The average U.S. FinTech loses $51 million to fraud every year, and many lose even more. Even so, that figure only begins to capture the heavy toll that fraud can have on FinTechs’ businesses. PYMNTs’ data finds that the true impact of fraud extends far beyond the black and white of the balance sheet.

“The FinTech Fraud Ripple Effect,” a PYMNTS and Ingo Money collaboration, details the myriad ways in which fraud can cut into FinTechs’ bottom lines. We surveyed 200 FinTech executives from across the United States to obtain an inside look at how widespread the fraud issue really is and how broad an impact it can have on FinTechs’ wider operations and end user experience.

This is what we learned.

This is what we learned.

• As FinTechs experience more fraud, they impose more frictions on their account holders. FinTechs that consider fraud costs to be a challenge impose twice as many frictions on their account holders as those that do not worry about fraud.

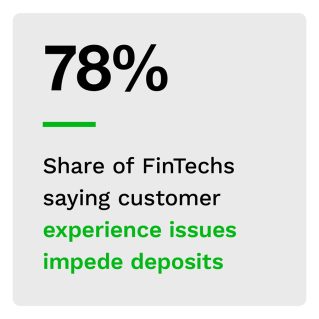

• Nearly all FinTechs say their users have trouble moving money in and out of their accounts, but FinTechs struggling with fraud are more likely to experience these frictions. Poor user experience is the most common friction making it harder for customers to deposit and pay using their funds, and 26% more FinTechs that struggle with fraud report experiencing this friction than those that do not struggle with fraud.

Poor user experience is the most common friction making it harder for customers to deposit and pay using their funds, and 26% more FinTechs that struggle with fraud report experiencing this friction than those that do not struggle with fraud.

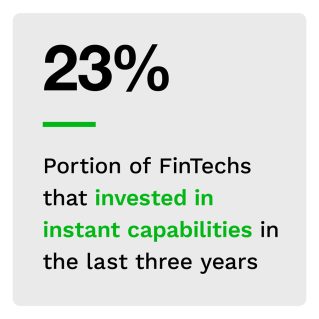

• The average FinTech plans to invest in instant offerings to improve the user experience. Investments in instant cryptocurrency wallet deposits and in-store cardless cash withdrawal options are near the very top of FinTechs’ innovation wish lists, with 31% planning to invest in the former and 28% planning to invest in the latter in the next three years.

These are only some takeaways uncovered in our latest round of research. “The FinTech Fraud Ripple Effect” provides a holistic overview of fraud’s true cost.

To learn more about the real impacts that fraud has on FinTechs, download the report.