Earnings season and PYMNTS’ own data signals the difficulty of keeping wheels on the road — literally.

As economies reopen, many firms are returning to a hybrid model. Travel is returning to (and surpassing) pre-pandemic level. And as we make more trips to the store (in-store pickup is gaining ground), transportation is becoming more essential than ever.

And while the price of gas has receded well off its previous highs, having the actual vehicle has become more expensive than has been seen in years. As with many other forms of debt, auto loans are pricier than they have been in decades. More than 15% of car buyers have monthly payment of at least $1,000 in the fourth quarter of 2022, according to Edmunds. That tally was 10.5% in the fourth quarter of the previous year.

The size of outstanding auto loans has ballooned. The aggregate of those loans from $1.44 trillion in the third quarter of 2021 to $1.52 trillion in the same quarter in 2022, according to the Federal Reserve Bank of New York. Edmunds has also that the interest rate on auto loans was 6.5% in the fourth quarter, up from the 5.7% in the third quarter and up from 4.1% last year.

As to the affordability of it all, Cox Automotive said earlier this month that loans delinquent by more than 60 days increased by 5.3% and were up 26.7% from a year ago. Overall, 1.84% of all loans were severely delinquent, which was an increase from 1.74% in November and the highest rate since February 2009.

Other data points from earnings call commentary spotlight the pressures that confront us in an economy where the majority of us — even high earners — live paycheck to paycheck. Capital One’s earnings call this month revealed that in the latest quarter, auto loan originations were down markedly, at $6.6 billion, down 20% year on year. Auto period-end loans decreased $1.2 billion, or 2%, to $78.4 billion.

Earnings filings show that net charge-offs in the auto segment were 1.7%, up from 1.1% in the third quarter and up from 0.7% in the year-ago quarter. Thirty-day delinquency rates were 5.6%, up from 4.3% in the fourth quarter of 2021. Andrew Young, CFO, said that loan loss provision increases were tied to lower recovery rates. Management has pointed to a normalization of credit performance overall, and this includes autos.

Separately, and in another example, Wells Fargo has seen its auto portfolios declined for three consecutive quarters, and balances were down 5% at the end of 2022 compared to year-end 2021. Meanwhile, originations were down 47% in the fourth quarter compared to a year ago, and stood at $5 billion in the latest period. In materials released by Wells in tandem with earnings, the 30-day delinquency rate was 2.6%, up from 1.8% last year. Net charge-offs in the auto lending segment were 1% of the portfolio, up from 0.4% a year ago.

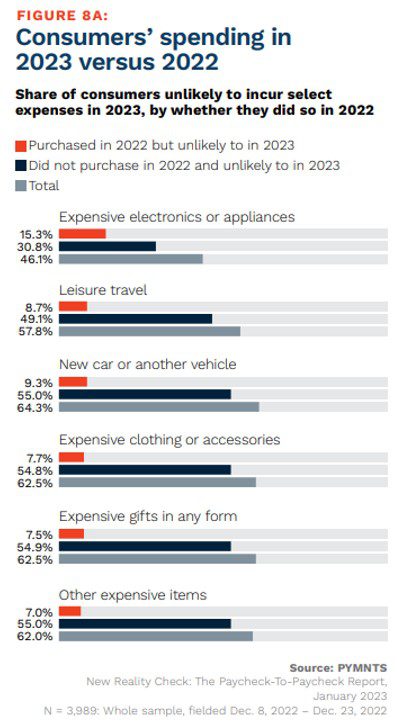

There’s other evidence that the loan originations will stall in the coming months, which will continue to pressure banks and other lenders. In the latest report on the paycheck-to-paycheck economy, done in collaboration between PYMNTS and LendingClub, 64% of consumers live paycheck to paycheck, up from 61% at the end of 2021. More than half of high income consumers, earning more than $100K annually, live paycheck to paycheck. The rough math states that at $1,000 a month, the aforementioned car loans would be 12% of the high earners’ $100,000 gross income — so the car loans of course are even tougher to juggle for the lower income brackets. The chart shows that 64% of consumers, overall, are unlikely to buy a new vehicle in the current year (whether they did so or not last year).

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More