Welcome To The Connected Economy

Making predictions is simply irresistible at this time of the year – this year in particular.

Tuesday marked not only the end of a year, but the end of a decade. Not just any decade, but one that has seen unprecedented levels of innovation touch nearly every industry segment and almost every corner of the world.

Predicting the future, though, is risky business – which may explain why many predictions are wishy-washy or soon proved wrong.

There’s a famous Steve Jobs quote, though, that I think frames any conversation about the future in a more thoughtful way.

Jobs said that predicting the future can’t be based simply on assumptions about what might happen. Instead, he said, looking ahead starts with looking back, then connecting the dots that define the present. Only then, he said, can one get clarity about how those dots can guide innovators about the future.

The last 10 years in payments and commerce have given us millions of dots to connect.

The introduction of the iPhone in 2007 – and the birth of the apps ecosystem a year later in 2008 –inspired an entirely new class of innovators, starting the 2010s with a brand-new toolkit. Armed with new tech, mobile devices, data and the cloud, they fast-tracked the shift from a largely analog world to the app-based economy of today.

Over the last decade, the combination of smartphones and apps has changed how we shop, how we pay, how we connect with people, how we discover and consume information, how we work, how we bank and even how we are paid.

In many ways, however, the decade of the 2010s was the warmup act for the transformation yet to come – the transition from an app economy to one in which connected ecosystems aggregate commerce experiences and enable transactions across channels, devices and environments.

Payments will power that shift.

That connected economy will be the result of the full force of the Internet of Things (IoT) in action. Just about every device will be connected to the internet and capable of enabling a transaction – between every possible permutation of machines, people and businesses. In this new connected economy, we will find ourselves living in a world where new networks, intermediaries and enablers will change what is today considered the payments and commerce status quo.

A status quo that a decade ago seemed almost unimaginable.

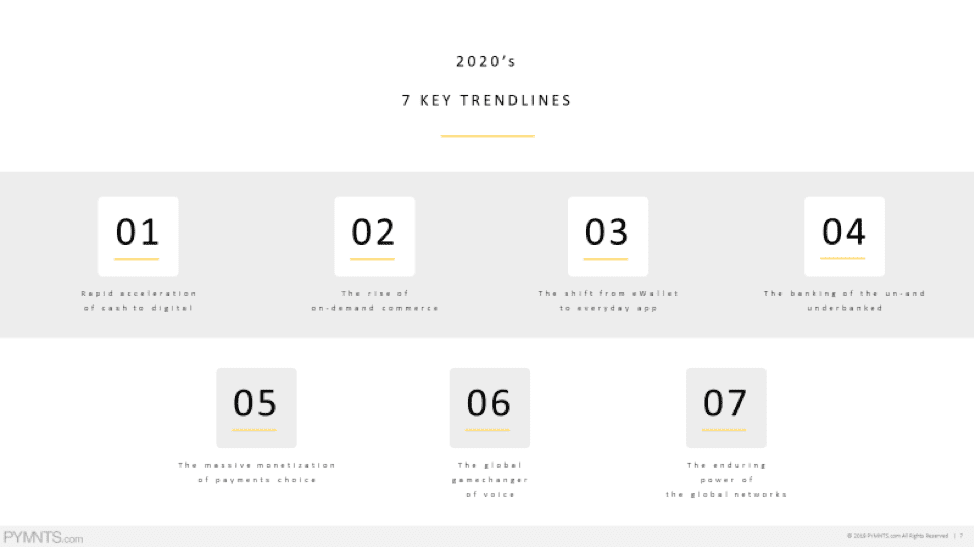

I’ve connected a few of the dots from over the last decade that I believe will shape how the world will evolve in the 2020s, as well as the role of payments in driving that change. From those emerge seven trendlines that will influence the direction of the exciting new decade that will begin a few weeks from today.

2020 Trendline One: Rapid Acceleration Of Cash To Digital Payments

Cheaper smartphones and more access to fast internet everywhere in the world will accelerate consumers’ demand to move cash to digital payment methods. Ironically, cash-in and cash-out networks will play a critical role in enabling that shift.

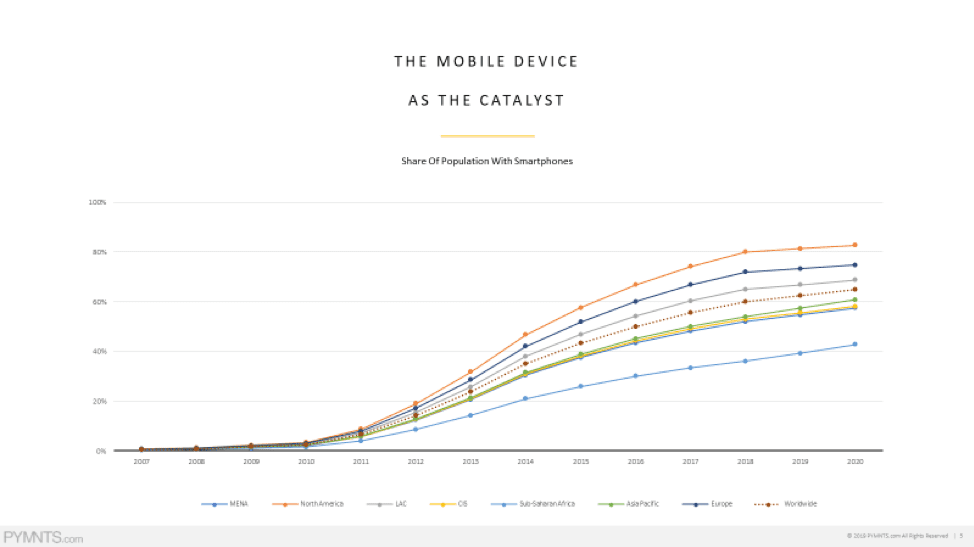

Today, there are 7.3 billion people in the world, 5.1 billion of whom have a mobile phone. That’s roughly 67 percent of the population – and in five years, that will grow to 71 percent. According to the GSMA, 79 percent of those users will own a smartphone.

And that’s just five years from now.

Looking across the globe, the average cost of a smartphone today is about $341, with Europe and the U.S. driving that figure higher. Yet today, a person in India can buy a pretty good smartphone for about $100 – and more competition and creative business models will only drive those prices lower over time.

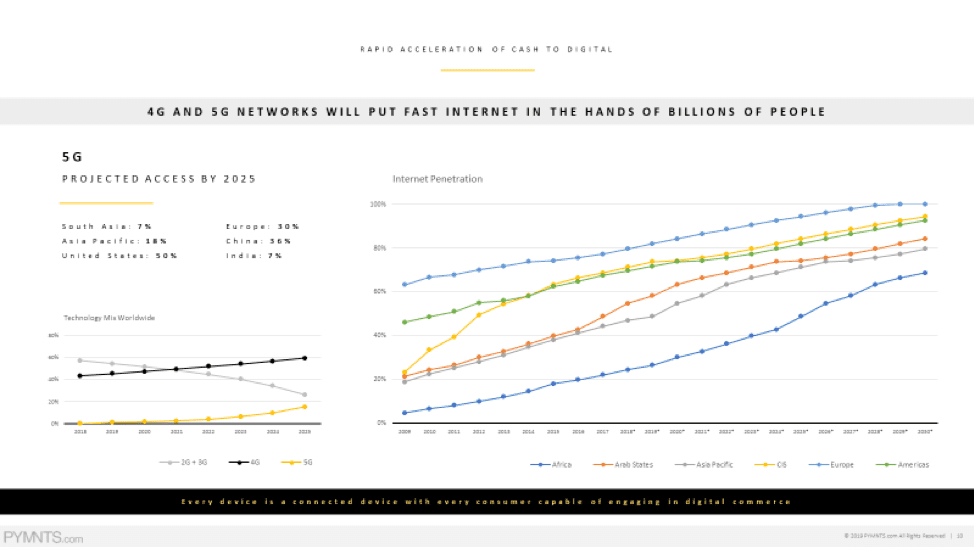

The demand for those smartphones (and the competition for lowering their prices) will increase as access to faster internet comes online, as developing markets move from 2G/3G to 4G, and as developed markets move from 4G to 5G.

In developed markets, 4G will move to 5G with 15 percent of mobile phones connected, and to 5G five years from now.

Access to faster internet means consumers everywhere can tap into ecosystems that were once largely unavailable to them, or not available in any sort of robust way. In developing and emerging economies, thin-feature, phone-friendly apps will give way to more robust apps and ecosystems that power shopping and buying online, paying bills, banking – even building a credit profile and receiving microloans.

When nearly every phone is capable of conducting a transaction and nearly every adult human on the planet is capable of engaging in digital commerce, there will naturally be a spike in demand to digitize cash and take advantage of a connected digital ecosystem that was once totally out of reach.

This is happening even faster than we anticipated.

Cash usage, across the more than 60 countries that PYMNTS has tracked over the last decade, has seen modest growth, even outpacing the overall GDP growth in many of the key countries we monitor. Much of that growth is driven by the growing size of the spending pie – that is, even if cash is declining in use as a payment method, more people spending more money will sustain or increase its use. That’s true even in developed markets like the U.S., where mobile devices, apps and digital methods are strong, and cash usage continues to maintain a stable course.

Fast-forward to the decade of the 2020s, and we will see a rapid deceleration in the growth of cash in many economies, including those that are today largely cash-centric. Cash, while important, is rapidly digitizing as consumers in emerging economies are keen to live in a connected, digital world.

That desire will drive demand for platforms to enable that cash-to-digital shift – and for the players in the connected economy to create new use cases that meet the needs of these emerging digital natives.

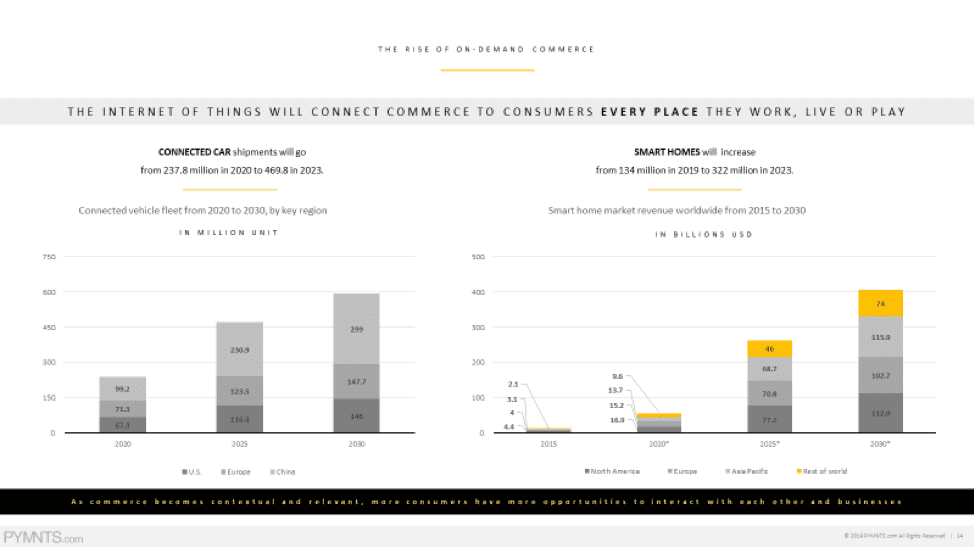

2020 Trendline Two: The Rise Of On-Call Commerce

In an analog world, consumers had to consciously carve out time to go shopping to discover what to buy and then buy it, do their banking and pay their bills.

Today, with mobile devices and apps, commerce is portable – simply a click or a swipe away. But in the connected economy, commerce will be all around us. Our homes, cars, workplaces, schools, hospitals and cities will become powerful software platforms capable of enabling on-call commerce by anyone, at any time and using any devices – and seamlessly across these ecosystems.

The notion of on-call commerce will do more than simply blur the lines between the online and offline worlds: It will make commerce present – and effortless – in entirely new channels, creating new efficiencies that will have a positive impact on the economic well-being of countries all over the world.

In emerging economies, this transformation will be led by smartphones. In Vietnam, to take just one example, smartphone penetration will reach 77 percent three years from now, up from 25 percent today. Southeast Asia will see 370 million new mobile users in the next five years, bringing smartphone penetration to 72 percent of that region’s population.

Back in the developed world, smartphone adoption will reach nearly 100 percent of the adult population – in the U.S. and Canada, it will grow from 83 percent of the total population today to 90 percent in 2025, and in Europe it will move from 73 percent to 83 percent in that same timeframe. And eCommerce volumes will soar, with countries such as China, Japan and the U.S. witnessing growth rates that are double, triple or even quadruple the projected global annual growth rate of 18.5 percent over the next five years.

But the shift from portable commerce to on-call commerce will come from the explosion of connected devices, which will push commerce anywhere a device and an internet connection intersect.

In five short years, by 2025, there will be more than 25 billion devices capable of interacting with the internet – up from nine billion today. Everything from cars to homes to offices to appliances will be capable of enabling transactions. Appliances will troubleshoot problems before they exist, ordering parts and alerting service technicians to set up a service call before things break down. Cars won’t need consumers to bring along their mobile phones to make them smarter, connected and capable of transacting. Connected car shipments in the U.S., China and Europe are expected to nearly double in the next three years.

Homes will get smarter, too.

Today, a little more than a quarter of U.S. homes are connected to the internet via some form of a smart device, with nearly half expected to be “smart” five years from now. And this is not just a developed economy phenomenon. Homes all over the world are getting smarter, as new construction incorporates smart elements into the building process, and homeowners install doorbells, light fixtures and other “smart” devices linked to a virtual assistant as they upgrade and remodel their residences.

It’s all part of the growing trend of consumers making the home the center of their connected commerce world – a trend that we saw emerge in our third annual How We Will Pay study, done in collaboration with Visa.

That’s not just because consumers can shop and buy online without leaving the house. Today, many of the activities that consumers once could only do outside of the home can now be done without leaving it.

More consumers are working from home, which changes their patterns and preferences for shopping and eating, as well as their daily routines. They’re watching Netflix at home while eating carryout instead of going to dinner and a movie. And instead of investing in tickets to go to a game, they’re investing in smart flat-screen TVs to watch live sporting events at home with friends. Instead of going to the gym, they’re climbing on their Peloton bikes or exercising in front of their Magic Mirrors with trainers and others who are part of those digital fitness communities.

All of these developments have laid the groundwork for the on-call commerce experiences that will shape how and why consumers engage with businesses of all types – forcing firms to adapt to those changes in order to attract consumers who increasingly want commerce delivered on demand.

2020 Trendline Three: From The eWallet To The Everyday App Ecosystem

A decade ago, the conversation about digital payments was largely about registering payment credentials with a third party to make online checkout less friction-filled wherever those “buy buttons” were accepted.

What a difference a decade makes.

Today, there are some 190 variants on the mobile wallets theme – literally a “Pay” for every person and every use case, with most driven from the birth of the smartphone/app ecosystem.

Some, like M-PESA in Kenya and I-Mode/DoCoMo in Japan, are enabled by telcos. There are Pays courtesy of mobile operating systems, like iOS/Apple and Android/Google and Samsung.

Others, like China’s WeChat Pay and Alipay, are enabled by internet giants – one with its roots in a social network and the other in a commerce ecosystem, Alibaba, which is also how PayPal got its start in 1998.

Still others, like Amazon and Walmart, are merchant-driven, linking authentication credentials to registered payments credentials to check out online and offline.

The next decade’s conversation will be different.

Today, consumers toggle between a variety of apps on their mobile devices to discover what to buy and pay for what they buy, to bank and pay bills, to send money to people, and to save and invest. A decade from now, consumers will spend much of their time inside one, or just a few, everyday connected ecosystems that enable all or many of those activities without stepping outside it. Consumers will move fluidly inside of that ecosystem instead of between the 20 or 30 apps that enable that engagement today.

We’re seeing it happen today as these ecosystems, with their critical mass of authenticated consumers and registered credentials, add more services to capture more of their users’ time and attention in an effort to become the “go-to” app.

Walmart has expanded its financial services ecosystem to include healthcare services for its users, in addition to making P2P transers, bill pay, savings and payments part of the services they provide. Amazon is leveraging Western Union’s global cash in/cash out network to let consumers shop online and pay in cash at one of their 500,000 global agent locations. Facebook wants to integrate payments to become a commerce platform instead of just an advertising platform. Apple has introduced a credit card and companion card app with personalized offers and an easy customer interface to drive more Services revenue. Uber is giving its drivers free digital wallets to receive their pay (and, they hope, all of their other pay as well) as well as access to special deals and promotions to linked to that account to keep more of them driving for the company. In South Asia, Grab and Gojek are giving drivers and consumers access to financial services, including microloans.

PayPal’s ecosystem gives consumers options to register a variety of payments credentials (and access to installment credit via PayPal Credit) and to use any of them to pay at a merchant. PayPal accounts can accept funds (including pay and cash), store funds, tap into working capital, receive instant settlements from a merchant on their platform and save money via a third-party app. With its recent acquisition of Honey, PayPal will help its users get the best deals on the products they would like to buy.

Google has embedded commerce into search across a wide variety of use cases, including travel, food ordering and food delivery. Storing credentials in Chrome creates a Google Pay account that consumers can use when shopping online at a merchant on that browser. The company’s recent announcement of a smart DDA with Citi is a potentially very “smart” move in bringing banking inside Google’s ecosystem with one of the most respected industry names – and on a global scale. And Google’s recent announcement that PayPal COO Bill Ready will join the firm as president of commerce in January is just the latest signal of how serious Google is about turning its search and advertising platform into the everyday ecosystem where consumers can interact – cross-channel and cross-platform.

As with many things, consumers don’t always know what they really want until they see it. Yet last summer, when we described what an “everyday app” might do for them in a PYMNTS study, more than half of all U.S. consumers said they’d be interested. As consumers search for speed, convenience and value in an increasingly time-challenged world, the appetite for simplifying their commerce experiences inside of a small number of very rich ecosystems seems high. And Big Tech (Amazon, Google) and FinTech (PayPal) players top the list of those who would like to enable it.

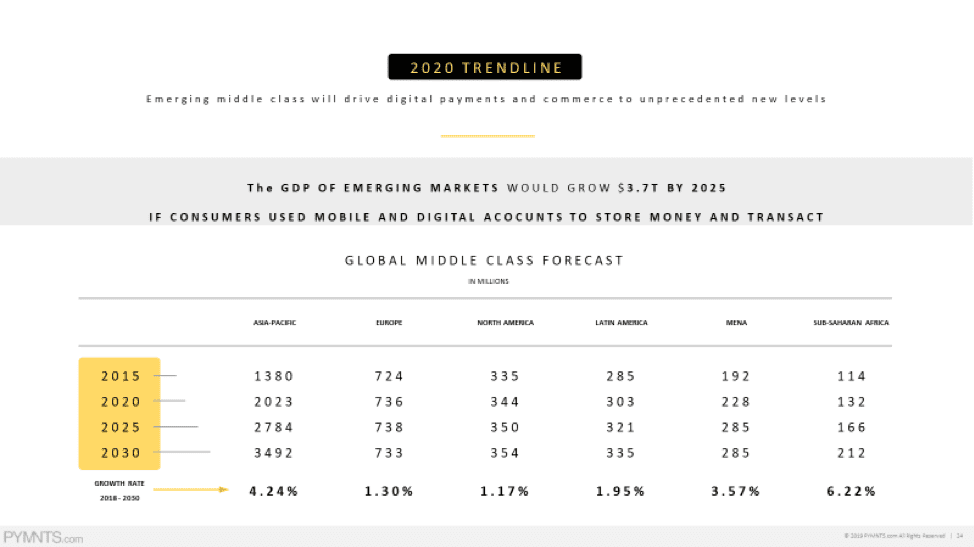

2020 Trendline Four: Banking The Unbanked And Underbanked

Today, nearly 70 percent of adults worldwide have access to a bank or bank-like account – either from their bank, a FinTech or a telco – up from 51 percent at the turn of this decade. In a world in which all seven-plus billion humans living on the planet will soon have a smartphone that can access apps and the internet, it’s hard to imagine that those who lack access to a bank account and/or bank-like services today will have to go without for much longer.

That includes those living at the very bottom of the pyramid today – and who, with such access, will finally have a way to participate in the financial services ecosystem. For these underbanked and unbanked people, their mobile phones will do more than allow them to create an account that can store value and enable digital transactions. These accounts will also integrate payments credentials with identity credentials to further streamline and protect parties to those transactions. Governments and others that distribute funds will have a digital means to do so, securely and compliantly, with the knowledge that funds will reliably reach those for whom they are intended.

With that access will come the visibility necessary to build a credit and financial history, which could pave the way to credit and microloans, as innovators use data and artificial intelligence (AI) to underwrite risk and build credit profiles.

With that access comes the potential for those individuals to build microbusinesses, sell their goods and services on digital marketplaces, and build and fortify a new emerging middle class.

And that also means an onramp for financial stability and financial independence – and economic prosperity for the countries where these 1.7 billion people now live.

This new emerging middle class will drive digital payments and commerce to unprecedented levels over the next decade. And it will fuel the interests of innovators and incumbents alike to use financial inclusion as a springboard to delivering the financial independence that billions of consumers once considered out of their reach.

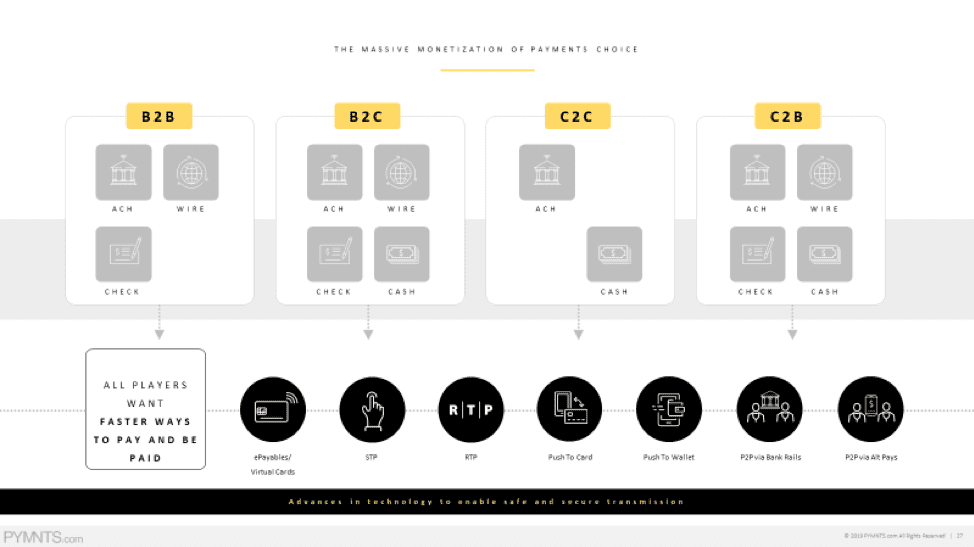

2020 Trendline Five: The Massive Monetization Of Payments Choice

In an analog economy, the world was standardized on a small number of ways to move money between people and businesses because there weren’t many available options.

In the apps economy of the 2010s, the number of digital options expanded dramatically for consumers and businesses – and with that expansion came pressure to enable acceptance by merchants and by businesses.

Over the last decade, on the retail side of payments, merchants waited to expand checkout choice until they felt that sales were at risk if they didn’t. On the B2B side of payments, acceptance by suppliers of anything other than a check or ACH payment often came through brute force. The larger the enterprise, the more demanding the supplier onboarding process becomes, and many simply defaulted to the paper check, particularly for one-off or infrequent ad-hoc payments, including disbursements. Today, the paper check still drives well more than half of all payments made between businesses – a percentage that’s even higher when small businesses pay each other.

In the connected economy of the 2020s, all businesses will be challenged to enable choice, as consumers push for options to pay and be paid using the many options available in their wallets today. And businesses will awaken to the notion that choice delivers a competitive advantage, including the choice to receive funds much faster than they move today – and in some of those cases, in an instant.

The opportunity for businesses and payments providers to monetize choice is nearly as massive as the challenge for businesses to enable it, particularly for B2B payments, where getting buyers and suppliers to support choice for the dozens, hundreds, thousands or tens of thousands of suppliers that are paid is daunting.

Delivering and monetizing choice means recognizing that businesses, like consumers, find the option of preserving it so compelling that they are willing to pay to give or receive it in many cases.

Over the next decade, enabling choice between businesses and between businesses and consumers will only accelerate the demand for platforms that deliver it across the entire end to end experience — from onboarding to risk management to credit to data to reconciliation to the incentives that give buyers as much of an incentive to enable payments choice, as suppliers who want to receive it.

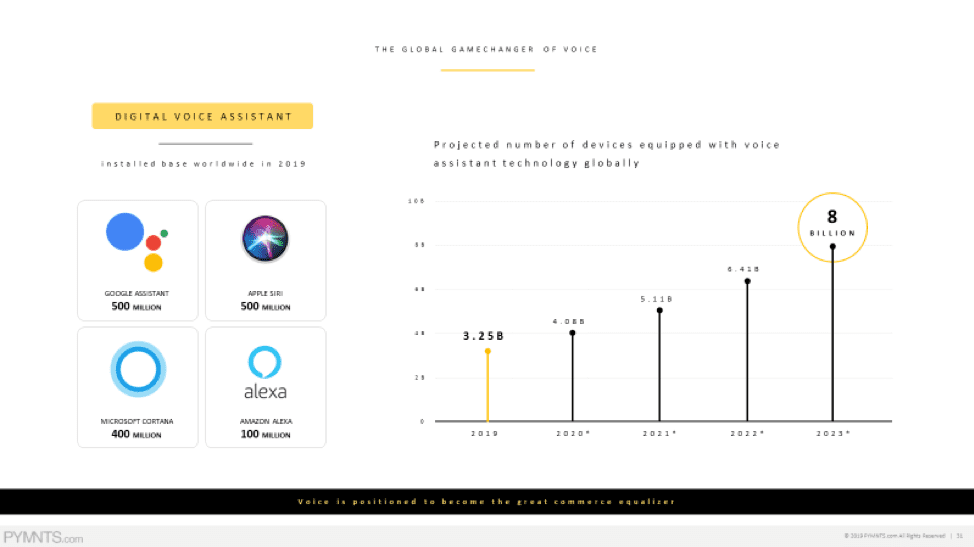

2020 Trendline #6: The Global Game-Changer Of Voice

Voice emerged in the second half of this decade as the new commerce ecosystem, one that will power the connected economy of the 2020s.

In fact, I said this years ago when I first saw the Echo device, as primitive as it was at that time. I wrote a piece shortly thereafter about voice as a powerful new payments and commerce intermediary – an ecosystem of skills connecting a virtual assistant to the activities consumers want to engage in. Intermediaries based on voice, I wrote then, had the potential to shift the power away from the card brands, bank brands and merchant brands to the product brands as consumers got hooked. Consumers would expand the use of those powerful virtual assistants beyond asking them to tell jokes or to answer basic questions to searching for information about what to buy, building their shopping lists, playing music, making telephone calls – all using the power of the human voice to replace the time and the tedium of apps and typing and swiping.

In four short years, we have seen the rapid adoption of voice-activated speakers and the rapid emergence of ecosystems and apps that have grown up to support both Alexa and Google Assistant. The shift was so fast, in fact, that it took half the time for 25 percent of the U.S. population to own a voice-activated speaker than it took to have broadband installed in their homes.

Today, based on our own research, more than 30 percent of consumers report owning a voice-activated speaker – more than triple the number who reported owning one over the three years PYMNTS has been tracking this – and nearly as many reported using it to make a purchase. That will only increase as voice plus visual – via a smart device with a screen or a voice-enabled mobile device – streamlines the commerce process.

In many ways, voice is the great payments and financial services equalizer – the most ubiquitous and natural of all ways to communicate and trigger a transaction. Over the next decade, voice commerce and the virtual assistants that enable access will accelerate the growth of the everyday app ecosystem, as well as the consumers’ embrace of the everyday ecosystems that will simplify their lives and the payments and commerce experiences that underpin them.

And two key players will emerge to dominate that experience – Google and Amazon, those two cross-device, cross-platform, cross-operating systems ecosystems that are well-positioned to leverage the power of voice commerce to keep their connected ecosystems sticky and to keep innovators eager to create new skills to keep them that way.

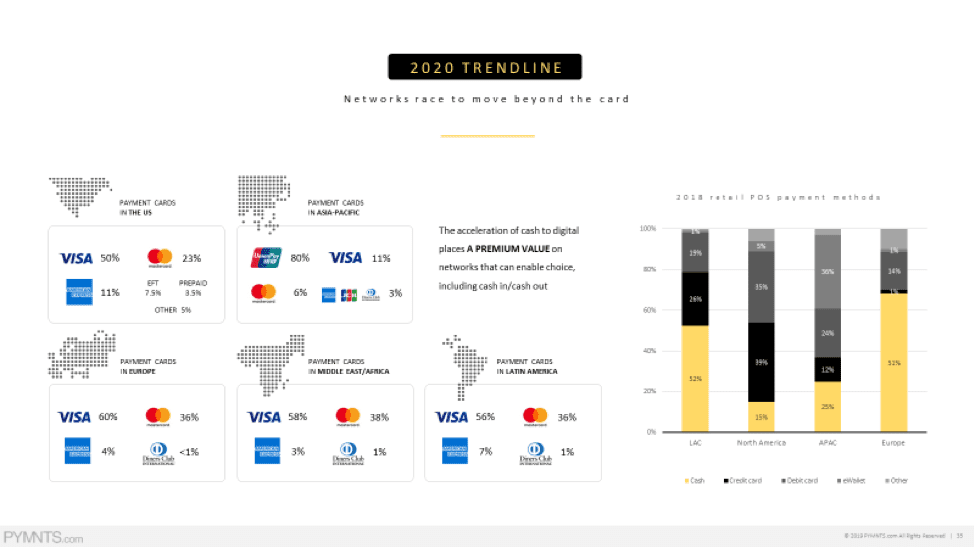

2020 Trendline Seven: The Enduring Power Of The Card Networks

Visa and Mastercard exist today because they innovated the transformation of analog payments to digital six decades ago (Visa) and five decades ago (Mastercard).

Consumers who once only used cash, checks and store accounts at retail stores could use a plastic card with a line of credit attached to it to shop at any store that accepted it. Thirty years ago, Visa ignited the debit card, which gave consumers the ability to buy things with funds in their bank accounts.

Over the last decade, those same credentials that were issued by their banks to make shopping in stores more efficient have also made online commerce possible. Tokenizing and provisioning those same credentials into mobile wallets now powers mobile contactless payments across devices and mobile operating systems around the world.

In the decade to come, the global card networks will also play an important role in powering the connected economy as they move beyond the card to tokenize any kind of payments credentials across any network and between any endpoint – including in developing economies, where card credentials are lacking today.

Critics of the card networks have been calling for their demise over the last decade, as economies without cards or card acceptance emerge as the next wave of digital payments transformation – and as domestic schemes have emerged all over the world to enable real-time movement of funds from account to account, without the need for card rails.

Yet they have all underestimated the difficulty of operating a secure and compliant global payments network at scale, as well as the willingness of the card networks to partner with and enable new payments experiences for innovators who view those networks as platforms to enable specialized use cases.

Today, Visa and Mastercard partner with innovators globally to enable the instant issuance of credentials to power installment payments at the point of sale, to turn funds in bank accounts into virtual debit cards for transacting online and across borders, and to leverage global remittance providers in moving funds instantly between senders and receivers. With China as an exception, it’s safe to say that every digital wallet in every country where Visa and Mastercard is accepted will also have a Visa- or Mastercard-issued credential. And the card networks will continue to work with merchants worldwide to increase their acceptance, as well as with innovators to remain relevant in the developing parts of the world, where consumers and merchants have fallen in love with mobile payments and often don’t rely on traditional cards for transactions.

What Could Bend, And Shake Up, The Trendlines

The next decade, like this one and those in the past, will face a number of threats that could derail or slow the journey to the connected economy future that I strongly believe is before us.

At the top of that list are the regulators, who seem quite driven to punish, and rein in, Big Tech and some FinTechs for getting too big for their britches. Maybe they have a point in some cases, but they don’t give these companies much (if any) credit for delivering all of the great innovations that have moved us from a largely inefficient analog economy to one that has created unprecedented sources of value for consumers and businesses all over the world.

The Big Tech bashing – driven not by complaints from consumers, but by many of the same media pundits who idolized them a decade before – could only make it harder for all innovators and innovation to flourish.

For instance, if the regulators are crawling all over Google for its potential Fitbit acquisition, then imagine the reaction if a larger and more strategic move were contemplated by Google, Amazon, PayPal or any of the Big Tech/FinTech innovators – even if the outcome of the action were demonstrably better for the consumer. Regulators can’t seem to reconcile themselves to the fact that taking actions that might make one Big Tech player weaker could also end up making other Big Tech rivals stronger. Consumers, with their actions, seem best suited and in the most relevant position to decide who gets their business – and, as a result, who survives or dies.

Consumers are always a threat to the pace at which we transition to a connected economy since they are the ultimate litmus test for what makes sense. Consumers have to trust that the new is better and safer than the old – and must get a pretty rich value proposition to move from what works well today to something different.

Part of what erodes consumer trust is bad behavior by those who want their business – and their trust. Facebook is the poster child for that over the last several years, which is why its prospects for Facebook Pay seem limited, and why Libra is simply dead.

Speaking of bad: Bad business models erode investor trust, which, in turn, destroys the business and sours future opportunities for others. WeWork is the prime example for that, as are the thousands of venture-backed companies that could only make a go of it so long as there was a big checkbook funding their losses – where value delivered was not sustainable, nor was it the basis for building a strong, viable business.

Perhaps the biggest threat facing everyone over the next decade is the potential obsession over the next big thing – the shiny object that looks good and makes it past someone’s screen in an organization, but consumes far too many resources for far too long before it is declared dead.

Or perhaps it is never declared dead, in hopes that someday, somehow, it will get its due.

So, What’s Next?

Over the last decade, about this time of year, I’ve defied the advice of one of my economist colleagues who says to never make a prediction that can be disproved in your own lifetime. Instead, I’ve put it all out there and shared my thoughts on how I see the next year evolving. I think I’ve had a pretty good track record of correctly calling a lot of those shots. Not because I have a secret crystal ball or superpowers, but because so often, the industry, pundit and media consensus isn’t based on an intellectual framework with which to assess the chances of success or failure in a complex ecosystem like payments. It’s one where platform economics rule, scale matters and even the best ideas may never get enough critical mass to succeed.

The seven trendlines I have laid out are rooted in that framework, as well as in the hundreds of conversations I have had with CEOs and innovators all over the world this past year. I believe that a shift to a connected economy is inevitable, and that it will happen faster than we think.

This connected economy won’t take 10 years to realize, and it will be powered by payments that will be largely invisible, but imminently powerful in shaping how commerce happens over lifetimes.

The role that each of you plays in shaping this shift will be up to you – and it will be fascinating to observe. I can’t wait to connect the dots that are laid in the months and years to come.