Where there’s smoke, there’s fire.

The signals smoldering from subprime loan delinquencies that the paycheck-to-paycheck economy is in trouble.

Data from credit reporting giant Equifax, and as relayed by The Wall Street Journal, show that individuals with relatively lower credit scores are, increasingly, delinquent on a broad range of loans, spanning car loans, credit cards and personal loans. The subprime borrowers, generally defined as those with credit scores below 620, are finding it harder to meet their monthly loan obligations.

A few data points from Equifax suffice to illustrate the trend: In March, 11.3% of subprime borrowers’ personal loans and lines of credit were at least 60 days delinquent, and 11.1% of credit cards wielded by this cohort were 60 days past due. That compares unfavorably with the respective 10.4% and 9.8% rates seen only a year ago.

Financial Health — Precarious

Turns out the health of the U.S. consumer, at least when it comes to managing credit, is a bit more precarious than had been thought. Blame inflation, of course — and the pressure is so great that delinquencies are nearing pre-pandemic levels, which means we’ve basically round-tripped back a few years, and the cash cushions of stimulus payments and tax credits are proving to be limited lines of defense.

Since the majority of consumers live paycheck to paycheck — 62% as per PYMNTS’ and LendingClub’s latest estimation — inflation hits hard, and means that there is an ever-tenuous balancing act across all income levels when it comes to managing cash flow.

But: We’ve also found that paycheck-to-paycheck consumers are three times more likely to have taken on credit card debt than those who do not live P2P (for short). By extension, they have additional carrying costs on the debt, and additional demand on income. The balancing act becomes a high-wire feat.

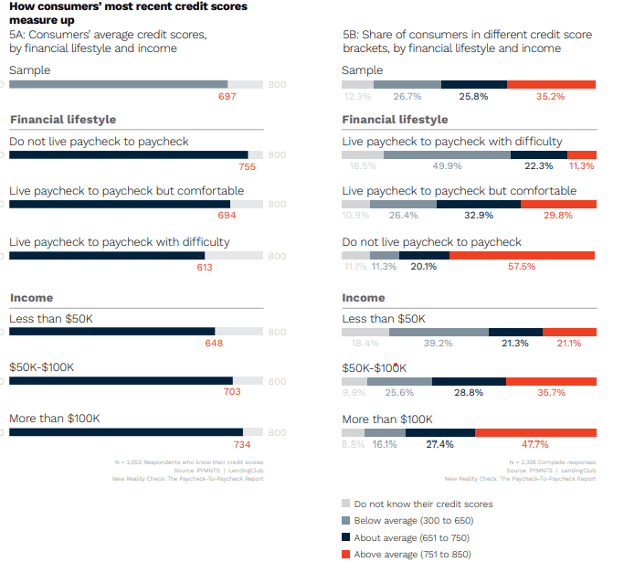

Getting a bit more granular with detail, and a significant percentage of P2P individuals have credit scores below 650, which shows a strong overlap with the subprime population tracked by Equifax. Roughly 49% of the P2P population that finds it difficult to meet expenses also have credit scores below 650; the average credit score here is 613.

Among cardholders living paycheck to paycheck, 34% of those without issues paying monthly bills and 47% of those who struggle to pay their bills “always” or “usually” have a revolving balance.

In a recent interview with PYMNTS, Anuj Nayar, financial health officer at LendingClub, said sticker shock is a continuation of a theme that is only getting louder.

“What we’ve been predicting for months is what is now happening,” Nayar said. “Inflation is affecting everybody’s pocketbook, no matter if you are at the higher or the lower end of the income spectrum.

“There’ll be belt tightening, and there’s no time like the present to step back and take stock. That means focusing on where to cut back on spending, while also building up the cash cushions that are needed to navigate the paycheck-to-paycheck economy.”

The days of forbearance and payment pauses extended by lenders are largely in the rear-view mirror. The cash cushions, we note, will take time to build, and in the meantime, consumers may fall further behind on their monthly credit payments, which can land them in serious arrears, with serious penalties — further damaging their financial health.

Read also: Paycheck-to-Paycheck Consumers 3x as Likely to Take On Credit Card Debt

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More