AI systems are unique, can process large volumes of data in real time and can “learn” to quickly identify suspicious financial activity. Yet, few FIs leverage this technology in their anti-fraud efforts — only 5.5 percent of them have adopted true AI systems. Instead, FIs’ anti-fraud departments tend to use less-sophisticated learning systems, like data mining and business rule-management systems (BRMS). What’s more, only 12.5 percent of fraud specialists use AI, while 92.5 percent use data mining and 65 percent user BRMS.

AI systems are unique, can process large volumes of data in real time and can “learn” to quickly identify suspicious financial activity. Yet, few FIs leverage this technology in their anti-fraud efforts — only 5.5 percent of them have adopted true AI systems. Instead, FIs’ anti-fraud departments tend to use less-sophisticated learning systems, like data mining and business rule-management systems (BRMS). What’s more, only 12.5 percent of fraud specialists use AI, while 92.5 percent use data mining and 65 percent user BRMS.

So, what is keeping so many fraud departments from investing in the technology they need to help fight cyber fraud?

need to help fight cyber fraud?

In the AI and Fraud Edition of the AI Innovation Playbook, PYMNTS, in collaboration with Brighterion, surveyed decision-makers at 200 American FIs to learn how they leverage AI technology in their fight against fraud — and to provide actionable insights on how FIs can maximize their use of this powerful technology.

The research found that getting management on board with the use of AI can be a big hindrance to its wider adoption. Few FIs currently use AI, but this stands in stark contrast to the attitudes of their leaders toward the learning system.  The study found that 63.6 percent of fraud specialists considered AI an effective means of reducing payments fraud. In comparison, only 28.4 percent considered data mining effective for that purpose, and only 17.6 percent felt that way about BRMS. Simply put, FIs are fighting fraud with some of the most ineffective learning systems available — and they know it.

The study found that 63.6 percent of fraud specialists considered AI an effective means of reducing payments fraud. In comparison, only 28.4 percent considered data mining effective for that purpose, and only 17.6 percent felt that way about BRMS. Simply put, FIs are fighting fraud with some of the most ineffective learning systems available — and they know it.

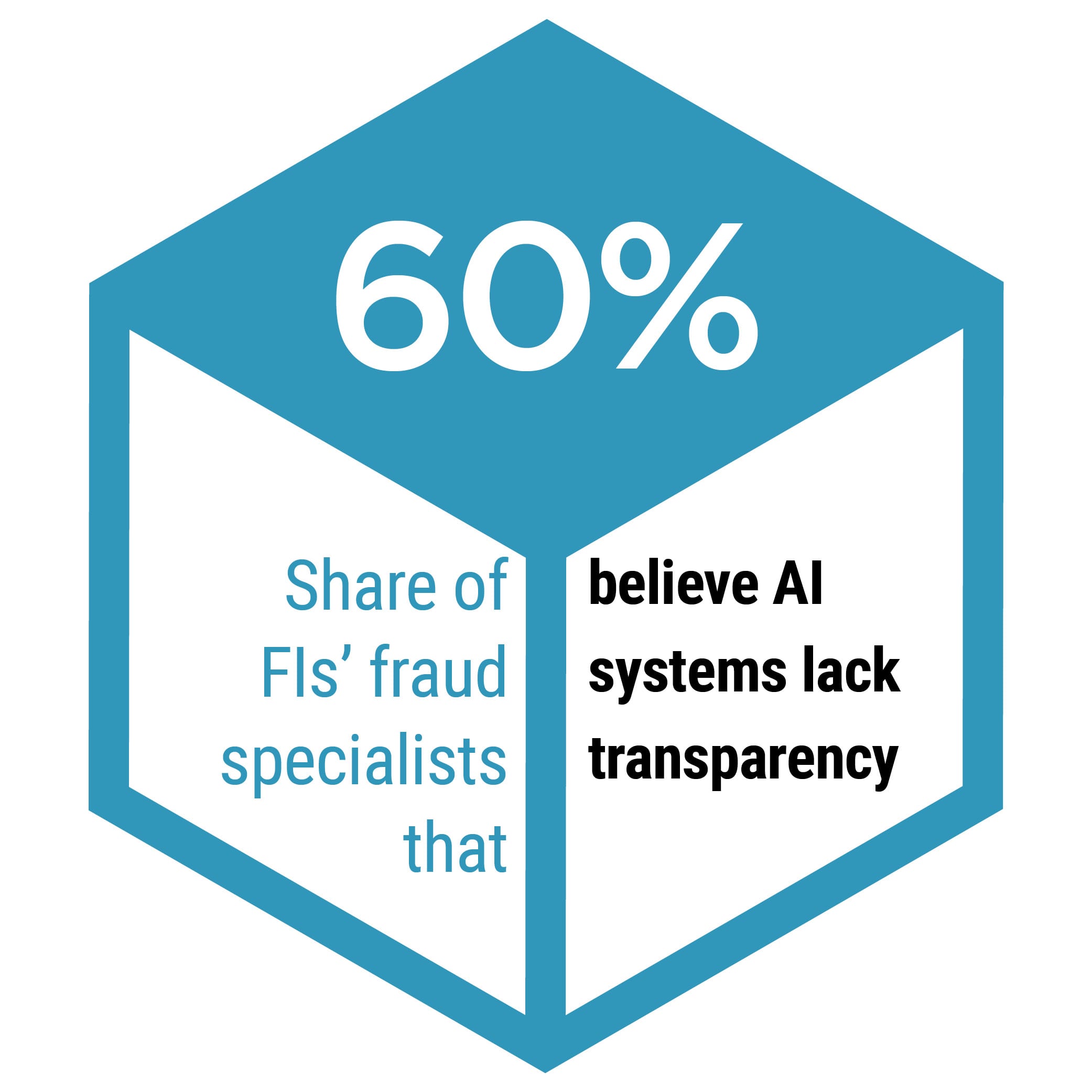

Another major barrier is the “black box” surrounding AI: Decision-makers do not always understand why AI systems make the decisions they do. In fact, 60 percent of bank fraud specialists don’t believe AI technology is transparent enough, and the same portion view it as complicated and time-consuming. This speaks not only to their misunderstanding of how AI systems make decisions, but to the fact that many may not fully understand how to use it.

Luckily for FIs and their fraud departments, education can help solve this problem — and the Playbook is just the beginning.

Key findings from the study include:

- 63.6 percent: share of FIs that believe AI is an effective tool for stopping fraud before it happens

- 80 percent: portion of AI-using fraud specialists that believe the technology could reduce payments fraud

- 63.9 percent: share of fraud specialists that believe smart agents could reduce payments fraud

To learn more about the promise of AI to modernize FIs’ anti-fraud efforts, download the report.

In the old days, forged checks were the biggest problems that bank fraud departments had to manage. Today, financial institutions (FIs) face a barrage of cyberattacks from hackers operating around the world, continuously shifting their tactics. It is no wonder that fraud prevention is one of the problem areas that FIs hope artificial intelligence (AI) can help resolve.

In the old days, forged checks were the biggest problems that bank fraud departments had to manage. Today, financial institutions (FIs) face a barrage of cyberattacks from hackers operating around the world, continuously shifting their tactics. It is no wonder that fraud prevention is one of the problem areas that FIs hope artificial intelligence (AI) can help resolve.