Digital assets are reshaping U.S. financial services, and their impact can be traced by the wake of new banking charter applications.

The U.S. Office of the Comptroller of the Currency (OCC) is receiving so many applications for digital asset-focused national trust charters that a lobbying group for the traditional financial sector, the Bank Policy Institute (BPI), is considering suing the banking regulator over its decisions to approve so many crypto, payment and FinTech companies for them.

Many crypto and crypto-interested financial firms are pursuing national trust bank charters because they allow custody and tokenization without the heavy regulatory burden of deposit-taking banks.

During 2025 alone, the OCC received 14 de novo charter applications, a number nearly equaling the total applications received by the agency in the previous four years combined.

Now, barely 2½ months into 2026, the OCC has already approved four new applications and received north of seven.

Digital lender Upstart on Tuesday (March 10) became the latest U.S. FinTech seeking a banking charter, applying to the OCC and the Federal Deposit Insurance Corporation (FDIC) to establish an insured national bank.

And while conditional approvals and actual operational status are two very different things, the direction of travel across banking implies that regulated infrastructure providers, not consumer interfaces, could be the most valuable layer of finance.

See also: Bank Charters Are Reshaping Who Can Compete for Consumer Deposits

Making Sense of Banking Charters

A predominant feature of the current charter wave is that many applicants are not seeking to become traditional banks. Instead, they are pursuing licenses that allow them to perform specific financial functions.

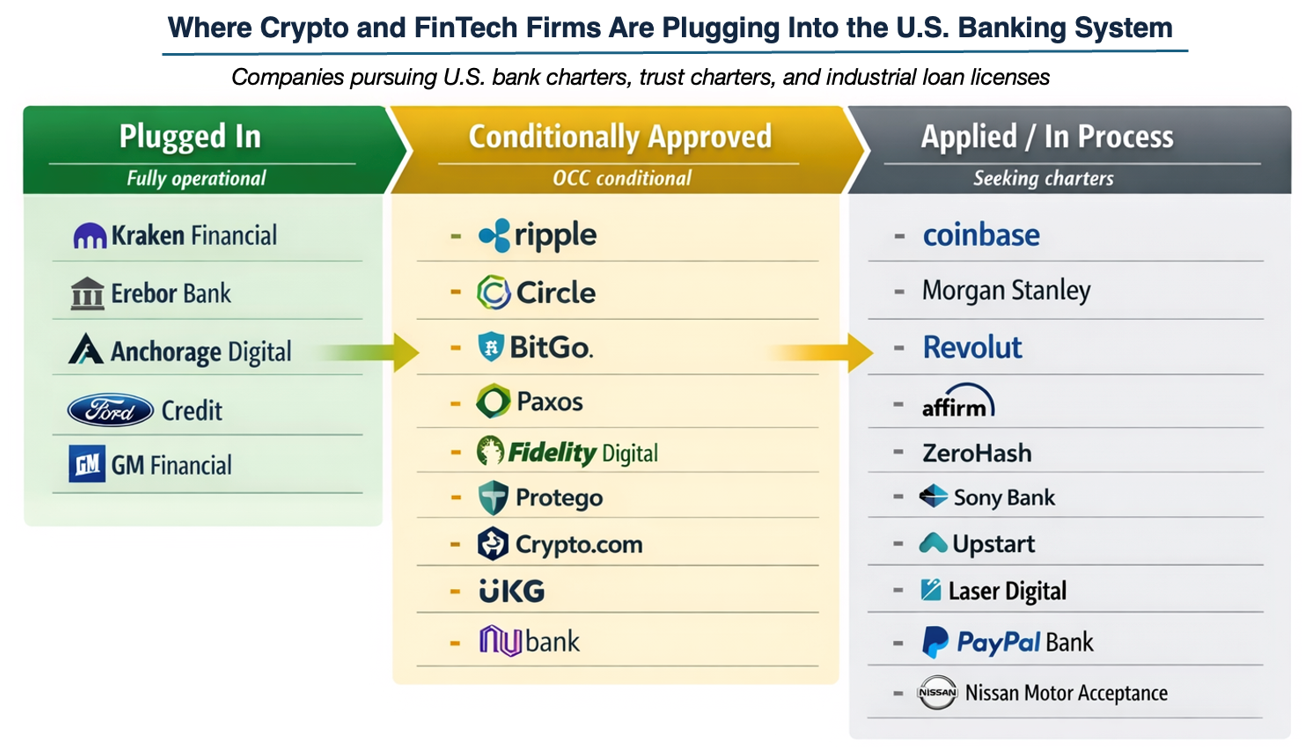

The pace of activity may be easiest to understand when visually mapped across approvals and pending applications.

As highlighted in the chart, despite the rush of approvals and applications, conditional approval does not mean a bank is operational. To launch, firms must meet additional regulatory requirements, including capital thresholds, governance structures, and operational readiness standards.

Protego’s own case highlights how difficult that transition can be. The company initially received conditional OCC approval in 2021 but failed to meet the required conditions before the approval expired. It was conditionally approved by the Treasury agency for a second time in February.

A bank charter “is not a trophy, and it certainly isn’t a product label, but it’s a public trust,” Rodney E. Hood, former acting comptroller of the currency, said in an interview with Competition Policy International, a PYMNTS company, in January.

“A federal charter should never be construed as an end run around supervision, and it should certainly never be a pathway to scale without accountability,” Hood added.

See also: Can Crypto’s Open Network Dreams Survive Going Corporate?

The FinTech Charter Strategy

Behind the charter race could lie a shift in how financial value is being created.

Historically, consumer banking has been dominated by institutions controlling deposits and lending. But digital assets are creating new layers of financial infrastructure across custody, settlement networks, tokenized securities, and blockchain-based payment rails. The companies controlling these layers may end up capturing the most value.

Research by PYMNTS Intelligence has found that 62% of Generation Z consumers would consider using a neobank as their primary bank account provider, “a striking level of openness that outpaces all other generations,” as covered here in October.

The implications, according to a paper published last month by economists Michael Junho Lee and Donny Tou at the Federal Reserve Bank of New York, could be systemic. The New York Fed report found that stablecoins do more than compete with bank deposits. They alter the liquidity demands placed on the banks that serve them. In doing so, they encourage a more reserve-heavy and potentially less loan-intensive banking model.

This model resembles what economists often call a “narrow bank.” Such institutions focus on safeguarding assets and facilitating payments while maintaining high levels of liquidity and minimal credit risk. In contrast, conventional commercial banks generate revenue primarily by transforming deposits into loans.

Regulation, as always, will have a key role to play in the future of the banking ecosystem. The PYMNTS Intelligence and Citi report “Chain Reaction: Regulatory Clarity as the Catalyst for Blockchain Adoption” found that blockchain’s next leap will be shaped by regulation. While evolving guidance is starting to create the foundations for safe, scalable blockchain adoption, “implementation challenges … continue to complicate progress.”