Call it a Sophie’s Choice for the modern banking industry. Should banks and financial institutions (FIs) focus more on giving consumers the convenience and simplicity they expect — and even demand — or instead focus more on implementing stringent security measures, potentially at the expense of user experience?

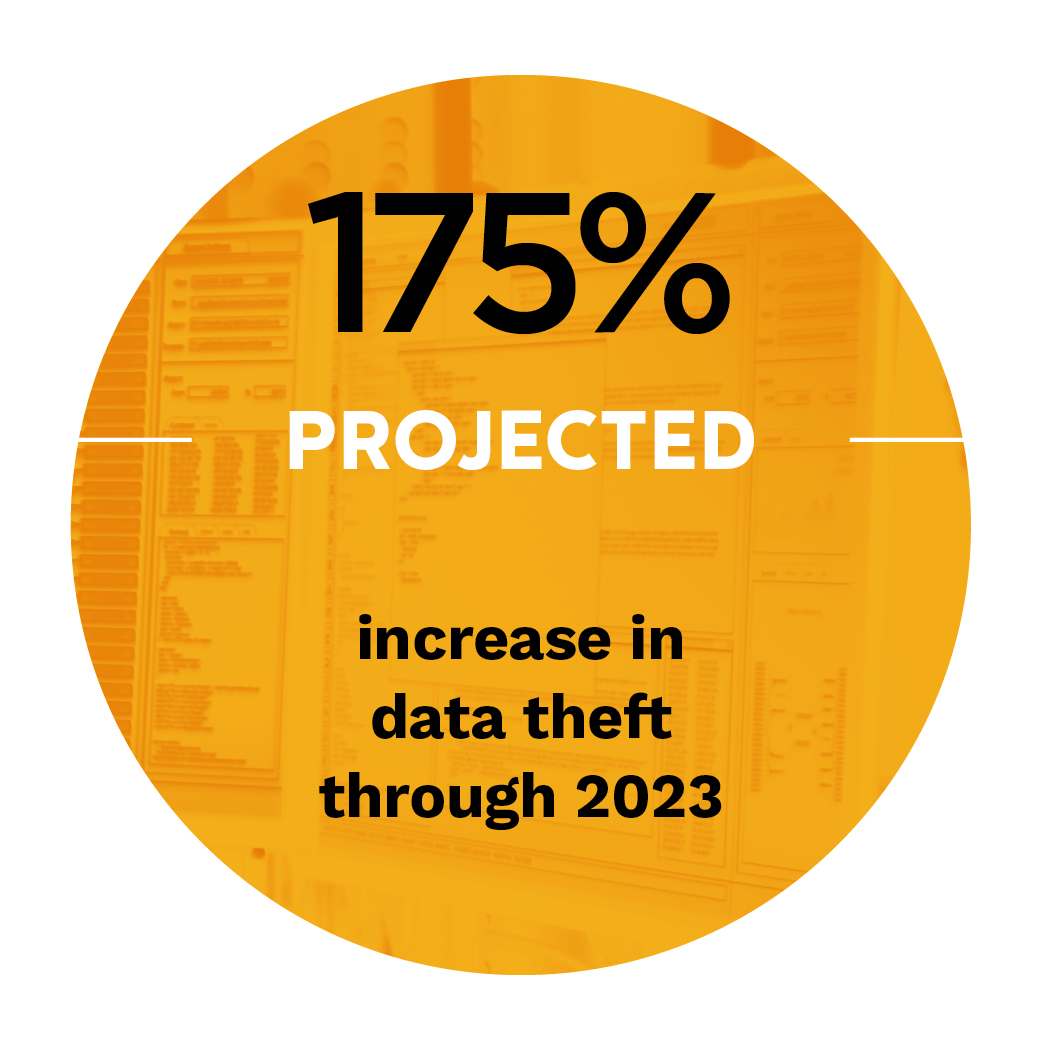

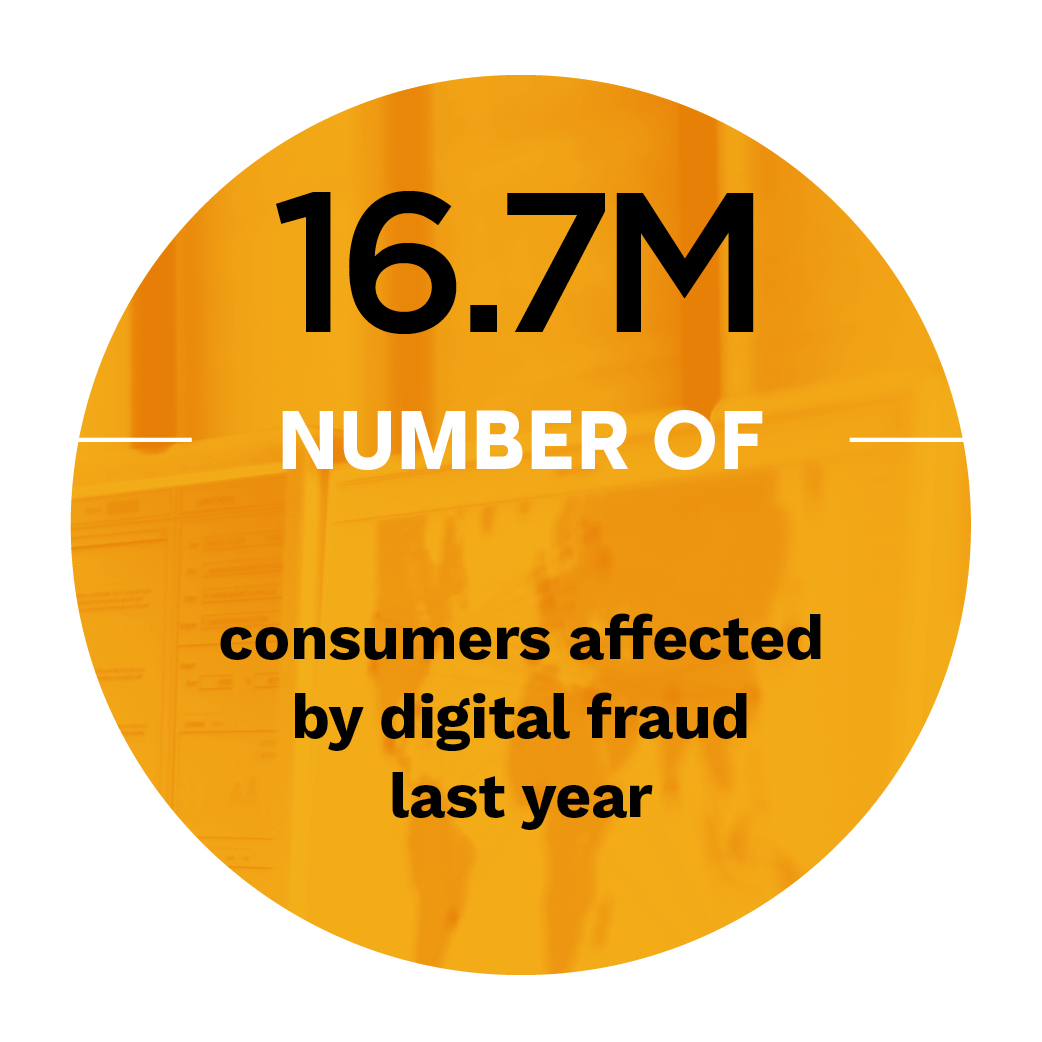

It’s a question that banks increasingly must work to answer in today’s day and age. Fraud is on the rise, as 17 million people in the U.S. alone were victims of cybercrime last year, an increase of 12 percent over the previous year.

In the inaugural issue of the Digital Fraud Tracker™, PYMNTS explores how online merchants and FIs are working to balance this need for security with consumer demand for convenience amidst rising fraud.

In the inaugural issue of the Digital Fraud Tracker™, PYMNTS explores how online merchants and FIs are working to balance this need for security with consumer demand for convenience amidst rising fraud.

Around The Digital Fraud World

Those hoping to stop the spread of digital fraud are turning to partnerships to match seamless user experience with top-notch fraud protection.

The World Economic Forum, for instance, has announced plans to pair with a half-dozen FI partners around the world to prevent cybercrime. The effort recently kicked off when the agency announced it would team up with Russia’s Sberbank to share information and technology going forward

The Israeli government is also turning to new partners in its fight against fraud. The country’s government recently announced it would invest 90 million shekels, or $25 million USD, in local cybersecurity providers to bolster its fraud prevention industry. The three-year program will enable companies working in high-risk research and development to receive up to 5 million shekels a year, and will also help fund pilot projects in Israel and abroad.

Meanwhile, Microsoft’s M12 venture fund also seems to have a new cybersecurity partner. The company recently contributed to a fundraising round for cybersecurity startup HYAS, which totaled more than $6.2 million in total investment. The company works to use consumer data to build security platforms that help discover and prevent cyberattacks. The company also seeks to track threats and discover the identities behind those responsible for them.

Meanwhile, Microsoft’s M12 venture fund also seems to have a new cybersecurity partner. The company recently contributed to a fundraising round for cybersecurity startup HYAS, which totaled more than $6.2 million in total investment. The company works to use consumer data to build security platforms that help discover and prevent cyberattacks. The company also seeks to track threats and discover the identities behind those responsible for them.

To read more on these stories and other from around the space, check out the Tracker’s News and Trends section.

Deep Dive: Fighting Fraud With AI And Machine Learning

Many of these players, along with others from around the space, are turning to artificial intelligence (AI), machine learning (ML) and algorithms to help them cut down on the number of successful cyberattacks that affect their business.

In the inaugural Digital Fraud Tracker, PYMNTS takes a deep dive into the world of cybercrime, exploring the latest attack methods employed by fraudsters, and the solutions security providers are using to stop them.

How Ally Balances Convenience And Risk

Giving consumers an experience that’s both enjoyable and secure takes more than artificial intelligence or machine learning.

Anand Talwar, deposits and consumer strategy executive for digital-only bank Ally, believes companies also need to invest in getting consumers on board with security standards. If not, they risk making themselves — and their customers — even more vulnerable to fraud.

Anand Talwar, deposits and consumer strategy executive for digital-only bank Ally, believes companies also need to invest in getting consumers on board with security standards. If not, they risk making themselves — and their customers — even more vulnerable to fraud.

In a recent interview with PYMNTS, Talwar discussed how the company works to provide both convenient experiences and stringent security to its customers, by giving them increased control over their security standards.

“The world moves really fast in this space,” he said. “We want to continue to evolve and make sure we’re moving to our goal of giving customers a convenient, frictionless experience while also making sure [they are] protected.”

To read the full story, download the inaugural Digital Fraud Tracker™.