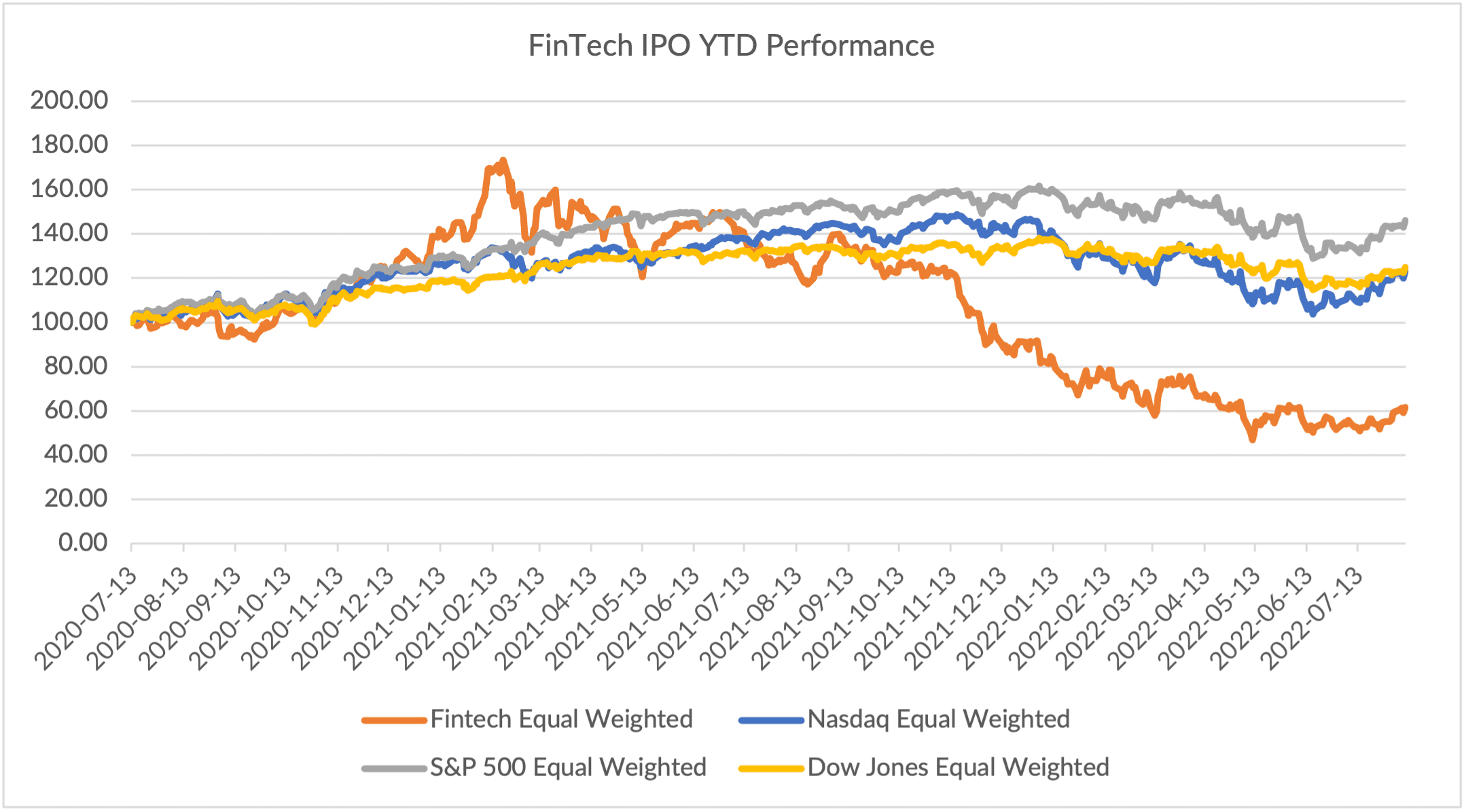

The FinTech IPO Tracker is up 16.9% for August — and we’re not even halfway through the month.

Earnings continued to drive stock performance, and in many cases the moves, up or down, were significant, often in the double-digit percentage point range.

Lemonade was up 29.5% on the week. The company said in its latest earnings release that in-force premiums stood at $458 million, up 54% year on year. Premiums per customer gained 18% in the same period, and the total customer count was up 31%, to 1.6 million. Lemonade said in its materials that 23% of the sales in the quarter came from cross-selling activity.

Lemonade was up 29.5% on the week. The company said in its latest earnings release that in-force premiums stood at $458 million, up 54% year on year. Premiums per customer gained 18% in the same period, and the total customer count was up 31%, to 1.6 million. Lemonade said in its materials that 23% of the sales in the quarter came from cross-selling activity.

With the closing of the Metromile (a pay per mile vehicle insurer) transaction, Lemonade said the deal “changes our product mix significantly. Renters now comprise about a third of our book, down from almost a half, while Car jumped from 1% to 20% overnight.” Car and home insurance will soon be bundled, the company said. Last week, Lemonade said it has divested Metromile’s Enterprise Business Solutions (EBS) to digital insurance platform EIS.

MoneyLion was up about 20% headed into, and just after its Thursday (Aug. 11) earnings report. The company said that customers were up 124% year over year to 4.9 million for the second quarter of 2022. In addition, products of 10.4 million was up 75% year-over-year for the second quarter of 2022. Total originations grew 85% year-over-year to $439 million for the second quarter of 2022.

Enfusion followed with a jump on its own results, where the shares were up 15.5% through the past week. Revenues grew to $36.5 million, according to the most recent release, up 38% year over year led by new client signings and growth from existing clients.

Some Decliners, Too

Not all names that reported earnings surged, however. Paymentus lost 38% on the heels of its results earlier this month, which showed that second-quarter transactions increased 39% year-over-year to 89.5 million. Revenue gained 28.3%. The company guided to slowing growth looking ahead, guiding revenue for the year to be up 25% to 27%.

Opportun was down 24.4%. The company said this week that its second quarter saw 103% year on year originations growth, with 63% year on year revenue growth. The company disclosed in its filings that it had more than 1.8 million members, a more than 300,000 increase since the start of the year. There is at least some nod to lowering originations due to credit tightening. The company also said it was increasing charge-off expectations. The filings note that the 30 day-plus delinquency rate was 4.3%, up from 2.5% last year. The annualized net charge off rate was 8.6% in the latest period, up from 6.4% a year ago.

And as reported in this space, Marqeta shares sank more than 20% Thursday, as growth is slowing, and the future is uncertain for Marqeta’s key FinTech customers, and specifically those customers’ card programs. Marqeta’s 53% TPV growth is a meaningful deceleration from 76% seen earlier in the year.

Chief Financial Officer Mike Milotich noted it is “prudent to be cautious about the next several months.”

FinTechs, he said, are being “less aggressive” about their expansion plans and investments. He stated that “many of the customers signed in the last 12-plus months, as well as crypto customers, will ramp their businesses more slowly than we expected a few months ago” which in turn means that these clients’ cards and other financial products offerings will be muted.

Within the TPV, growth accelerated in expense management and on-demand delivery, offset by tough year-over-year comparisons in financial services and BNPL segments.

Read also: Marqeta’s Results Point to Slowing Growth in FinTech Digital Card Issuance

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More