Credit unions may consider pausing but perhaps not completely foregoing cryptocurrency offerings as the sector emerges from recent scandals.

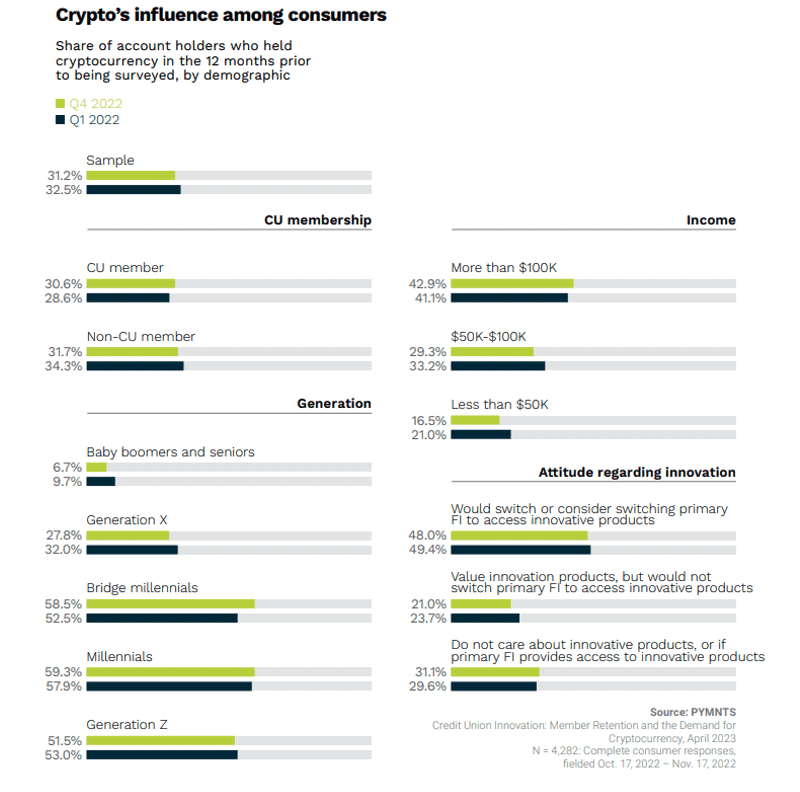

FTX. Gemini. Binance. With now-household names of crypto exchanges and funds having crammed headlines, it’s no wonder that U.S. consumers publicly seem to be backing off from cryptocurrency investments. This sentiment is echoed in the latest PYMNTS/PSCU collaboration, “Credit Union Innovation: Bridging the Cryptocurrency Divide,” where surveyed consumers showed less interest in crypto in the last quarter of 2022 than they did in the first.

Muddying the waters is crypto’s volatility, as some digital currencies such as bitcoin are seeing record trading while other sector firms such as Gemini and Coinbase are announcing significant layoffs. Additionally, since the collapse of Silicon Valley Bank (SVB) and Signature Bank, many crypto companies have been left looking for U.S. bank backing.

Credit unions have so far been hesitant to hold crypto at the same rate as some of their other financial institution competitors. When surveyed in Q4 2022, 66% of CU executives were not interested in offering crypto products due to volatility concerns. And while caution may be warranted when it comes to decisions on where to make innovative investments such as crypto ownership offers, it comes at the expense of possible customer retainment.

Previous PYMNTS research noted that 43% of millennial credit union members own crypto, although if their CU does not offer crypto services, they carry accounts at other institutions. However, 19% of CU members are very or extremely interested in their primary FI offering crypto services. And though public sentiment has waned with crypto’s downturn in 2022, one out of three U.S. consumers still own some amount of the digital currency.

In an interview with PYMNTS, Dr. Yan Zhang, co-founder of Web3-native payment aggregator Pelago, explained why the overall crypto sector may simply be in a temporary flux as lawmakers debate regulation.

“[Lack of regulation] has put the entire industry into chaos status,” Zhang said. “The instability of the regulation is really harming the industry. From my perspective, no decision is worse than bad decisions. It will take time to debate, but the industry is looking for certainty — these things are allowed, these things are not allowed, these things are temporarily not allowed.”

Meanwhile, there are more tangible signs that crypto may not be finished. In New York State, lawmakers are considering a bill introduced earlier this year allowing consumers to pay state agencies with the digital currency. Overseas, two French companies are piloting a program in which crypto is enabled as a payment choice in-store meant for broader use if proving successful. Swiss government-owned bank PostFinance got into the cryptocurrency business earlier in April after partnering with Swiss digital bank Syngum to offer customers “a range of regulated digital asset banking services.”

It’s understandable why credit unions may be hesitant to handle crypto at the present moment. However, it may be useful to look at the digital currency’s continued uptake by governments and foreign FIs as these hiccups pass and regulations surrounding the currency come more into focus. As the dust settles, crypto features may yet prove to be a worthwhile loyalty-building investment.