Europe sets the pace for fashion, finance … and fraud? As EMV gains traction in the States, the chip card revolution on the Continent has already largely been completed. And the bad guys are increasingly plying the fraudulent transaction game online. TSYS offers up a few data points you should know about Europe when it comes to payments fraud.

If a data breach is a sprint — where a fraudster grabs as much data as he or she can, as quickly as possible, in an effort to maximize ill-gotten gains — the fight against fraud is a marathon.

A marathon that never ends.

Fraud varies country to country, region to region. Just as payment methods are varied, so too are the ways that people pay, and whether, given a certain locale, they prefer paper (cash) over plastic (via mag stripe or chip card), or mobile over interactions with the cashier — these differences color fraud as well.

Europe may offer a tell on the fraud to come. As has been widely noted, the region has paved the way for the adoption of EMV, and its embrace by merchants in the EU, mandated though it has been, has steered hackers and criminals to online methods of siphoning funds from consumers and cheating companies. European countries led the adoption of EMV, with 86 percent of cards and 99 percent of transactions complying with EMV rules. By way of contrast, only 51 percent of cards in the United States are chip cards, and only 20 percent of transactions go by way of EMV mandates.

No mag strips, and so … when it comes to fraud, no swipe, no sweat?

No mag strips, and so … when it comes to fraud, no swipe, no sweat?

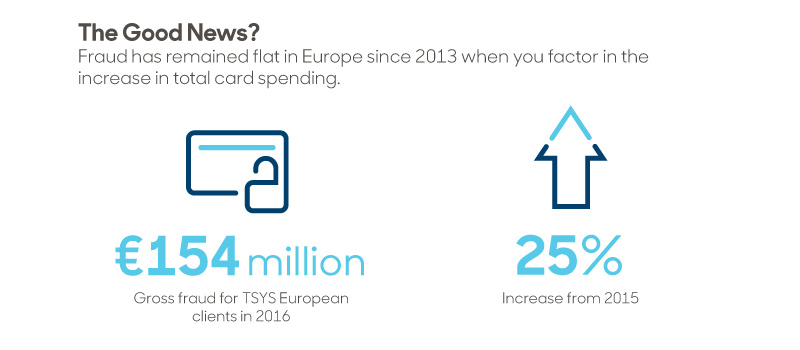

In a recent whitepaper by TSYS, research revealed some rather troubling news: Europe remains a leading indicator of the less-desired sort, a harbinger of fraud battles to come here in the United States. The data shows that overall, gross reported fraud was up to €154 million, up 25 percent from the year before. Of more than half a dozen types of fraud, ranging from stolen cards to counterfeiting, card-not-present (CNP) fraud remained the dominant conduit to fraud losses, at 80 percent of the tally.

And in looking across the pond at the EU, CNP fraud leads the way, with numbers stretching from a low of a “mere” 75 percent to a high of 82 percent, depending on the country, and the average stood at 79 percent.

And in looking across the pond at the EU, CNP fraud leads the way, with numbers stretching from a low of a “mere” 75 percent to a high of 82 percent, depending on the country, and the average stood at 79 percent.

Amid the things to note about fraud as it is done in European nations:

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More