How to Catch the Next Wave of Digital Transformation

Steve Ballmer’s reaction to the release of the iPhone in 2007 is regarded as one of modern business history’s most egregious faux paus. As the story goes, the then-president of Microsoft scoffed at the idea of a $499 phone that lacked a keyboard and, by extension, any appeal to the business crowd.

His strategic blunder was the failure to see the power of putting a personal computer — and a year later, an app store filled with apps — in the hands of every person on earth. This cost Microsoft and its Windows OS the opportunity to be a player in the rapidly growing and eventually massive smartphone market that defines our times.

Fifteen years later, the iOS and Android operating systems — and the smartphones they power — are at the heart of the digital transformation we see happening all over the world.

At the end of Q2 2022, PYMNTS’ study of 15,000 consumers in 11 countries, which comprise 50% of global GDP, finds that digital engagement is on the rise everywhere as more consumers use digital methods to engage in one of the 37 routine activities measured by the study. Nearly 84% of the consumers in the study recently engaged in at least one of those 37 digital activities, even as they resumed their physical world activities.

Platforms that enable technologies and payments providers have made the digital experience better, more accessible and more efficient for consumers looking to allocate their time.

Expanded payments choice, including installment payments and BNPL options, have unlocked more digital buying experiences for more consumers, and merchants have benefitted from higher conversions. Logistics and more efficient business payments and trade finance have and will continue to improve delivery and distribution for the merchants and businesses that support the delivery of these digital products and services.

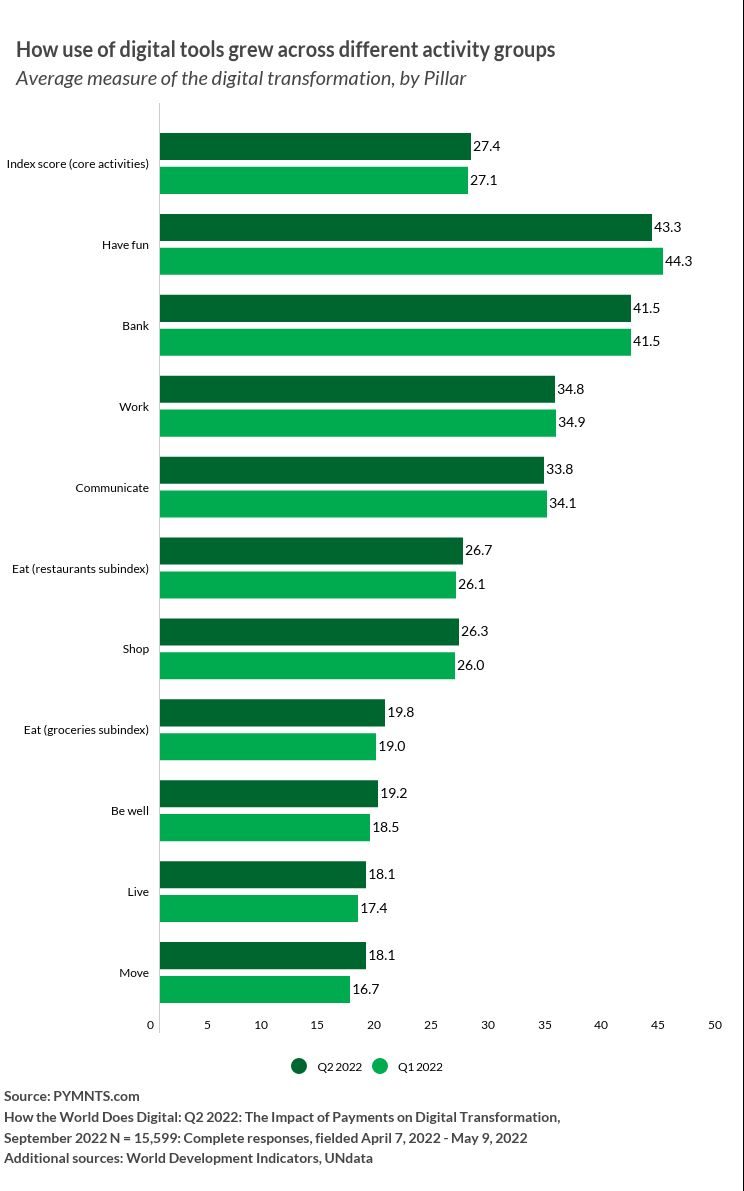

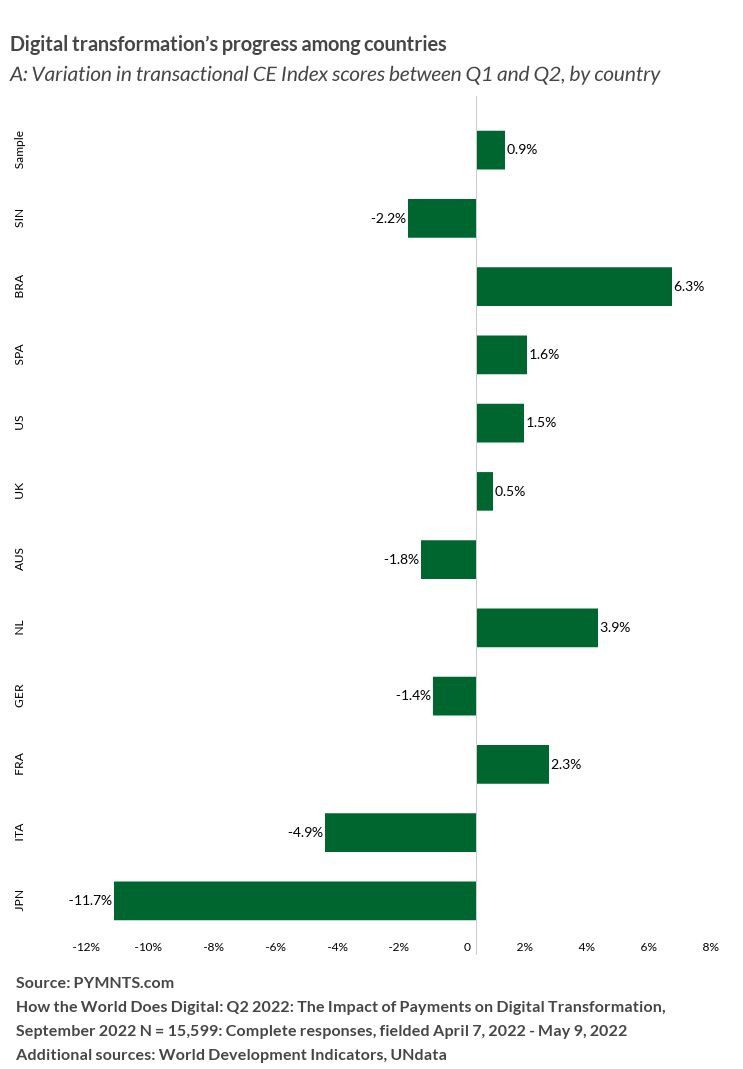

For that reason, The ConnectedEconomyTM Index, which measures digital transformation’s progress based on the number of people engaging in digital activities and the frequency of their usage, increased 1.2% between Q1 and Q2 2022.

Despite that progress, we still have a long way to go before all consumers use connected devices, technology and payments in some way to access and/or complete the 37 routine activities we monitor.

For entrepreneurs and business leaders, that’s great news.

In the six months and two global studies we have conducted this year, we see a roadmap emerging for bringing more consumers everywhere more fully into the digital economy.

That roadmap involves making the physical world an extension of consumers’ digital experiences. I have been writing about this concept since 2019, as it became clear then that the decade of the apps and smartphones would begin the transition to ecosystems and connected experiences as the calendar turned to 2020.

Read the 2020 New Year’s Day prediction: Welcome To The Connected Economy

Making the physical world part of the digital experience

The digital transformation of the world’s economy was already well underway when the pandemic, starting in March 2020, created an overnight incentive for people everywhere to do more things online that they once did in the physical world.

By the end of 2019, digital had already hastened the decline of physical retail and mortally wounded the print media business and the advertising model that supported it. Digital had given birth to the gig economy business model that made it efficient for supply and demand to find each other in many business segments and had expanded access to music and video content via apps like Netflix and Spotify. Social networks connected billions of people all over the world with each other, and online marketplaces connected sellers with buyers and eliminated the need to be within driving distance of a store to buy something from it.

Related to that shift in retail: Why Consumers Are Firing Traditional Retailers

The discussion about the blurring of the lines between the physical and digital worlds certainly isn’t new.

But digital transformation’s next wave will go farther than blurring the lines between physical and digital channels — it will make them invisible. Over the next several years, the physical world will increasingly become more of the consumer’s digital experience.

That will make the activities, not the channels consumers use to access them, the focus of successful innovators. They’ll take as their guiding principle the reality that nearly every physical world experience will start in the digital world with a connected device of some kind: the search for a doctor, fitness studio with classes on Saturday mornings at 8 AM, closest hair or nail salon, coupons for products for items consumers want to buy, a store with winter blankets on sale and in stock, the best neighborhoods to buy a home in St. Louis.

Innovators make the related physical engagement more valuable and less friction-filled, and in the end, those experiences will complement and close a sale already far along in the process. Channels will have to adapt to the consumer’s preferences and not the other way around, making the trip to the store, doctor, real estate agent’s office or gym worth their time and their money.

Consider what savvy retailers are doing to make the consumers shopping experience better.

MatchesFashion, an online specialty department store with three stores in London, allows customers to add the items they see on the store’s website or app to their wish list and arrange to have them waiting in a dressing room to inspect and try on when they arrive. Fitters and stylists are on standby to tailor items as they are being tried on — no better way to close a sale then to have clothing altered — and to style outfits. The store’s total offering is a shopping experience that started online, maybe weeks before the shopper ever walked through the doors, and finished with a purchase in the fitting room.

Take grocery shopping as another example, where platforms and tech will force a similar shift in the $11 trillion global grocery market. The divide between digital and physical is eroding and may collapse completely in the next few years, even as 80+ percent of groceries are still purchased in the grocery store today.

See more: 58% of Consumers Increased Online Grocery Shopping in Past Year

Over the last two years, food has become, like every other purchase, something that consumers are more comfortable buying online. A digital shift created by the pandemic translated into habits that have stuck with the consumer. An increasingly hybrid work environment has shifted grocery shopping from a weekend chore in the store to a weekday order for delivery or curbside pickup. Subscription services such as Amazon Subscribe & Save and D2C specialty brands are whittling away the center aisle purchases from grocery stores — of course, at different paces with different merchants in different countries — and will for some time.

Further reading: The Omnichannel Grocery Report: Leveraging Digital Purchasing Channels To Boost Conversion

Delivery aggregators have increased grocery store competition by making the consumer’s choice for where to buy their groceries independent of having to hop in the car to get there. Smart grocery store executives will shift their focus away from the channel a consumer shops to the activity the consumer is doing when shopping: buying food for their family wherever and whenever she finds it convenient.

See the study: The 2022 Global Digital Shopping Index

Then there’s the whole set of activities where digital engagement remains nascent.

Healthcare is one of those greenfields, poised for a similar global disruption as patients and doctors are challenged in different ways to make the physical experience of seeing a doctor a valuable or necessary extension of digital-first engagement.

In many markets, including emerging economies, telemedicine is the difference between having no access and having a digital lifeline to doctors who can diagnose and treat patients suffering from common ailments. The challenge for innovators to overcome is one of basic infrastructure — connectivity — and the logistics necessary to get medicines to consumers living in those remote areas.

In developed economies, telemedicine will languish unless it becomes a better use of the consumer’s time and money.

When the pandemic made seeing the doctor difficult, access to a telemedicine specialist using a digital channel became almost as much a lifeline as it was in lesser-developed countries. Today, televisits have become an expensive stutter step to seeing a doctor, and a channel that consumers will likely skip after a few bad experiences.

Read more: The Data Point: 46% of Americans Mixing Telehealth, In-Person Care

Innovators that align telemedicine use cases with the technology and diagnostic devices that save the patient and doctor time will make the channel of delivery irrelevant, and the provision and payment of healthcare a better connected digital experience.

Digital engagement becomes contagious

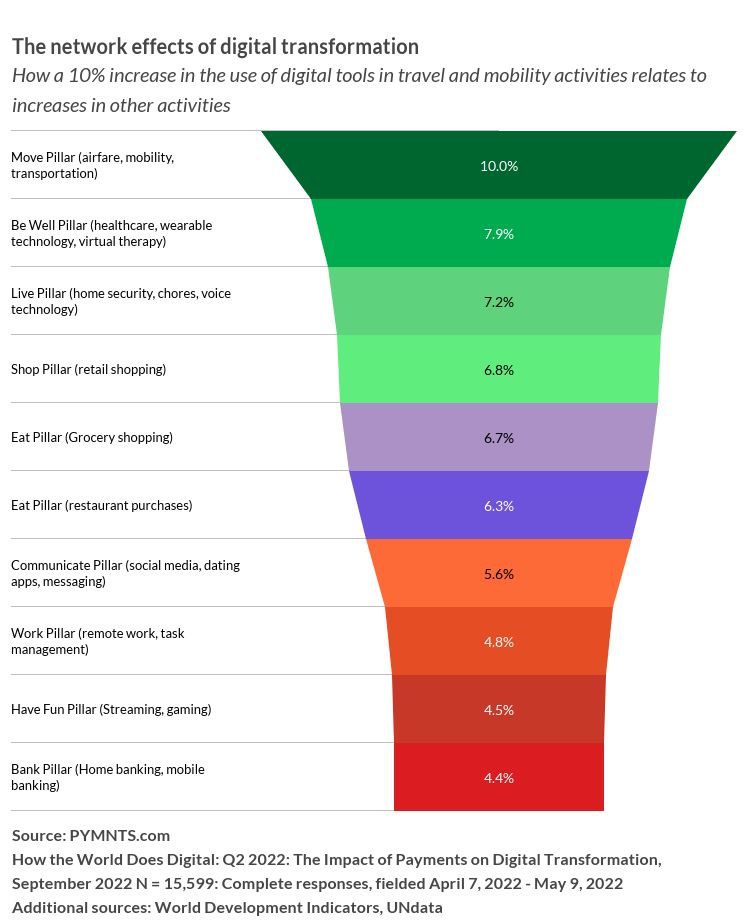

Call it the network effects that make innovators swoon: Consumers who engage in one digital activity also engage digitally in other activities that share similar characteristics or are related to something they are already doing using digital methods.

In Q2, we find lots of opportunity for innovators to swoon.

Half of consumers across all 11 countries who used digital methods to book travel or local transportation also used digital methods to order food from restaurants or grocery stores. More than half also used digital methods to make retail purchases. The common thread is travel of some kind: for work or pleasure, and the efficiencies of sticking with digital methods to access and purchase things related to those experiences.

But the network effects don’t stop there.

Based on these observed correlations, we have used our model to estimate the increase in digital engagement across all 37 activities that would be associated with a hypothetical increase in digital engagement of 10% in local transportation or travel activities.

What we find is that the more exposure consumers have to accessing services and making purchases using digital methods, the more they will stick with those behaviors. They’ll also be more likely to explore new ones based on the trust and confidence and ease and convenience they have in other areas of digital engagement.

“Super Apps” are banking that such correlations in digital activities will drive demand for consumers to want a single place to digitally engage in a set of activities that once required multiple apps and logins. We see that in China and other Asian markets. PYMNTS research shows that nearly two thirds of consumers in the U.S., U.K., Germany and Australia have an interest in using a Super App to make buying things and managing their finances more efficient.

Find out more: UK Consumers Trust PayPal More Than Banks to Provide Super App, Study Finds

Innovators have an opportunity to use the power of these network effects to determine how and where they fit, to influence consumer engagement in activities that connect in some way to their core product or service or by being more accessible on the open web as consumers use search to discover new products and experiences.

We also see enormous potential to integrate payments into the digital activities that consumers largely use today to access services or content.

Eighteen of the 37 activities that PYMNTS monitors are those used by consumers to access content or services, but not to make a purchase: watching movies, listening to music, messaging their friends and family, connecting on social networks. Embedding payments and finance into those experiences has the potential to convert the attention of a captive audience of consumers into a commerce experience.

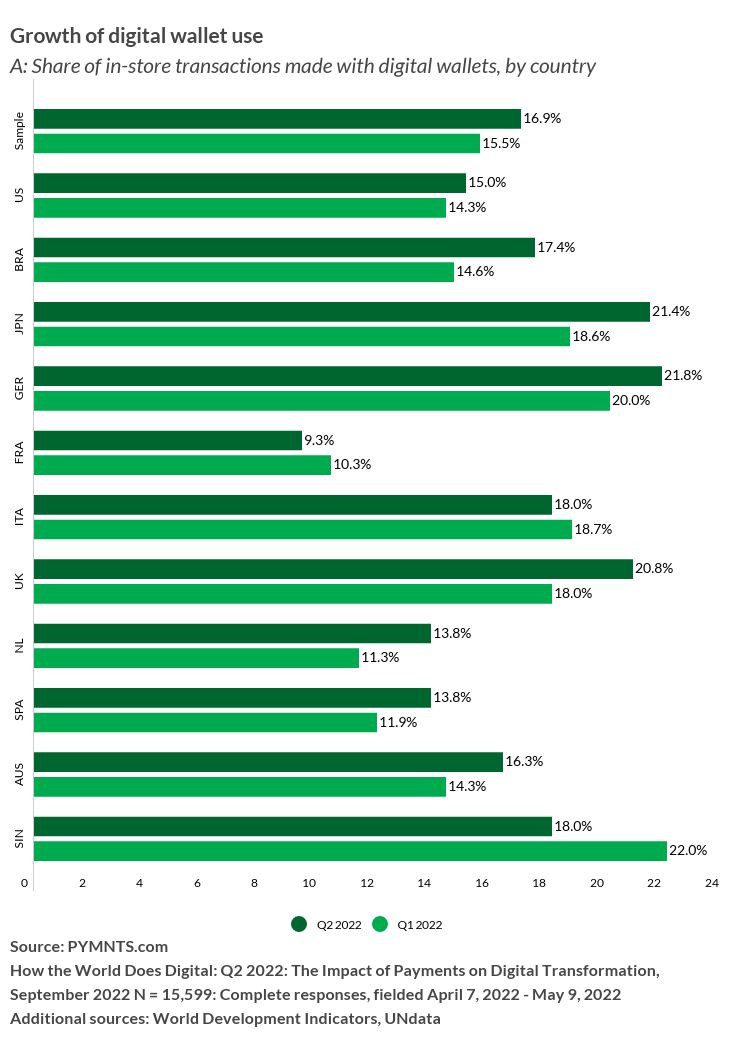

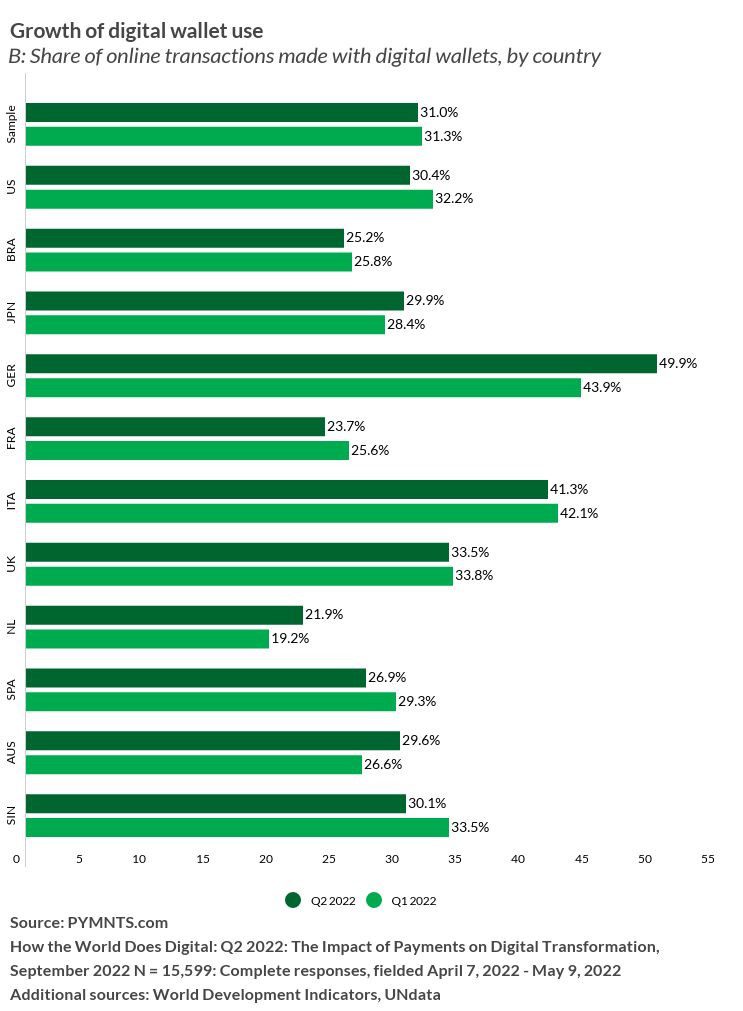

Mobile wallets go in store, but not far enough

In Q2, PYMNTS’ study finds that the use of mobile wallets to pay for purchases made in brick-and-mortar establishments increased by 9%. The greatest increase of in-store digital wallet use was in Brazil, Japan and the U.K., the latter largely driven by an increase in use of Big Tech wallets, e.g., Apple Pay. Native or domestic wallet usage was the principal driver for the increase in digital engagement with mobile wallets in Brazil and Japan.

That’s the good news.

Everywhere, the use of mobile wallets to pay for things in the store pales in comparison to their use online — by as much as a third in some countries — and everywhere remains a small fraction of retail sales. In the U.S., the instore mobile wallet story is nothing short of disappointing as the lowly plastic card remains the fiercest competitor at the point of sale despite mobile wallets’ eight-year march to replace it.

Get the numbers: Mobile Wallet Adoption: Apple Pay Still the Big Fish in a Small Mobile Payments Pond

What held mobile payments’ use back was positioning them as a replacement for a card at a terminal in the physical store, rather than a cornerstone of an entirely new checkout experience that lives in the cloud.

Innovators who are focused on the transformation of checkout are already thinking past wallets as a form factor to a set of identity and payments credentials that authenticate the user when they log into an app or a connected device at a store, start their connected car or tell their voice assistant to send the same basket of groceries they ordered last week to their home later in the day.

What’s Next

Macroeconomic uncertainty and a global consumer challenged to keep pace with historic levels of inflation have forced business leaders and entrepreneurs to make the right bets on where to invest time and money to generate a profitable return. Many of the playbooks that looked great in January, and probably even June, have been tossed aside as consumer and business sentiment have shifted. Everyone everywhere is looking for “what’s next.”

Six months of examining the digital behaviors of 15,000 consumers living in 11 different countries hasn’t uncovered the big lightning bolt quick-fix. Rather, it confirms the power of such a simple concept: physical and digital channels no longer compete as digital reinvents the physical world in mutually reinforcing ways.

Labels like omnichannel minimize that potential, and so do cutesy buzzwords.

Business leaders and entrepreneurs have the power to rethink how to use the advantages of both worlds for the benefit of consumers and businesses everywhere in the world. There is a long runway for doing that, starting with getting more consumers digitally engaged in something, then letting the network effects accelerate their own engagement and that of the country in which they live.

There are many fortunes yet to be made for those who use technology, software, data and connected devices to make digital more physical and physical more digital — and for those who create new sources of value by embedding payments into those experiences as the $84.2 Trillion global economy moves digital.