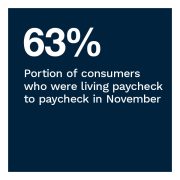

With a new year on the horizon, setting financial goals is top of mind for many U.S. consumers. The past 12 months have been a financial roller coaster, as inflation continues to weaken consumers’ spending power. In November, 63% of U.S. consumers were living paycheck to paycheck, about the same as last year but a 3 percentage point rise from October, according to PYMNTS’ research.

With a new year on the horizon, setting financial goals is top of mind for many U.S. consumers. The past 12 months have been a financial roller coaster, as inflation continues to weaken consumers’ spending power. In November, 63% of U.S. consumers were living paycheck to paycheck, about the same as last year but a 3 percentage point rise from October, according to PYMNTS’ research.  High-income consumers have seen the steepest increase in paycheck-to-paycheck status, jumping 4 percentage points in the past month to 47%.

High-income consumers have seen the steepest increase in paycheck-to-paycheck status, jumping 4 percentage points in the past month to 47%.

In fact, paycheck-to-paycheck consumers are less likely to be stable savers and more likely to lack savings and saving capacity. Our data shows that living paycheck to paycheck is a strong differentiator in the likelihood of having clearly defined financial goals. More than half of those with issues paying monthly bills have unclear short-term or long-term financial objectives.

Our data also finds that 57% of paycheck-to-paycheck consumers think high inflation has diminished their capacity to reach their long-term financial goals. Compared to a year ago, 32% of all consumers reported a decrease in the portion of their paycheck they are able to save, while 42% of struggling paycheck-to-paycheck consumers say the same.

These are just some of the findings detailed in this edition of “New Reality Check: The Paycheck-To-Paycheck Report,” a PYMNTS and LendingClub collaboration. The Financial Goals Edition examines the motivations behind consumers’ ability to save and plan for large expenses, as well as their long-term financial goals and expectations.  The series draws on insights from a survey of 3,895 U.S. consumers conducted from Nov. 4 to Nov. 22, as well as analysis of other economic data.

The series draws on insights from a survey of 3,895 U.S. consumers conducted from Nov. 4 to Nov. 22, as well as analysis of other economic data.

More key findings from the study include:

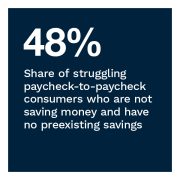

• One-third of consumers are currently not saving any money, with 60% of these consumers also saying they have no pre-existing savings. Paycheck-to-paycheck consumers are half as likely to be stable savers and seven times more likely to have neither savings nor saving capacity than other financial lifestyles. At 48%, paycheck-to-paycheck consumers with issues paying their monthly bills are the most likely to not be saving and to have no savings, compared to only 15% among those living paycheck to paycheck without issues paying bills. Meanwhile, 41% of paycheck-to-paycheck consumers living without difficulty are sporadic savers.

• Financially struggling consumers are the most likely to lack both long-term and short-term financial goals. PYMNTS’ research finds that 36% of all U.S. consumers have not identified short-term financial goals, nor have 38% defined long-term objectives. Consumers living paycheck to paycheck with issues paying their bills are the most likely to lack clear short-term and long-term financial objectives, at 57% for each type of goal.  Among consumers living paycheck to paycheck without difficulty, 37% do not have short-term financial objectives and 40% lack long-term goals. For those not living paycheck to paycheck, less than one-quarter lack clear short-term or long-term financial goals.

Among consumers living paycheck to paycheck without difficulty, 37% do not have short-term financial objectives and 40% lack long-term goals. For those not living paycheck to paycheck, less than one-quarter lack clear short-term or long-term financial goals.

• The most common reasons that consumers save for the long term is to plan for retirement and to cover unexpected emergencies. Saving for retirement is the main reason consumers set a long-term financial goal, with 33% citing this as their most important motivation. Building up emergency savings is the second most common reason, yet only 11% cite it as their most important motivation. Repaying debt, cited by 14% of consumers, is the second-most important motivation for setting long-term financial plans. Financially struggling consumers are the most likely to cite paying off debt as the most important long-term goal, at 24%, compared to 17% of consumers living paycheck to paycheck without difficulty and only 7.8% of those not living paycheck to paycheck.

To learn more about how inflationary pressures will impact financial planning among paycheck-to-paycheck consumers, download the report.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More