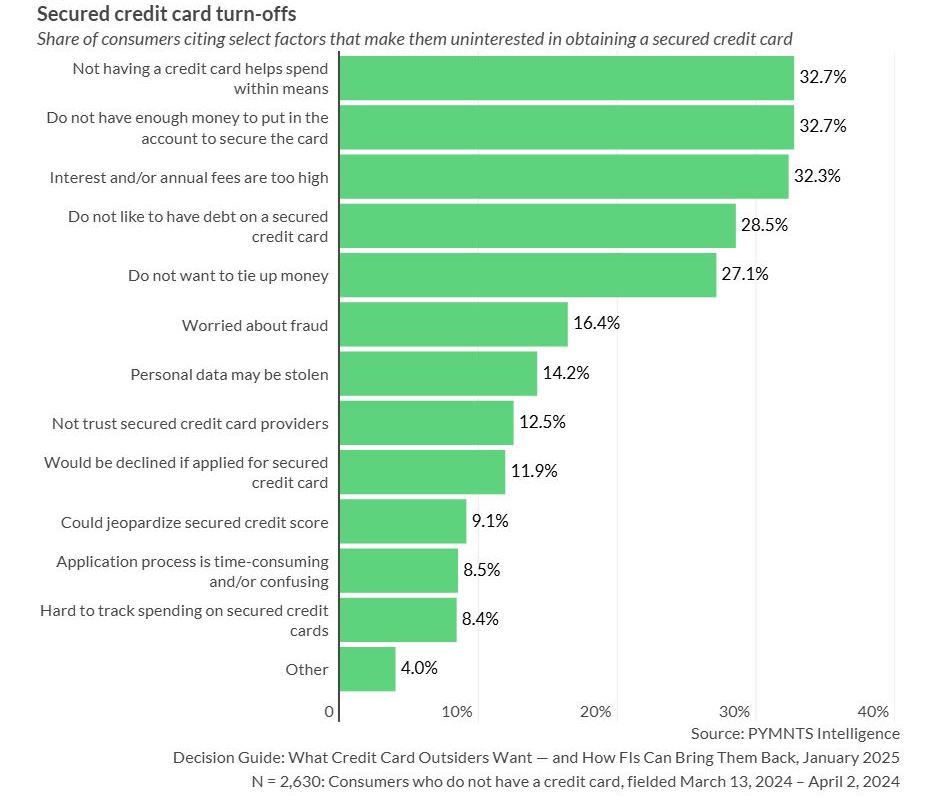

Despite the demand for secured cards, several barriers prevented outsiders from adopting them. The biggest obstacle was the upfront deposit required, which 33% of outsiders said they could not afford. Additionally, 32% said secured cards do not offer enough flexibility in spending, while others were deterred by high interest rates or annual fees. These concerns were prevalent among second chancers, with 53% citing insufficient funds for a deposit as their primary issue.

Psychological barriers such as fear of fraud (16%) and mistrust of providers (13%) complicate the appeal of secured cards. To address these issues, FIs could consider reducing deposit requirements, simplifying application processes and emphasizing the long-term benefits of secured cards, such as credit score improvement. FIs should also focus on reassuring consumers about security and transparency. Offering products that are low-cost, flexible and secure will help rebuild trust and attract outsiders, particularly those who are eager to reenter the credit market.