Health concerns and reduced access to brick-and-mortar locations prompted a large portion of consumers to shift their banking from in-person to online in 2020, with consumers paying bills, depositing checks and opening bank accounts without ever stepping inside a physical location.

Even branch loyalists adapted to the digital evolution, with 26% of them using online banking more and 23% increasing their mobile banking usage. It looks as if the digital shift largely will be permanent, as PYMNTS research indicates that 75% of those who migrated to digital banking channels plan to keep using them indefinitely.

What has not changed during this unprecedented transition is the need for consumers to feel a personal connection with their banks as a basis for trust and loyalty. Research shows consumers are craving a level of personalization in their banking that signals unmet needs, and the share of customers who say they trust their banks has dropped sharply from only two years ago. This may indicate where the digital channel is failing some consumers by overlooking the human touch, running the risk of forcing consumers to choose their banks based on price alone. It represents a major opportunity, however, for traditional banks to gain ground by infusing their digital experiences with humanity and personalization to create strong relationships, build trust and drive vigorous growth.

The following Deep Dive examines the progress of digital and mobile banking adoption from the consumer perspective and how banks can personalize their digital platforms to enhance customer experience, thereby gaining a competitive edge and growing their customer base.

Physical Branch Locations Are Closing

The closure of physical branches around the globe in 2020 resulted in a dramatic digital shift in banking, but not all consumers were quick to embrace this change. One study found that markets such as China, Mexico and Saudi Arabia contain the largest shares of consumers who fit the persona of tech-savvy risk takers eager to engage with digital and mobile platforms. On the other end of the spectrum, the study showed that the largest groups of customers in Canada and Germany favor human interaction and avoid technology whenever possible.

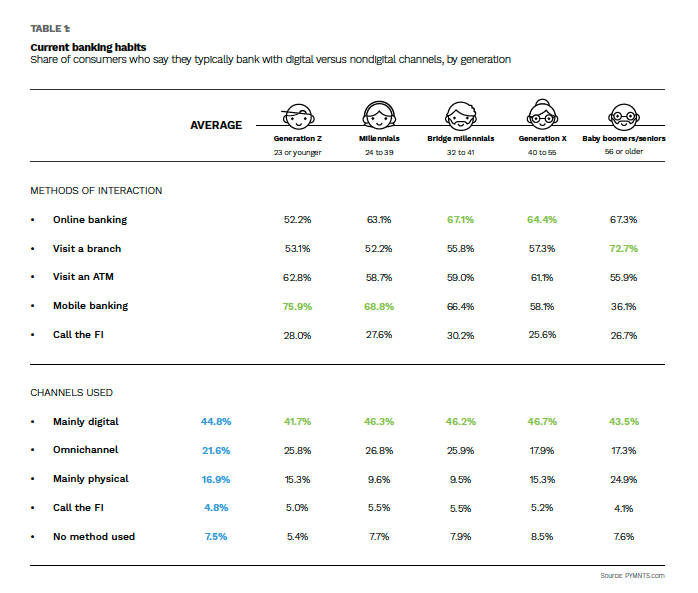

A PYMNTS study showed a generational divide in comfort levels with various banking channels. While all demographics use mainly digital channels, Generation Z and millennials prefer mobile banking apps, bridge millennials and Generation X favor online banking, and baby boomers and seniors prefer to visit a branch. Many consumers still want the option to visit branches, and PYMNTS’ research shows that people who use digital banking tend to combine it with in-person methods. Some people enjoy the human interaction or feel safer providing their personal information to a live teller.

A growing number of banking executives, however, believe the traditional banking model may become obsolete soon, giving way to a fully digital ecosystem. This poses a risk as a lack of personal connection could reduce banking to a simple commodity, in which price alone will determine success. A December study found that consumer trust in banks is faltering, with only 29% of customers trusting their banks to have their long-term financial well-being in mind, down from 43% two years ago.

The good news is that the changing landscape offers an opportunity for traditional banks to forge a personal connection with their customers to regain their trust, keep their loyalty and provide the personalized services they crave.

Digital Banking With a Human Touch

To better serve customers, banks must consider each client individually. A Chase survey revealed that customers want their banks to deliver personalized information and tools that will better inform their spending and savings habits. This was particularly true among members of Gen Z, with 79% of these respondents saying they want more personalized offers or information from their banks to help them meet their financial goals and save money at their favorite retailers. Forty-one percent of all respondents want a more personalized banking experience, and 48% believe that personalized data on their spending could help them boost their savings. Consumers clearly see the value of digital money-saving tools, and meeting customer demands has been shown to increase loyalty — and profitability.

Banks can use the data they already have to shape the customer experience. Predictive insights allow financial institutions (FIs) to anticipate customer behavior and connect more intimately with account holders. Research suggests that an increasing number of consumers show interest in targeted promotions, custom coupons and tailored recommendations. Strategies such as emails, push notifications and videoconferencing can help where human interaction is lacking or impossible. Personalization of the digital banking space contributes to a longer customer life span, increases revenue for the issuing bank and aids in the adoption of new technologies.

Chase, for example, offers a mobile app feature called Snapshot, which relies on a combination of advanced algorithms, artificial intelligence (AI) and machine learning (ML) to deliver a daily digest of a customer’s transactions and financial trends. It also recommends actions to the user, such as paying bills or setting autosave functions to achieve personal goals.

Obtaining and leveraging such data requires customers’ trust to begin with, so it is vital for banks to optimize the customer experience with digital interactions now. Banks that focus solely on digitization may succeed in developing effective offerings but may fail to engage customers personally and lose them in the long run. Banks that imbue digital experiences with humanity and personalization, on the other hand, can help ensure their lasting place in a digital-first future.