“Don’t touch that!” No other parental admonition from our childhoods is as relevant to 21st-century payments as a universally-recognized “hands-off” warning. Only this time, it’s not about your brother’s hockey gear, your sister’s makeup or even Dad’s sacred toy railroad collection.

Now, it’s about ATMs, cash, POS keypads in stores — you name it. Just don’t touch it.

In the credit union (CU) sector, as in all other zones of the commercial map, touchless payments went from a novelty to something we can’t live without so rapidly that we had to measure it. PYMNTS’ March 2021 Credit Union Innovation Playbook, a PSCU collaboration, does exactly this, gauging CU member demand for new payments types with a “Look, mom! No hands” quality.

Surveying a census-balanced panel of over 4,800 U.S. consumers, the Playbook comes out swinging, noting that “48 percent of all CU members say their interest in touchless payments technologies has increased since the pandemic began,” and adding that “54 percent and 59 percent of millennial and Gen Z CU members, respectively, say they are more interested in using touchless payments for in-store purchases now than they were prior to March 2020.”

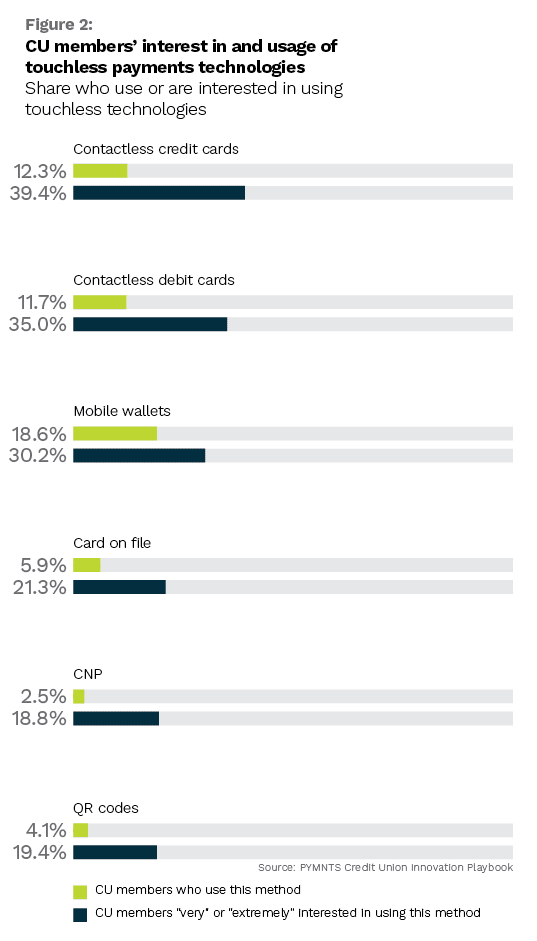

If only it were as easy as offering a one-and-done touchless product. Payments preference now calls the tune, and touchless is no exception. CU members, like other consumers, want choice, with the Playbook stating that “interest in contactless credit and debit cards is unmatched. Thirty-nine percent of all CU members are either ‘very’ or ‘extremely’ interested in using contactless credit cards,” while 35 percent said the same about contactless debit cards.

This makes contactless cards the first- and second-most in-demand touchless options among CU members. And it doesn’t end there, as the Credit Union Innovation Playbook proves.

The FinTechs Are Coming

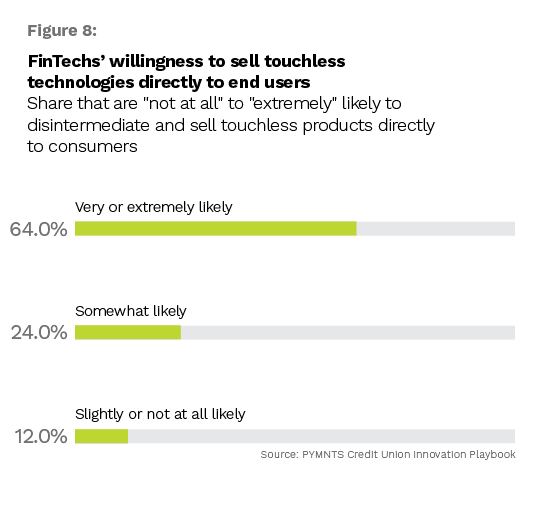

Of all the revealing findings in the March Credit Union Innovation Playbook, perhaps none is more salient — or alarming — than this: Two out of three FinTechs would bypass CUs and FIs to sell touchless payment options directly to consumers, given the chance. That’s worrisome.

“Credit unions could lose their members if they do not begin investing in touchless payment innovations. Our research shows that 15 percent of all credit union members would be ‘very’ or ‘extremely’ likely to leave their current CUs to bank with competitors if those competitors were able to offer them touchless payments options,” per the Playbook. “We also found that 21 percent of members would be ‘somewhat’ likely to switch FIs for touchless payments.”

It’s worth paying attention to this troubling trend for CUs. As the Playbook adds, “many FinTechs are innovating those touchless payments to steal CUs’ members away,” with researchers finding that 64 percent of FinTechs “say they would go around their partner CUs and banks if it meant selling directly to end users. CUs are thus in a race to roll out touchless payments innovations before their FinTech competitors beat them to the punch.”

While all is fair in love and war, many CUs are right to fear FinTechs simply because the CUs themselves are lagging on the touchless tech side — and members simply aren’t having it.

According to the Credit Union Innovation Playbook, “only 31 percent as many CU members use contactless credit cards as would like to use them, and only 33 percent as many CU members use contactless debit cards as would like to use them. A similar pattern can be found for mobile wallets, card-on-file options, CNP options and QR codes. There are far more CU members who would like to use each of these technologies than currently use them. Closing this gap through innovation will be critical to meeting credit union members’ payment needs going forward.”

Poaching Customers (Without Touching Anything)

Poaching Customers (Without Touching Anything)

Touchless payments are now a battleground, and the window is closing. CUs investing in alignment with their members’ payment preferences can ensure success in the fight.

“Fifteen percent of all CU members would be ‘very or ‘extremely’ likely to leave their CUs to bank with competitors if those competitors could offer touchless payment options, and 21 percent would be ‘somewhat’ likely to do the same,” per the new Playbook.

Putting an even sharper point on it, the Playbook notes, “The majority of FinTechs are interested in rolling out touchless payment innovations that could put them in direct competition with credit unions. Seventy-six percent of FinTechs are ‘very’ or ‘extremely’ interested in developing contactless credit cards, and 68 percent are just as interested in innovating contactless debit cards.” Also, 84 percent are interested in new mobile wallets, and 86 percent are interested in the possibilities for more QR code-enabled payments.

When it comes to FinTech poachers, don’t forget this important finding: “Bank and FinTech customers are far more willing than CU members to switch primary FIs for touchless payments options, as 24 percent are ‘very’ or ‘extremely’ likely to do so. Another 22 percent of bank and FinTech customers would be ‘somewhat’ likely to do the same.”

In other words, poaching customers works both ways, and CUs are getting wise to that fact.