The banks have two targets in the digital wallet battle — one, Apple Pay, may be easier to “beat.”

PayPal may prove to be a tougher foe.

As noted here, America’s biggest banks are banding together to launch a digital wallet to take on Apple and PayPal.

The digital wallet is slated to debut in the second half of the year, and though some of the details have yet to be made public, we know at this point that the digital wallet will be linked to Visa and Mastercard’s debit and credit cards. The wallet will be managed by Early Warning Services and will not, according to reports, be tied to peer-to-peer (P2P) service Zelle.

Coming right out of the gate, the wallet will have the connections in place for significant scale: As many as 150 million debit and credit cards will be available inside those wallets. That scale will be formidable, leveraging payment methods (the cards) that have been entrenched for decades.

Digital Wallets’ Appeal

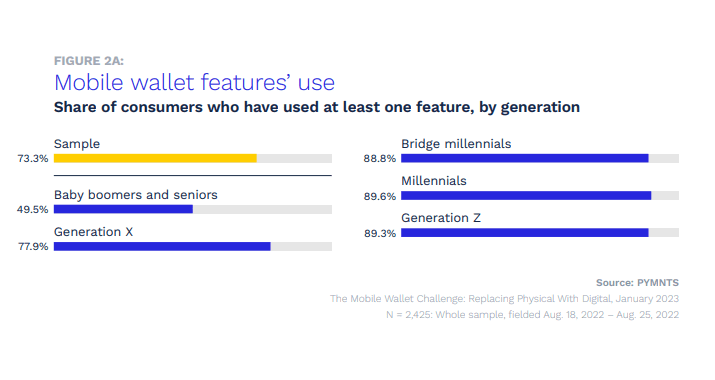

PYMNTS’ research in recent months has shown that the general appetite for digital wallets has been growing — and so, of course, the banks are bringing new efforts to bear in creating a new, digital conduit for payments, and in the process, chip away at Apple Pay and PayPal. But In “The Mobile Wallet Challenge: Replacing Physical with Digital,” the data shows a bit of bifurcation of the use cases. As seen in the chart below, roughly 74% of more than 2,000 consumers surveyed said they’d used a digital wallet for at least one feature. Drill down a bit, and younger cohorts — the Gen Z consumers and the millennials — have been more “exposed” to using the wallets.

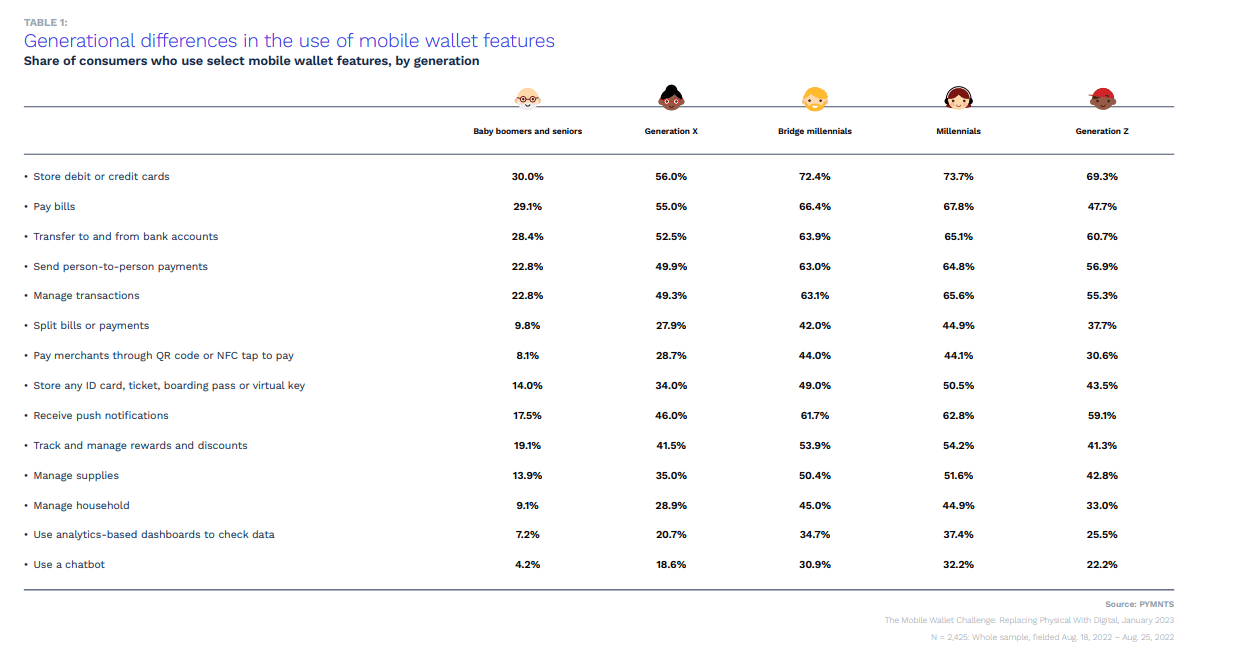

As for what they use the wallets for, there’s some indication that the banks will have some runway for growth here. Most users (excluding baby boomers) use digital wallets to store debit and credit cards, pay bills and transfer money to and from bank accounts. These are all core banking functions, we note, that would translate easily to using a bank-issued digital wallet.

Of course, the banks’ goal is to capture a share of transactions and payment methods used in those transactions. As to why Apple Pay might be the relatively easier target, at least at first and especially in in-store settings, we found late last year that Apple Pay, eight years after its debut, had captured only 2.4% of in-store transactions. More recent holiday season shopping data show that Apple Pay had been used in 12.7% of online transactions. That was far outpaced by the fact that credit and debit cards had been used in roughly half of the transactions online during holiday purchasing activity.

In the meantime, some indications are that Apple’s own card efforts, which “live” in the wallet, are facing headwinds. As reported last week, the Federal Reserve is investigating Goldman Sachs’ consumer credit division, which includes Apple Card, over consumer protection issues. Losses in that division have been mounting and Goldman has boosted its provisions for anticipated future losses, too.

Setting Sights on PayPal, Too

PayPal’s, arguably among the oldest digital wallets, showed in its most recent results that its total active accounts continues to grow, though it is slowing, where it had been in the double digits and now stands at 4%, per the latest quarter.

But that tally is 432 million, a strong showing and an entrenched, installed base. The number of payment transactions has been growing faster than accounts, at 15%, indicating repeat usage. Users, of course, have bank-issued cards in the digital wallet functionality offered by PayPal (the company’s eponymous Checkout function lets members bypass filling in details and pay with credit and debit cards). There may be some headwind in the banks gaining digital wallet share from PayPal, where those bank account/card details are already stored.

Much remains to be seen when the banks finally come to market with their digital wallets. But the banks have a natural onramp to linking those wallets to everything from lending to investments to insurance, forging a digital, connected ecosystem that extends beyond the debit card and the credit card.

The battle will be fully joined later in the year — some would argue a bit late — but better late than never.