What The Launch Of Facebook’s Libra Means For Payments

The endless speculation over Facebook’s plans to build a new set of global payments rails and launch a global cryptocurrency comes to an end today with the official launch of Libra.

Or does it?

The announcement today establishes Libra as the foundation for a new, low- or no-cost, global payments and financial services ecosystem, one built by Facebook, to give billions of people access to the “internet of money.” This ecosystem consists of that new network, a new global currency and governance system that puts control of Libra in the hands of an association of financial services and payments industry stakeholders. The ecosystem’s first application is a stand-alone digital wallet, Calibra. The Calibra wallet is a product offered by a stand-alone subsidiary of Facebook by the same name.

Both the Libra network and the Calibra application are expected to launch in the second half of 2020.

I explain how it all works below.

Twenty-eight of the who’s who in payments, marketplaces and venture investing have a seat at the Libra table as Founding Members. They are being asked to contribute their collective experiences in operating global, regulated payments and financial services networks to shape Libra’s charter and frame its governance structure. At some point, they will be asked to kick in a few bucks to fund its operation and get it off the ground. Many of those players are also the very same players that Libra would seem, at first blush, to displace if its vision of creating a new global payments infrastructure really takes off.

That makes today’s launch not the end of a process for Facebook in creating that vision, but the beginning of one that will determine Libra’s future — even perhaps whether it will have a place in the future of how commerce will happen on a global scale.

First, what we’ve been told.

The New Rails — The Libra Blockchain

The Libra ecosystem consists of new rails, the Libra Blockchain, built by Facebook engineers, and the introduction of a new programming language, Move, designed to make it more efficient and more secure for developers to create new payments and financial services applications that run on top of it. The Libra Blockchain code developed by Facebook is being contributed to the Libra Association under an open source license and subject to the governance framework established by the Association.

The open source protocol that Libra uses is Apache 2.0, a permissive license which requires developers to explicitly document and preserve modifications but not release the source code after modifications are made.

Unlike other crypto rails, the Libra Blockchain is a single data structure that records transactions over time and makes the history of those transactions visible to others on the network. Like other crypto rails, the identity of the user is decoupled from the transaction itself.

Initially, the Libra network will be used by Association Members (more on that in a minute) to build or power applications that ride them.

For the first five years the Libra network will be permissioned — open only to Members that meet certain threshold criteria. After that it is Facebook’s vision that the rails will become permissionless and open to all to encourage broad participation, innovation and application development.

And given the nature of the open source licensing protocol, potential forking by others to support global use cases that also use the Libra currency.

The New Cryptocurrency — Libra

Riding those new rails is a new global currency, Libra, whose value is tied to a basket of low-volatility currencies, including the dollar, the pound sterling and the Euro and held in reserve in Geneva, Switzerland. Applications that ride the Libra rails will use the Libra cryptocurrency as the method by which value is exchanged between parties. The intent is for Libra to become a new exchange of value, globally, as more applications ride the network rails and more consumers and businesses use it to transact.

Libra is positioned as a currency that will offer more financial stability than fiat currencies in some developing economies with currency that can be far less stable. Facebook says that it is currently in discussions with regulators, who they claim, are eager to engage in conversations with them about it.

I have no doubt they are.

“At PayPal, we believe in democratizing participation in the digital economy for people from all walks of life and businesses of all sizes. PayPal is pleased to join other leading technology and financial services organizations to form Libra, with the goal of exploring a new, global digital currency, built on blockchain technology.”

– Dan Schulman, President and CEO, PayPal

The New Governance Structure — The Libra Association

A new governance structure will monitor and manage the activities of the Libra network, the reserves backing the Libra cryptocurrency and the applications that ride the Libra Blockchain rails.

The Libra Association, headquartered in Geneva, Switzerland will be governed by a Council and a Board of Directors, led by a Managing Director with a three-year term. Decisions related to the vision, execution, business models and monetization schemes, as well as the roles and responsibilities of all participants, will be discussed, vetted and decided upon by the Council and Association Members.

Facebook has said it plans to play a large role only throughout the remainder of 2019 as the Association gets up and running and additional Members and funding are recruited. After that, Facebook has made it clear that its influence will be equal to that of any other Association Founding Member as the Council, the Board and Managing Director assume control. Some decision-making will require a supermajority — more than two-thirds of Members — others will require only 50 percent, assuming that two-thirds of all Members participate in the vote.

As I mentioned earlier, Association Members, at launch, include 28 of the leading players in payments, venture investing, crypto, marketplaces and NGOs as Founding Members. These Founding Members also constitute the Council. Facebook hopes to increase the number of Members — and therefore the Council — to 100 by 2020.

Association Members are both known and familiar: Mastercard, Visa, PayPal, Stripe, PayU, Andreessen Horowitz, Union Square Capital, Coinbase, Xapo, eBay, Uber, Lyft, Farfetch, Mercado Pago, Spotify, Vodafone among others. Members agree to operate as validator nodes on the Libra network which means that they agree to secure and validate Libra transactions running across it. Operating as a validator node means complying with certain technology and availability requirements, including 24/7/365 availability.

Members, with some notable exceptions, will be asked to contribute $10 million to buy Libra Tokens to confirm their Membership and the voting rights associated with that Membership. The money collected will fund the operating costs of the Association, including the incentives needed to encourage participation. Sources familiar with the matter tell me that no money has exchanged hands to this point. Association Members can increase their standing by making additional $10 million investments in Libra Tokens, up to a threshold. No one Member can control more than one percent of the votes.

Think of the $10 million investment, at least for now, as the price of getting a seat at the table — and the opportunity to understand, and influence, the direction of Libra. It is also apparent that as a side benefit Members get clear, first-hand information on how Libra plans to compete with them now and over time.

Several social impact organizations and NGOs — Women’s World Bank and Kiva, to name two — have also signed on as Founding Members and are part of the 28 included in today’s announcement. They, and others like them including academic and research organizations, will not be asked to contribute funds to participate.

All Members, including NGOs and social impact agencies, are, however, subject to strict membership guidelines, including the ability to meet financial, scale and business stability/business standing thresholds.

Libra assets will be held by The Libra Reserve, which is a decentralized and distributed network of custodians with investment-grade credit rating. Calibra is a digital wallet that stores and moves Libra across the network but will not operate as an exchange.

New Network, Crypto Applications

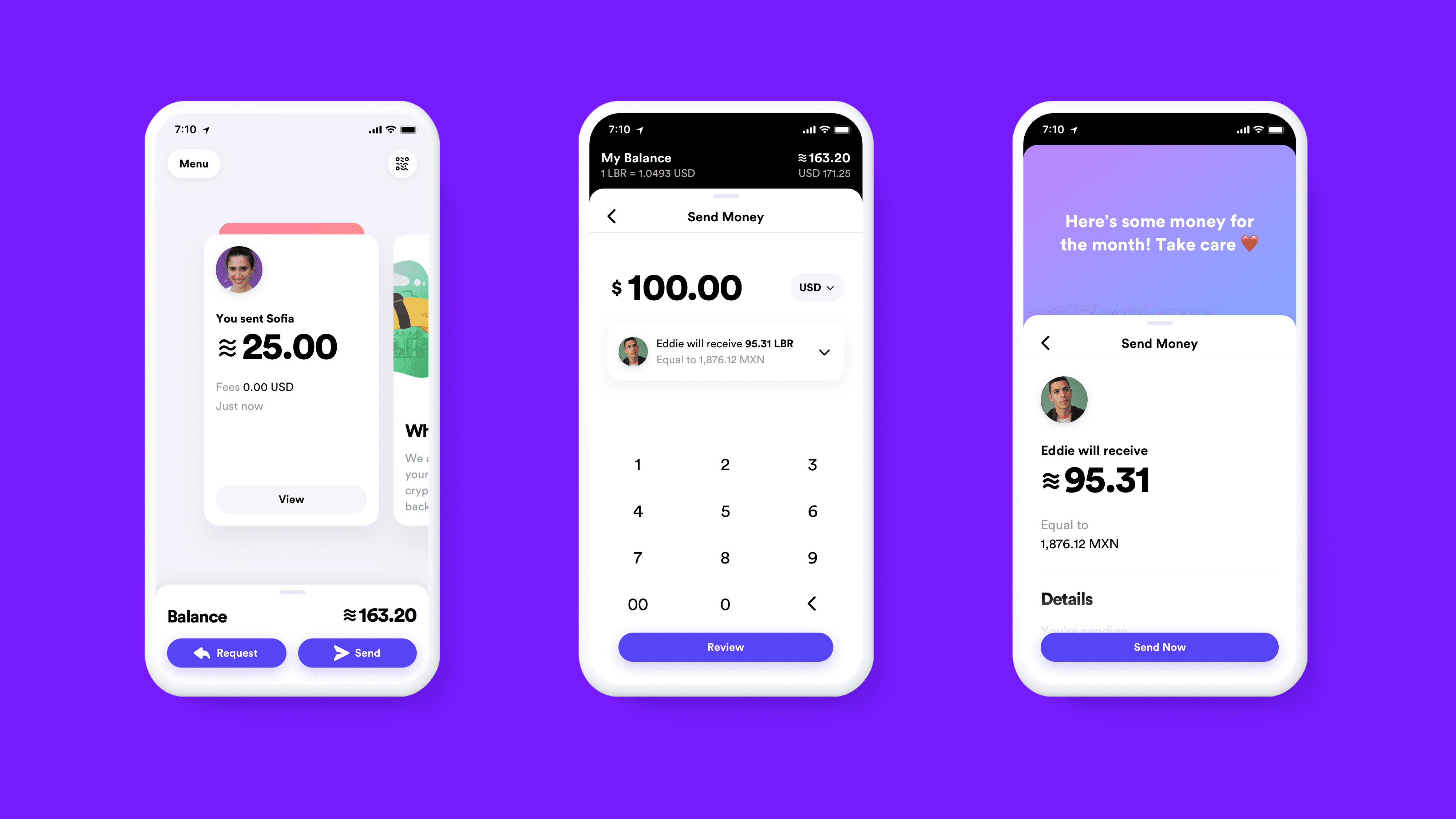

Finally, the ecosystem will consist of new cryptocurrency-based applications that ride the Libra Blockchain rails and use the Libra currency. The first such application, also announced today, is a digital wallet, Calibra, from a Facebook subsidiary by the same name. Calibra is scheduled for release in 2020 and is intended to be the application that will drive the monetization of commerce on Facebook, using the Libra currency.

Calibra will be available across all Facebook properties, starting initially with Messenger and WhatsApp. Users will be able to download the app inside of those platforms and transact with it using the Libra currency. Calibra will also be available for consumers to download in the Apple and Google app store. Calibra is registered as a Money Services Business and is in the process of securing additional licenses.

Calibra was created as a stand-alone app and registered subsidiary of Facebook to avoid the appearance of and the actual inability to comingle data related to payments transacting with data related to social interactions. Calibra data, in the aggregate, will be used by Facebook to comply with AML and other regulatory requirements. With the user’s permission, Calibra will allow consumers to import or export their data to third parties, including their social network contacts from Facebook.

The initial use case for Calibra will be P2P payments, cross-border.

“Tomorrow’s innovation may just be an idea today. We are committed to ensure that the Internet of Everything comes with the inclusion of everyone. By activating partnerships to explore, co-create, and test new ideas, we can cultivate ideas to make inclusion a reality sooner than some may think. This effort embraces that spirit.”

– Jorn Lambert, Executive Vice President, Digital Solutions, Mastercard

New Mission?

The mission statement of Libra is nothing short of bold and inspiring: to give the 1.7 billion people in the world without access to a bank account the ability to have one at no or low cost. It is about, Facebook says, igniting a new commerce ecosystem that will make it as easy for billions of people to send money around the world as it is to send a picture or a video across the internet, but to do it more securely. It is about laying the tracks that existing infrastructure, they also say, is lacking, with today’s global payments and financial services networks.

Libra, and Calibra, as an initial application, Facebook says, will move the ecosystem forward to solve that problem. Judging from the affirmations from many of the initial Founding Members, they seem to agree.

On that, I am not so sure.

Why The Unbanked Are Unbanked

The white paper issued by Libra describing the vision for solving the world’s unbanked problem hyperlinked to a study published every three years by the World Bank that examines that issue across 140 economies. It is called the Global Findex Index, and the 2017 report took on the impact of digital technology, mobile phones and access to the internet on financial inclusion.

Between 2014 and 2017, the report says that 515 million people gained access to an account at a bank, a mobile money account with a telco or other third party. That means that 69 percent of the world’s population now has a bank account or something similar, up from 62 percent in 2014 and 51 percent in 2011. Sixty-three percent of people living in developing economies have access to a bank account of some kind now, too.

That inclusion is the result of banks, telcos, remittance players, card networks, NGOs and innovators collaborating to create access to financial services across regulated and secure rails, and building the critical mass of users to ignite it.

Telcos have ignited mobile money networks like M-Pesa. Payments players like Alipay, Paytm, WeChat and Grab are creating their own domestic and regional mobile money schemes using mobile phones and QR codes to enable consumers to pay local merchants in those markets, save and build credit. Remittance players have opened their networks to third parties to create new payments flows and lower the cost of money transfers by moving more of those flows digital.

The results are demonstrable and compelling, particularly for women and other microbusiness owners who are able to lift themselves out of poverty by being included in the world’s financial system.

Yet 1.7 billion people still lack a bank account, nearly half of whom, the World Bank study reports, live in just seven countries: Bangladesh, China, India, Indonesia, Mexico, Nigeria, and Pakistan. They share a few common characteristics which makes serving them a challenge: They are extremely poor, uneducated and unemployed.

Less than a third have completed high school and 47 percent of them lack employment. They don’t have bank accounts because, when asked, two thirds say that they simply don’t have enough money to put into one. Whatever cash they have, they want available and accessible. These people are living hand-to-mouth, and access to a bank account alone, sadly, isn’t likely to change that fact.

Others do not have a bank account because someone else in their household does — a family of four adults has one bank account into which deposits are made and household finances are managed.

Cash As Currency

In developing markets, the ability to transact digitally means solving for the age-old, two-sided network problem that bedevils any and all payments networks: acceptance by people and businesses of a new way to pay — and an easy way to fund those digital accounts.

In developing economies, that’s cash. As low tech as cash is, it’s trusted by people because they have it, see it, hold it, count it, store it and use it everywhere, and can access it at any time they need.

The success of every successful digital payments network in these economies is, therefore, linked to cash: the ability to deposit cash into a digital account and a way to take it out to spend at businesses that don’t accept any other way to pay.

Or use it inside of a closed commerce and financial services ecosystem that accepts that method of payment for all of the types of payments transactions.

Take Kenya, which, by all accounts, is the poster child for financial inclusion in Africa. M-Pesa ignited in Kenya because it established an agent network of 40,000 locations where users could withdraw cash sent to them by others via those M-Pesa mobile money accounts. M-Pesa was the method of transport, and the account that kept those funds secure. But cash was the method of payment used in those villages by those recipients — and remains to this day.

Take remittances. The vast majority of remittances in developing countries aren’t picked up in cash because receivers don’t have bank accounts, but cash is preferred because it is how business is done.

Take Alipay. Alipay is a closed ecosystem for Chinese consumers who can send payments to people and businesses inside of the Alipay ecosystem — using a fiat currency understood and accepted by all Chinese consumers.

That sets up a rather challenging ignition problem for Libra and Calibra if they are truly aiming for the unbanked, who need any cash they can get, as well as the banked in cash-intensive economies.

People will create a Calibra wallet and send Libra if the person they are sending it to can use it to pay bills, pay people or pay businesses using it.

Or cash it out to spend where it is not accepted — which will be mostly everywhere, for the foreseeable future.

People will create a Calibra wallet and send Libra if they can buy it and put it into their digital wallets. That’s easy provided that person already has a bank account, or a convenient way for cash to be deposited into that account and converted to Libra currency.

Provided, of course, they trust the wallet, network and new global currency called Libra.

The Trust Factor

Igniting the Libra network, the Libra currency and Calibra wallet requires that people feel comfortable buying into using an entirely new global currency backed by an association they’ve never heard of based in a country they’ve probably never visited — and using, at least initially, a digital wallet created by Facebook on one of two platforms that are also part of Facebook network: Messenger and WhatsApp.

That’s a lot for anyone to understand and process, much less someone living in a developing country with limited education, and for whom money — and trust — may not come easily.

A big priority for Libra and Calibra is to establish that trust with those users — and there are a number of ways that can be done. Starting with, perhaps, asking third parties that today pay consumers in cash to, instead, deposit Libra into their Calibra accounts.

For example, Libra and Calibra could approach governments that pay social benefits to people in developing countries in cash and ask them to fund Calibra accounts instead using the Libra currency. The World Bank report says that social benefits paid into a digital account would bring 100 million more people globally into financial inclusion.

Libra and Calibra could also approach private sector employers that make cash payments to workers with the same proposition. That would add another 230 million unbanked workers 235 million unbanked farmers to the mix.

Collectively, that would bring another 565 million people into the ranks of the banked and onto the Libra network with a Calibra wallet, ready to transact using the Libra currency.

A good idea — but perhaps a pretty tough sell, particularly at the same time that other schemes, including all the mobile money schemes that have launched successfully around the world, the card networks and well-funded innovators that are solving for specific use cases in their domestic markets are gaining steam. It is particularly hard to see Libra displacing Alipay or WeChat Pay in China for the unbanked or Paytm in India.

Just because consumers feel completely comfortable using Messenger and WhatsApp today to send and receive messages doesn’t mean they will feel comfortable using them to send their own money to people who absolutely need to receive it.

The Libra and Calibra team understand this, too, and concede that implementing their vision is a long, slow build, perhaps even over “decades.” However, in payments, long slow builds don’t always work to one’s advantage, particularly when part of getting ignition means getting regulators on board who have the power to slow way, way down, or even stop progress.

“Sending money to your friend shouldn’t be harder than getting them an Uber ride home. We’re excited to work alongside the other Founding Members to help bring Libra to life. Libra has the potential to bridge the gap between traditional financial networks and new digital currency technology while reducing the costs for everyone – especially consumers.”

– Peter Hazlehurst, Head of Payments and Risk, Uber Technologies, Inc.

Who Wants A Global Currency?

Libra has taken a page out of the payments industry playbook in setting up its initial charter: assemble an association of key stakeholders and establish a governance system that allows them to control and run it. That framework is what ignited the card networks many decades ago.

The big difference with Libra, and the big change for regulators, is the introduction of a single global currency into the mix, at the expense of domestic fiat currencies. That is where many may push pause, and where the regulators could decide to simply push stop.

It took a little bit of time, but regulators the world over have now agreed that bitcoin, as a global currency, is a non-starter, since no central bank wants to give up control of its monetary supply to a single global currency over which they have no control.

Bitcoin, of course, came with its own set of baggage. Even though Libra will be governed differently, more thoughtfully and responsibly, the issue of a single global currency persists — one that is out of the control of central banks. It may not help that it was an idea conceived by Facebook, even though Facebook has taken great pains to distance itself from having any undue control of the network and the currency. Facebook is not exactly the darling of regulators today — and having the Calibra wallet as the first application running on the Libra network inside of two Facebook platforms may give them pause.

For regulators, and perhaps even many of the Founding Members that today operate regulated global payments rails, the real risk seems to lie in the creation and use of the Libra global currency for transacting across Libra rails.

It’s a concern that recently got the attention of the IMF head, who warned that ceding control of our financial services and payments schemes to FinTech firms, aka Facebook by name and Libra by inference, in her opinion, puts the stability of our financial system at risk. A risk that could become much more pronounced as the permissioned network transitions to a more permissionless state in five years’ time.

Persuading regulators that this risk doesn’t come with a severe downside also comes at a difficult time for Facebook. The WSJ reports last week of Mark Zuckerberg’s email trails around its privacy issues come at the same time that the FTC is about to hand down a sweeping fine, and restrictions, for its data privacy failings.

The Facebook Ecosystem

Facebook sees the Libra network, the Libra currency and the Calibra wallet as an opportunity to monetize its massive user base. A new payments network and a new global currency, it hopes, will be enough to persuade the captive audience of 1.6 billion monthly active users on WhatsApp and the 1.3 billion monthly active users on Messenger to give it a try when sending money to family and friends. If they do, that could create the foundation for a global commerce network inside of the Facebook ecosystem.

Here’s the disconnect, still, for me.

Facebook says that low- or no-cost cross-border P2P payments is its initial use case, as is giving the 1.7 billion unbanked a low-cost or no-cost way to access the financial services ecosystem. I wonder if that’s simply window-dressing in an attempt to gain favor by the regulators — because otherwise, it just doesn’t make any sense.

Many of those who use Messenger for sending messages today have their own money transfer networks in place for sending money to family and friends cross-border. Persuading them to move to Calibra isn’t asking them to switch from Western Union to Remitly, but moving to something that is entirely new, and — at least, as it is currently envisioned — without any way to get cash in and cash out.

As for the unbanked, and for all of the reasons that I just laid out, there are simply too many hurdles for Calibra and Libra to overcome to turn the unbanked into banked consumers, beginning with lifting them out of wrenching poverty. There are even more hurdles to persuade governments and employers to opt into Libra as a funding source for its citizens and workers (at least right now), when there is no easy way to spend it.

That leaves one use case: microtransactions.

It could be that Facebook uses Calibra accounts, and the Libra currency, to pay people small amounts for their data. Facebook doesn’t necessarily want to do that, but regulators are suggesting that Facebook shouldn’t be getting all that valuable consumer data for free (of course, users are getting Facebook for free in return, but that value exchange doesn’t seem to register with the regulators).

In that case, Facebook would become a Calibra funding source, which could be enough of an incentive for consumers to release data to Facebook. That Libra/Calibra ignition strategy would help Facebook both preserve its advertising model, keep the regulators happy and force the creation of Calibra accounts. If nothing else, Calibra and Libra provide an insurance policy if regulators start insisting that Facebook pay for consumer data and make those potentially micro, micro transactions easier. Provided, of course, that consumers have a place to spend their Libra.

Facebook may also be counting on Calibra and Libra to ignite a commerce ecosystem, which they have struggled for years to do. They may be looking enviably at China’s Tencent, a social network and gaming behemoth, which is far less dependent on advertising then they are. Tencent, of course, operates commerce through WeChat, and its users can use WeChat Pay.

Then again, I could be completely wrong that these are the plans. Maybe Facebook and its Association Members really do think that Libra is the solution to the problems of the 1.7 billion people living in extreme poverty without bank accounts and money to put in them. But I just don’t see how a digital currency, pegged to three non-domestic currencies, is going to help.

I was given an opportunity to be briefed by the Libra team in advance of the public announcement, and received materials to review in advance as well. It’s clear that the team has examined this issue from a technology perspective quite thoroughly, and taken on board the lessons learned from the decade-long bitcoin debacle and its attempt to solve the same global financial inclusion problems.

Bitcoin hasn’t ignited as a general-purpose online payment method, despite billions in venture money, and the ecosystem of exchanges, wallets and processors (aka miners) that emerged to support its global payments ambition. The reasons are well known, but at least one of them is a lack of any real governance system — and assorted, and sordid, other problems.

After listening to the thoughtful approach that this team has taken to establishing Libra — the currency, the network and its governance — one is left to wonder where bitcoin might be today had it taken a page from the Libra playbook.

However, that was a decade ago, and 10 years is a long time in the payments world. Over that period of time, the payments and financial services ecosystem has made great progress in addressing the issues associated with moving money between people, cross-border, and in the domestic markets where banking and payments infrastructure is lacking in a safe, secure and regulated way. Could it be better? Of course, and concerted efforts are in place to do that — in a way that consumers are familiar with, know and trust, using the fiat currency that they can spend in the places they shop — in physical and digital forms — in a way that brought 515 million people into financial services ecosystem over the last three years.

So, it’s just not clear to me that a blockchain/global cryptocurrency solution — even one that is as well conceived as this one — is really what’s needed to solve the problem of the 1.7 billion people in the world who don’t have a bank account today, or even that it is likely to be able to do so.

I’m not even sure that’s Libra’s real objective.