Consumers’ desire for banking convenience has spurred their interest in bundled banking services. In fact, many consumers are willing to leave banks that fail to offer bundled services, according to “Bundled Banking Products,” a PYMNTS and Amount collaboration based on a survey of 2,290 U.S. consumers.

Get the report: Bundled Banking Products

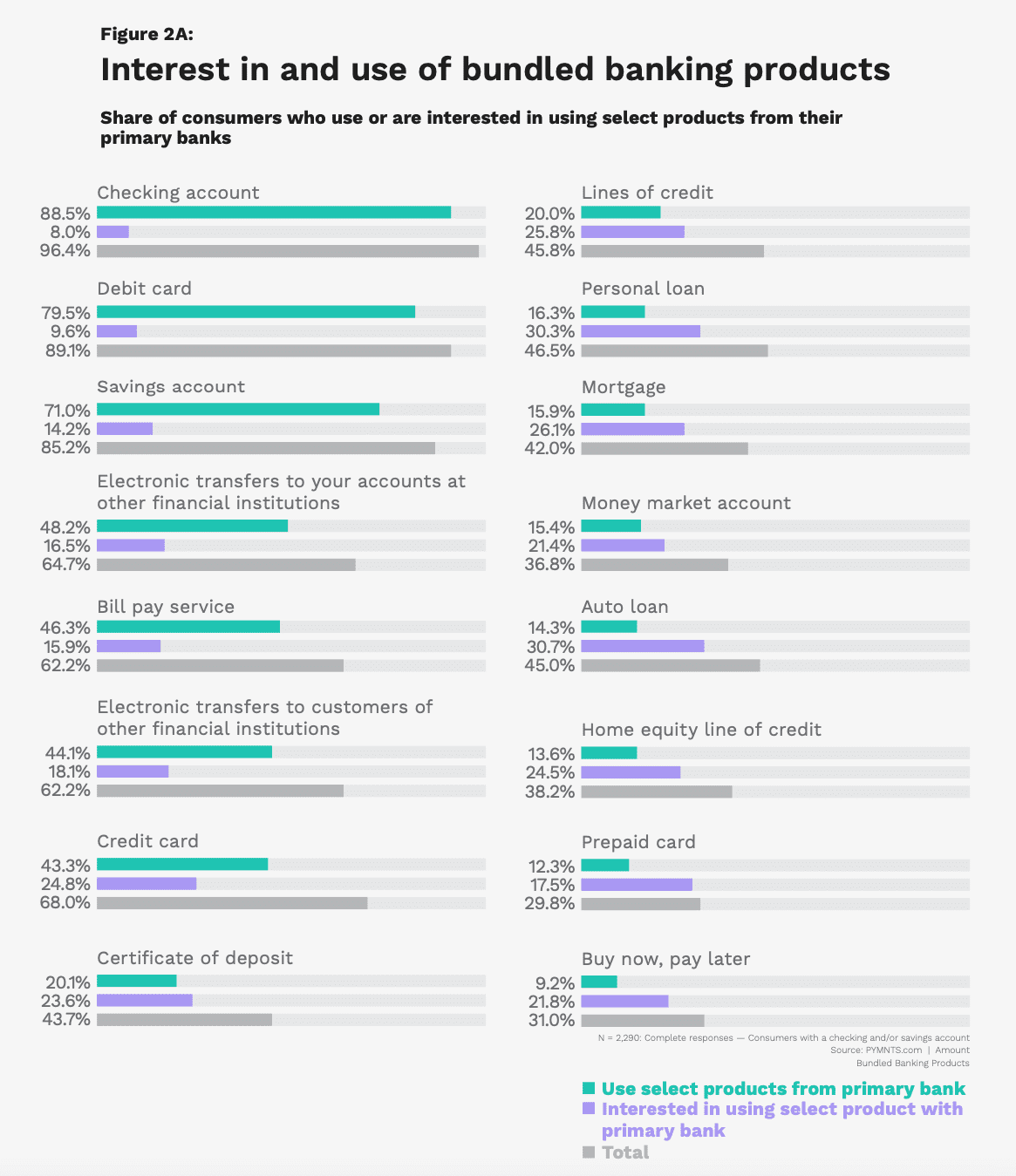

A bundled account is usually a single service offering from a bank that includes multiple offerings, such as a checking account, debit card and/or credit card.

Currently, consumers go to their primary banks for traditional banking products.

The top seven most common products that banking customers get from their primary financial institutions are a checking account, debit card, savings account, electronic transfers to their accounts at other financial institutions, bill pay service, electronic transfers to customers of other financial institutions and credit card.

While consumers use multiple products from their primary banks, nearly one in four use credit cards from a different issuing bank.

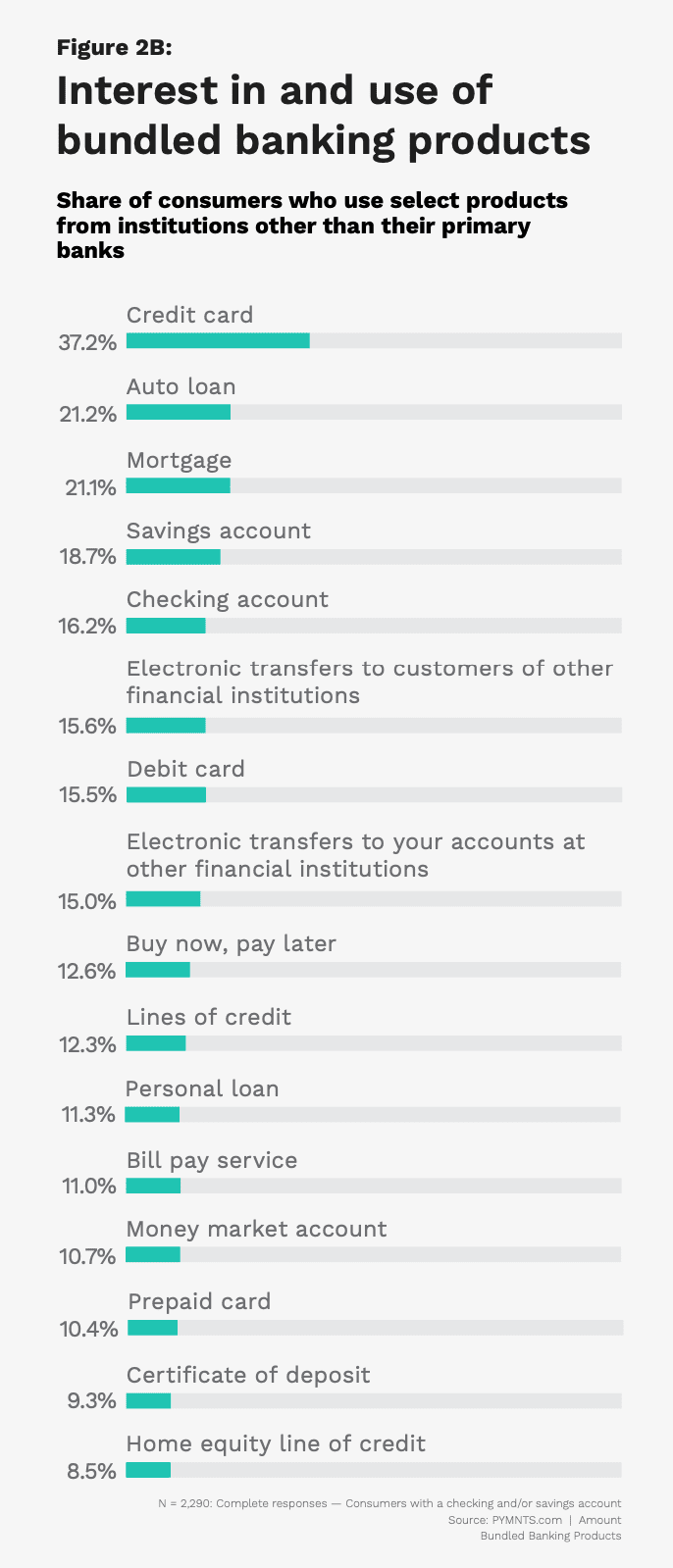

Together with credit cards, some of the most common products that banking customers get from financial institutions that are not their primary banks are auto loans and mortgages.

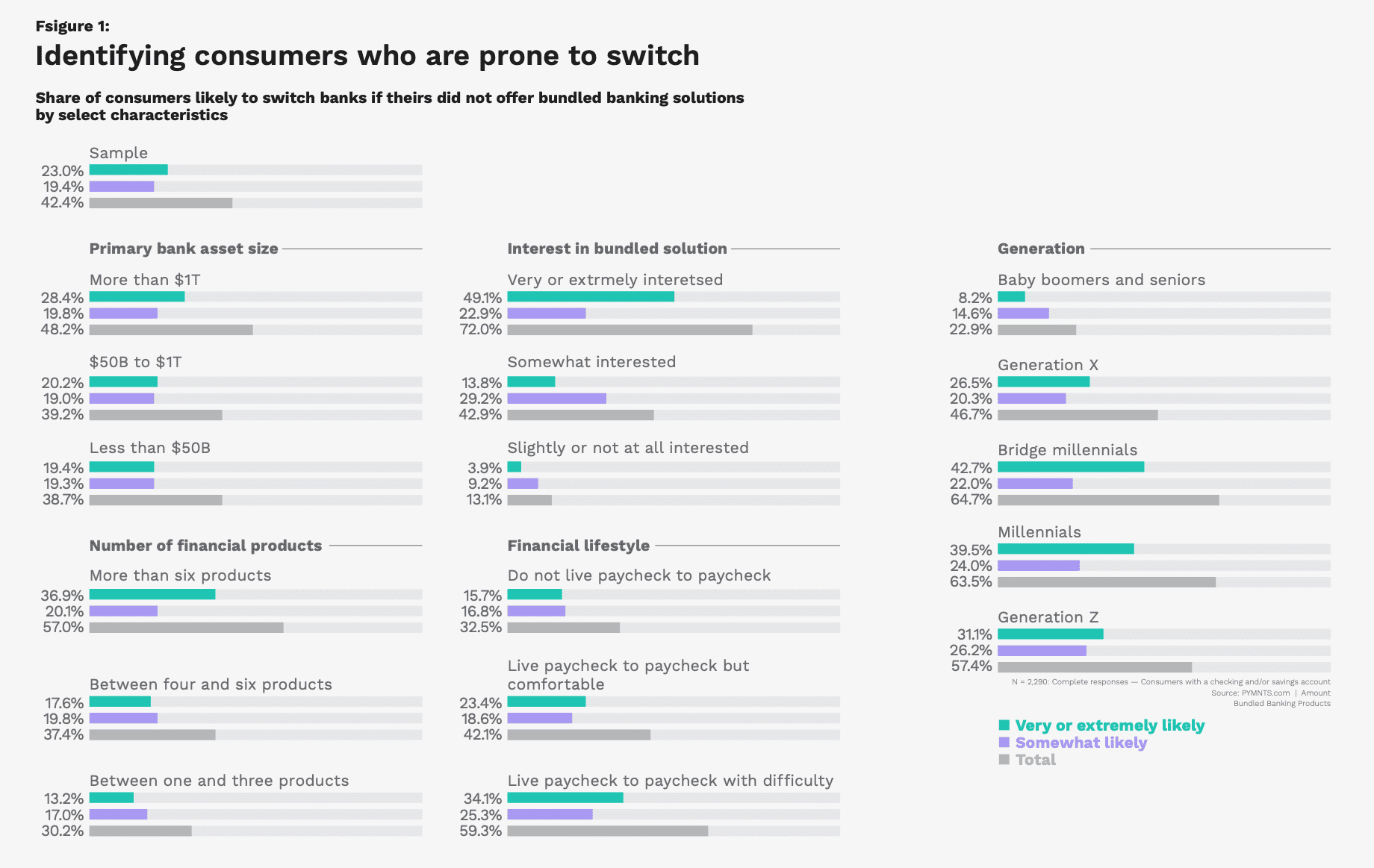

Wanting to enhance their convenience and have a range of payment options at their disposal, many consumers would consider going elsewhere to get bundled banking products.

In fact, 42% of consumers would be willing to switch financial institutions if their primary financial institution did not offer bundled banking products.

That share includes 23% of consumers who would be very or extremely likely to switch banks, and another 19% of consumers who would be somewhat likely to switch.

PYMNTS’ data clearly finds that consumers are prepared to seek out banks that provide innovative and flexible bundled offerings with convenient payment options and helpful recommendations.

The banks that openly provide these types of convenience may win consumers over for the long haul.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More