Disbursements Satisfaction Report 2020: Monetizing Payout Choice

Introduction

Consumers have been using internet technology for everything from nonessential health services to ordering from restaurants in the last few years, especially shopping more frequently online for retail products and groceries. The COVID-19 pandemic has accelerated this shift to digital, creating the need for a wide range of digital financial solutions that offer immediate, well-known and tailor-made services.

Instant payments are one of these solutions, allowing companies to digitally transfer funds 24/7 year-round. Consumers and other businesses can access their tax refunds, benefits, freelance income, insurance claims, dividend payments and other disbursements within 30 minutes of being paid — sometimes even within seconds. The funds can then be deposited into any type of account, including a bank account, prepaid card or digital wallet.

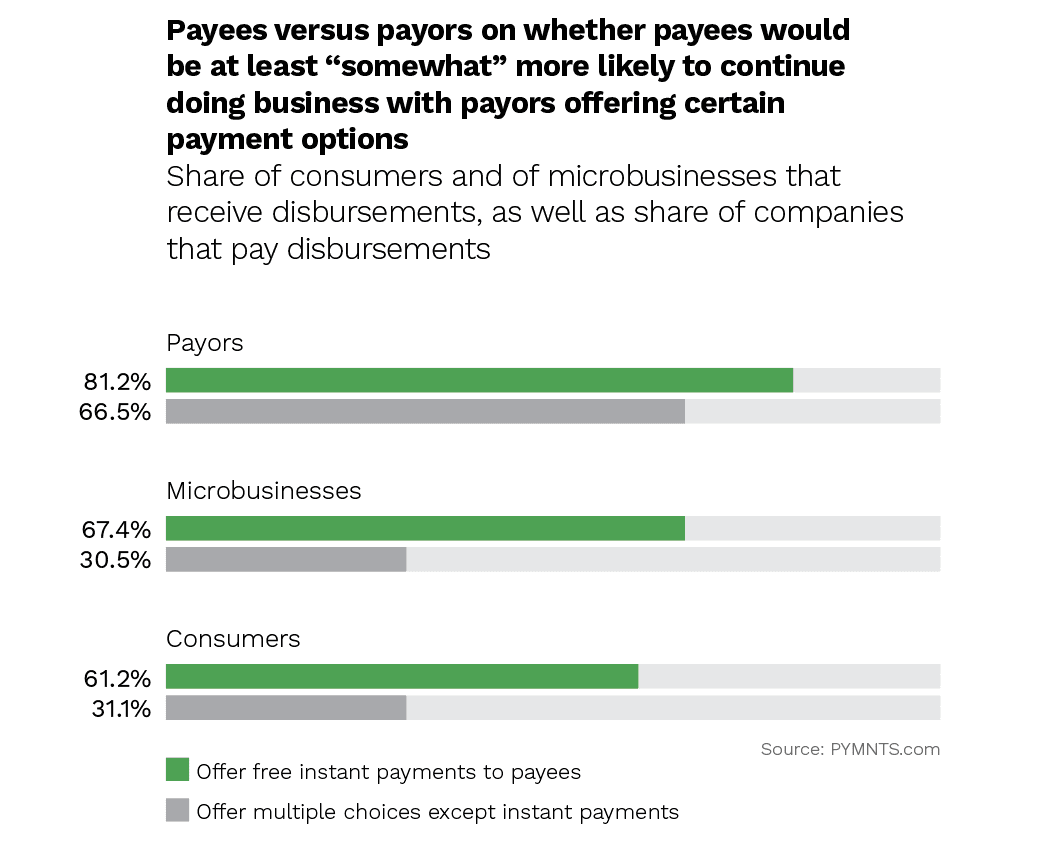

PYMNTS has found that more than 60 percent of consumers and microbusinesses that receive disbursements — known as “payees” — say they would be more willing to continue a business relationship with companies — or “payors” — that offer free instant funds access, but only 30 percent would continue doing business with a firm that did not offer this payment option. Payors know this but greatly underestimate how much payees value instant payments.

Most United States payees cannot access their funds immediately. Only 13 percent of consumers and 8 percent of microbusinesses get their money through an instant payment to a debit card, credit card, digital wallet or prepaid card. Checks and bank account deposits can take several days to settle yet continue to serve as the main disbursement method. The lack of access to instant payments not only goes against consumers’ preferences but jeopardizes the livelihoods of those who are living paycheck to paycheck. It also limits the growth possibilities of microbusinesses that need funds to acquire new clients and to invest in their operations.

Payees also perceive that they have limited choices, a perception that extends beyond lacking instant payment access, even though payors say they offer choice for most of the disbursements they send. This “choice gap” is perhaps one of the most interesting findings of our study and is particularly notable for payments that are made using point-of-sale (POS) channels, such as insurance, lending and product purchase-related disbursements. Payors may offer payment options in these cases, yet payees may not necessarily have access to them or see them as real options. Choice is ultimately in the eye of the receiver.

All the evidence suggests that payees want choice and highlights the existence of demand for instant payments. One question to resolve is who bears the cost of enabling the service. Three times as many payors as payees said they would be willing to pay a fee to receive or enable instant payment access, yet most payors believe that charging a fee would not impact payees’ willingness to continue working with them. Those payors operating in sectors where the costs of switching to a competitor are low, however, recognize that they may have to make instant payments available for free.

These are some of the takeaways of PYMNTS’ Disbursements Satisfaction Report 2020: Monetizing Payout Choice, a collaboration with Ingo Money. We surveyed more than 5,000 U.S. consumers and 500 microbusinesses that receive disbursements, as well as 600 companies of all sizes that make disbursements. We gathered their views on payout options, instant payment adoption and their willingness to pay to receive or enable instant payments. We also identified existing market gaps across specific disbursement categories.

This is what we found.

Key findings

We found that only 31.1 percent of consumers and 30.5 percent of microbusinesses that receive disbursements would be at least “somewhat” more likely to continue doing business with a firm if it did not offer to pay them instantly. Payors underestimated payees’ preference for instant payments, however, with 66.5 percent of payors believing that payees would continue working with them even if they did not offer to send their payments instantly.

This gap between payees’ preferences and payors’ perceptions of those preferences could be explained by the relatively limited possibilities that consumers and microbusinesses have to take their business to a competitor that offers instant payments. Our survey supports this argument as only 11 percent of payors that used instant payments within the last twelve months said they make instant payments available to keep their payees’ business. This ranks as the least important reason for offering instant payments. Convenience and payees’ preference for instant payments were the top two explanations for enabling instant access to funds, cited by 65 percent and 57 percent of payors, respectively.

The portion of consumers receiving instant payments has plateaued over the past 12 months, despite the growth in both the number of consumers that receive payments and the number of disbursements that each of them gets. Just 13 percent of consumers said they currently receive their disbursements instantly.

Investment-related payments, such as dividend payments, investment account withdrawals and annuity withdrawals, have the lowest instant payment penetration: Less than 5 percent of consumers report they can access these types of funds instantly. This raises concerns, considering that investment-related payments are the second-most important consumer disbursement category among private disbursements, with 28 percent of individuals receiving them and with that number almost tripling between 2018 and 2020.

The situation for microbusinesses is more dire: Only 8 percent of them say they can access their disbursements instantly today. Instant payment availability is particularly low for income- and earnings-related payments at less than 6 percent. More than two-thirds of microbusinesses report receiving these types of disbursements, which include earnings for freelance or contract work (45 percent) and payments for goods and services sold online (32 percent). These disbursements constitute microbusinesses’ lifelines, and lacking quick access to them could be putting the smallest U.S. businesses in a vulnerable financial situation.

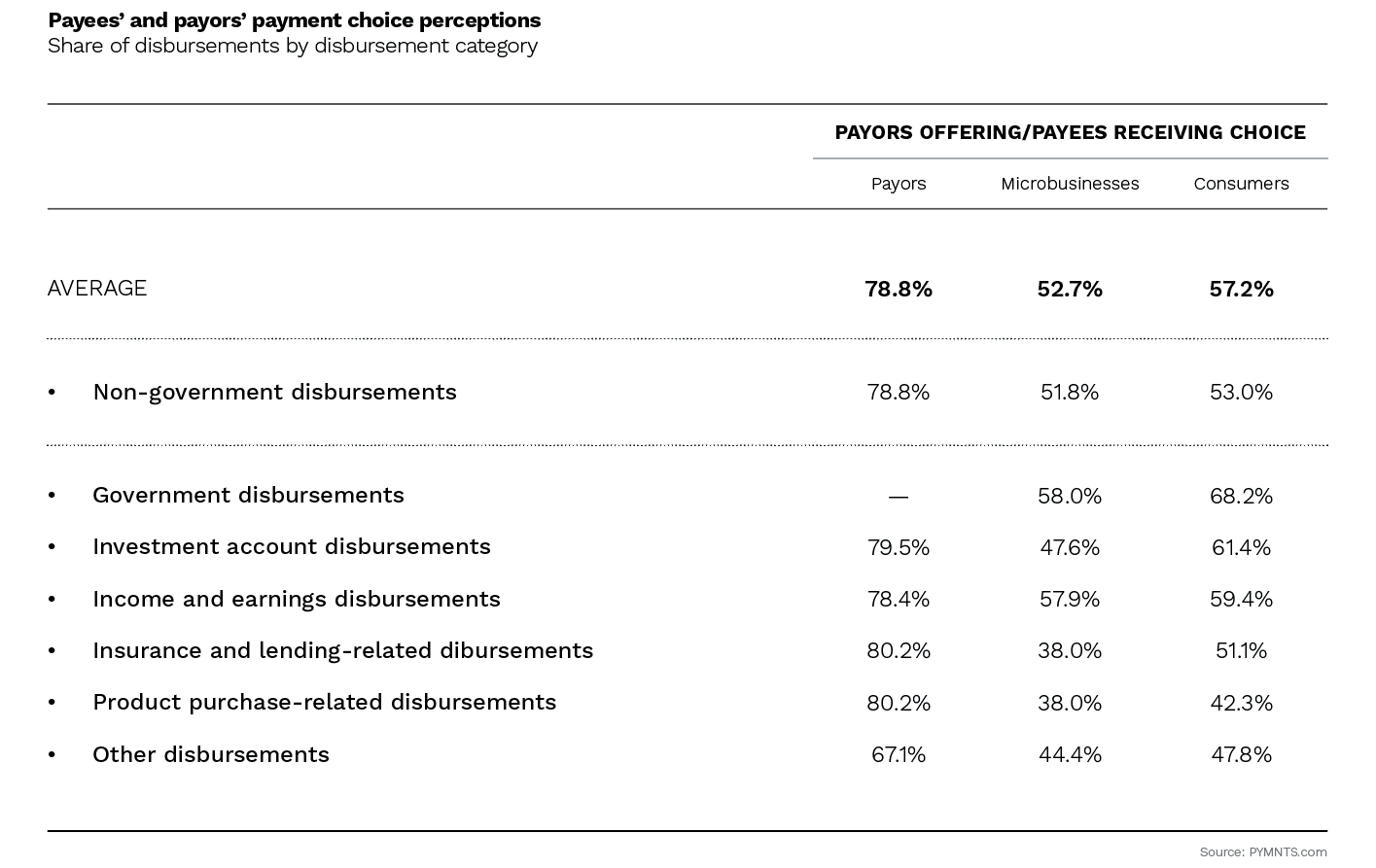

Payees perceive that they have restricted payout choices — particularly when compared to the claims of payors. We found that 52 percent of consumers and 53 percent of microbusinesses said they can choose whether to receive their disbursements through a check, a deposit to a bank account, a credit card payment or any other payout method, yet payors say they give payout choices for almost 80 percent of disbursements.

This choice gap seems to be particularly large in the case of payments made via point-of-sale (POS) channels such as product purchase-related disbursements and insurance and loan payments. Payors say they offer payout choices for more than 80 percent of these types of disbursements, but consumers told us they have payment choice for only 42 percent of product purchase-related payments and 51 percent of insurance and lending payments. Microbusinesses report faring even worse, saying they have choice for only 38 percent of each of these two types of disbursements.

This perception gap is likely explained by consumers being offered several payment options that they recognize as close substitutes and therefore do not consider to be separate payment choices. A consumer who is offered a healthcare claim reimbursement by either check or bank account deposit, for example, could expect to see the money in a bank account three to five business days after the payment has been made — or maybe even later, after administrative work. An alternative explanation is that payors offer choice at the POS, but consumers do not have access to such options. Choice is ultimately in the eye of the payee.

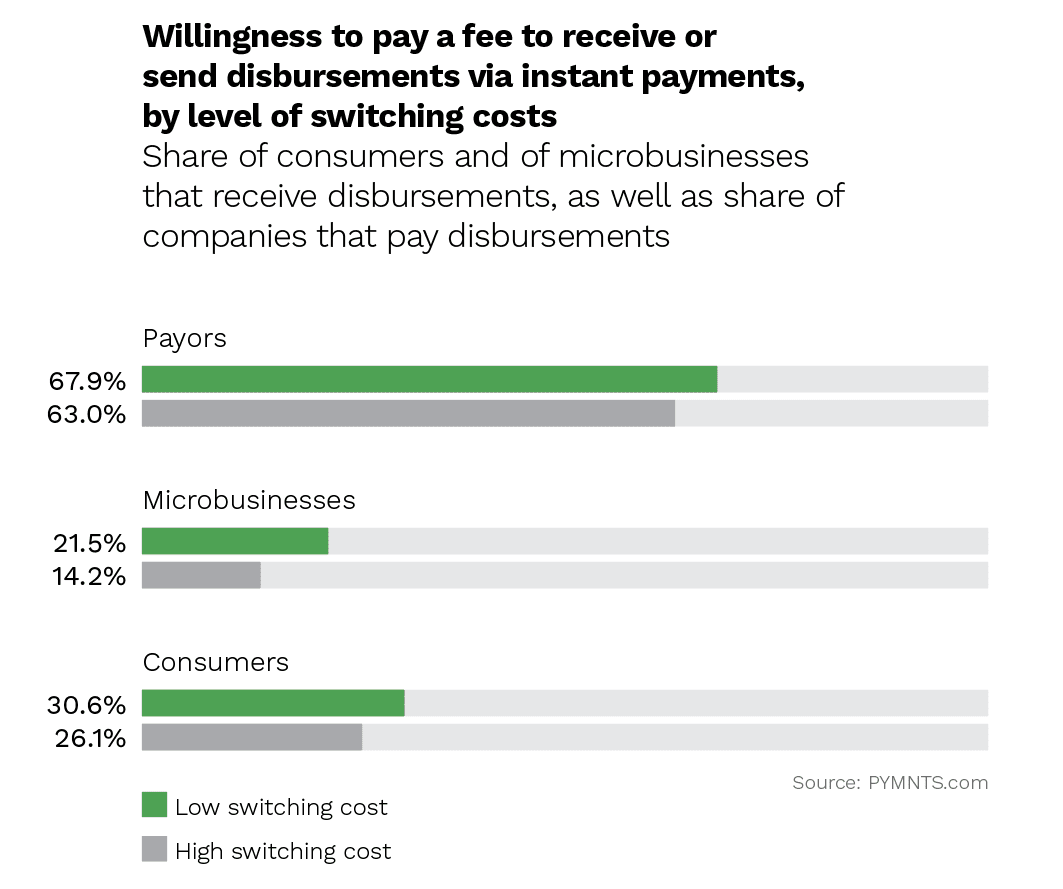

We found that 63 percent of payors said they would be at least “very likely” to pay a fee to make instant payments available to payees. Our research also discovered that 17 percent of consumers and almost 15 percent of microbusinesses would be willing to cover the cost of accessing their disbursements instantly.

The evidence we collected overall suggests payors believe that passing on the cost to clients, contractors and suppliers would not affect their businesses. Approximately 80 percent thought their payees would be more likely to continue a business relationship with them if they offered instant payments for free, yet 75 percent said this would also be the case if they were to charge their payees a fee to access their payments instantly.

Payors in markets where consumers and microbusinesses face relatively lower switching costs seemed to be more willing to pay a fee to make instant payments available. Almost 68 percent of payors sending insurance, loans and investment disbursements said they would be willing to pay a fee to send their payments instantly to the individuals and microbusinesses with which they do business as opposed to 63 percent of payors in high-switching-cost industries, such as those involving income and earnings.

We also gathered payees’ interest in using new technologies to personalize their payment experiences and make them more convenient.

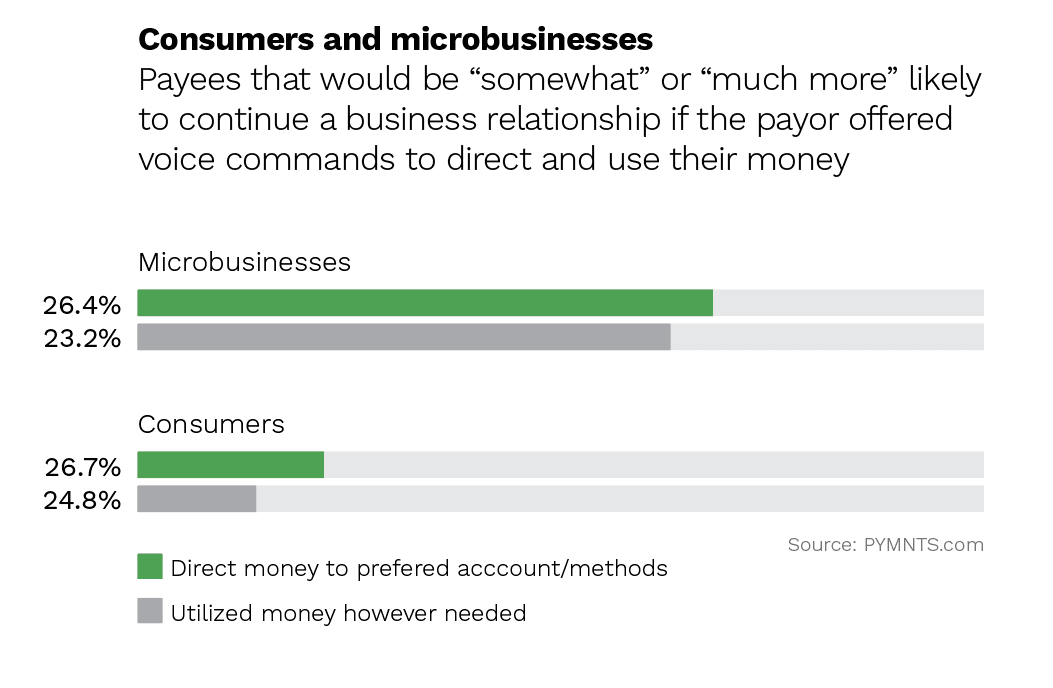

More than one-quarter of consumers and microbusinesses said they would be more likely to continue a business relationship with payors that offer voice commands to direct their disbursements to their preferred bank accounts, credit cards, debit cards or digital wallets. We also found that more than 20 percent of payees would be more likely to continue a relationship with a sender that offered voice commands that allowed them to use their money as they pleased, including paying their bills, placing it in different investment products or sending money to family and friends.

Interest in these new technologies is particularly high among tech-savvy consumers, such as bridge millennials (consumers between the ages of 32 to 41) and millennials (consumers aged 24 to 39). Around 37 percent of the former and more than 35 percent of the latter say they would continue a business relationship with a company that offered voice commands to help direct money. This is also true of 31 percent of younger Generation Z consumers (aged 18 to 23) and older Generation X consumers (aged 40 to 55).

Conclusion

The recent pandemic has accelerated the need for immediate, ubiquitous and tailor-made financial services. Instant payments fit these three criteria by allowing payees to receive disbursements around the clock, enabling them to use their money however and whenever they want to. Both consumers and microbusinesses highly value instant payments, and many of them would be willing to pay to access them. Nearly nine out of 10 payees, however, cannot access their disbursements immediately.

This market gap can be explained by the fact that payors underestimate how important instant payments are for payees. Payors also seem to consider that their clients, contractors and suppliers would generally be willing to continue doing business with them if they did not offer this payment option or if they were to charge for access to it. Our findings suggest, however, that firms competing in markets with low switching costs, such as the insurance and investment industries, recognize that they may have to offer instant payments and make them available to payees for free.

This would not only give more payees access to much-needed instant funds but would also increase the relatively limited payout options that consumers and microbusinesses perceive having.