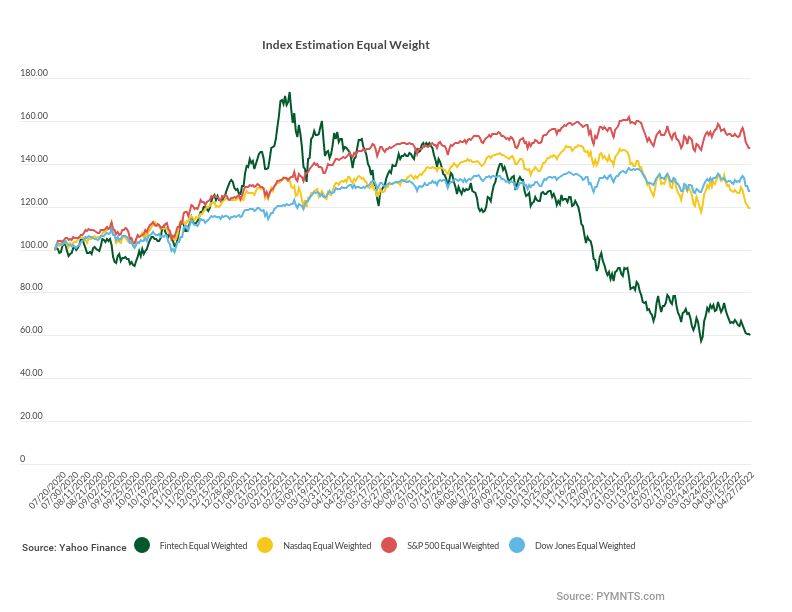

Down 7.5% for the week.

Ending April down 16.4%.

And for the year, the FinTech IPO Tracker has dropped 34.3%.

More of the same, in other words — and the future will no doubt be rocky.

Because: May is when we will see earnings reports, for many of these small digital upstarts (as measured in market cap). The fact that the names have continued to trade “down” in action ahead of earnings gives at least some indication of caution.

Signals and the read across from economic data and other companies within the financial services space are mixed. The payments networks such as Visa and Mastercard show that consumer spending has been resilient. So has the general number released with the latest GDP information — where GDP declined by 1.4% on an annualized basis. But with a bit more granular detail, consumer spending was up 70 basis points. The question becomes how long. That same government report shows that inflation is running ahead of disposable income, while savings dropped.

PYMNTS’ own data show that consumers are tightening the belts a bit, spending on essentials (but not much else).

Read more: Today in Data: Inflation Has Consumers Sticking to Essentials

None of this augurs particularly well for our FinTech names … because if and when consumers pull back, that pullback will hit transaction volumes, the urge to embrace new digital services and products, and by extension, hit the top lines for many of these newly-public FinTechs. The capital markets would, naturally, tighten as rates move higher, which hurts the ability to tap funding that helps offset cash flow burn as these ascent firms seek to (eventually) turn profits.

With all of these cautionary signs, it may be no surprise that only four names eked out positive gains on the week, and meager ones, too. The best performing name on the week was KE Holdings, up a bit more than 2.8%, followed by OneConnect, up 2.1%. And yet, both of those names are down a respective 33% and 43%, year to date, as of this writing.

Opendoor Technologies and Katapult were the two worst performing names in the group for the week, off a respective 17.5% and 15.8%. Opendoor, of course, has been subject to the vagaries of the housing market, where rising mortgage rates and home sales continue to push and pull against one another (and really, no one can tell how the residential real estate market will fare).

Separately, vis a vis lease-to-own (LTO) platform Katapult: In an interview with Karen Webster, Katapult CEO Orlando Zayas said there’s a growing mismatch between circumstances and financial capacity.

“Regardless of whether you want these items, you will absolutely, positively need them at that moment,” he told Webster, “which makes the situation for those who have trouble getting financing even harder.”

That opens the door for the lease to own opportunity, he said, especially in the paycheck-to-paycheck economy.

Read also: Lease-to-Own Plans a Boon to Merchants and a Lifeline to Strapped Consumers

And in other company specific news, Paysafe announced a new partnership with Exeter Finance LLC, an indirect auto finance company headquartered in Texas. Paysafe is expanding its presence in the payments space for U.S. auto finance by offering its Paysafecash online cash, or eCash, solution as a payment method for Exeter customers, per a news release.

In what might be a hint of just how firms may have to react to the fact that the hyper growth spurred by the pandemic might be in the rearview mirror (at least in beefing up operations), Robinhood has said it’s laying off 9% of its full-time employees to reduce duplicate roles and organizational complexity.

Read more: After Spurt of Pandemic-Driven Hiring, Robinhood Cuts 9% of Full-Time Staff

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More