Financial institutions (FIs) must carefully balance staying compliant and keeping their customers safe, all without introducing frictions that could scare customers away. However, despite the friction points that can get introduced into the process due to anti-money laundering (AML) and Know Your Customer (KYC) processes, FIs have no choice but to comply, or they risk fines and loss of customer trust.

The March AML/KYC Tracker® explores the challenges FIs face to keep up with regulations, and the solutions that can help.

The March AML/KYC Tracker® explores the challenges FIs face to keep up with regulations, and the solutions that can help.

Around the AML/KYC World

Even well-meaning FIs and corporations can struggle to maintain proper compliance when working across various global markets, each with their own specific set of regulations. Yet, solution providers are working to address this issue. For instance, client lifestyle management software provider Fenergo recently announced a new regulatory rules software that can be integrated into businesses’ platforms, and serve as a repository of local and global rules for AML, KYC and other requirements.

As businesses seek to expand their reach into new markets, they need to be sure they can handle due diligence for those new sets of consumers. Global identity verification solutions firm Trulioo aims to ease the way by expanding its automated AML and KYC due diligence product to cover consumers in more markets — most recently, Bangladesh.

Other financial service providers must rethink their due diligence approaches. Recent policies in India require mobile wallet providers to administer more robust KYC processes to their consumers. Those policies affect companies like Amazon, which offers its Amazon Pay mobile wallet in the country. Some observers have noted that the eCommerce company may be trying to find an alternative to administering a full KYC process by promoting a solution that enables eCommerce shoppers to pay via Unified Payments Interface (UPI), something that would put the KYC burden on the banks.

Other financial service providers must rethink their due diligence approaches. Recent policies in India require mobile wallet providers to administer more robust KYC processes to their consumers. Those policies affect companies like Amazon, which offers its Amazon Pay mobile wallet in the country. Some observers have noted that the eCommerce company may be trying to find an alternative to administering a full KYC process by promoting a solution that enables eCommerce shoppers to pay via Unified Payments Interface (UPI), something that would put the KYC burden on the banks.

To get the rest of the latest headlines, download the Tracker.

Deep Dive: an Automated Approach to the $2T Global Money Laundering Problem

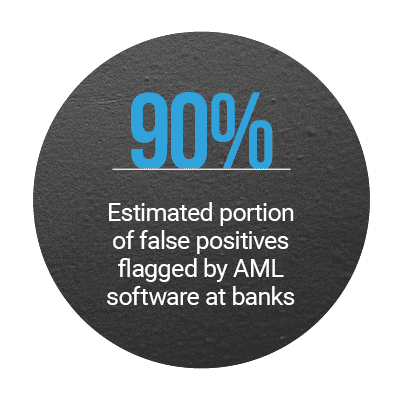

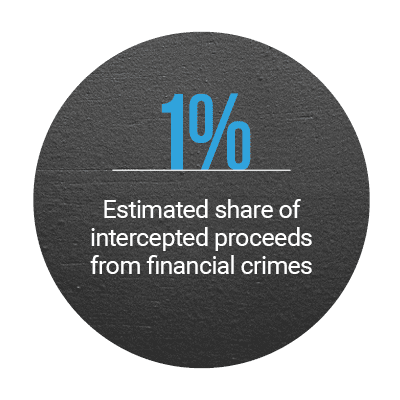

Effectively fighting money laundering can be a challenging task, and increasingly so in today’s fast-paced, globally interconnected, digitally enabled world. For FIs, keeping up with AML compliance, and staying ahead of the bad actors, can be a constant effort.

To stay current, FIs are investing in AML strategies. However, they must be sure they’re putting their money where it’s most effective. This month’s Deep Dive examines how automation tools can help FIs overcome regulatory challenges.

Read the full Deep Dive in the Tracker.

Where the UK Fails on Anti-Money Laundering

Watchdog organizations have said the U.K. is falling behind on restraining money laundering, with hundreds of billions of pounds in criminal proceeds reportedly laundered through the nation’s banks and subsidiaries each year.

Watchdog organizations have said the U.K. is falling behind on restraining money laundering, with hundreds of billions of pounds in criminal proceeds reportedly laundered through the nation’s banks and subsidiaries each year.

High-end money laundering is particularly problematic, with the U.K. frequently failing to actively investigate it or enforce AML compliance on banks and corporations, according to Susan Hawley, director of policy at nongovernmental anti-corruption organization Corruption Watch. In this month’s feature story, Hawley dug into just-released research to explain the troubled state of the U.K.’s regulatory system, including the weak slap-on-the-wrist penalties for noncompliance and an economic philosophy that may be discouraging reform.

Find the full story in the Tracker.

About the Tracker

The AML/KYC Tracker®, a Trulioo collaboration, provides an in-depth examination of current efforts to stop money laundering, fight fraud and improve customer identity authentication in the financial services space.