Consumers have quickly shifted how they make routine purchases during the pandemic, with many moving online to buy their groceries or pay bills rather than shop in person. A recent PYMNTS study found that 79 percent of consumers intend to continue the digital shopping habits they picked up in the early months of the ongoing crisis, in fact. The continued migration to virtual channels and digital payment methods is just one of the significant ways consumers’ shopping and buying preferences are changing. The value consumers want out of their everyday payment experiences is evolving as well.

Consumers are seeking convenient payment solutions that offer tangible financial benefits while allowing them to complete their transactions speedily, and research shows that they are more than willing to switch financial institutions (FIs) when they find these features lacking. One recent study found that approximately one in five consumers have switched to new financial providers in the past year, 33 percent of whom did so to access better savings or improved rewards. Consumers prize these programs when making purchases, with another study finding that 67 percent of consumers decide where they will spend based at least in part on their ability to earn rewards in doing so.

Merchants should take note of consumers’ rising interest in rewards as well as the growing popularity of debit cards. The following Deep Dive takes a closer look at why debit rewards are reemerging as a draw for consumers, owing to continued economic anxiety and to the emerging role of payments via connected devices such as digital wallets. It also points out how merchants can reap key benefits from participating in these programs as they aim to capture and retain customer loyalty.

The Debit Rewards Renaissance

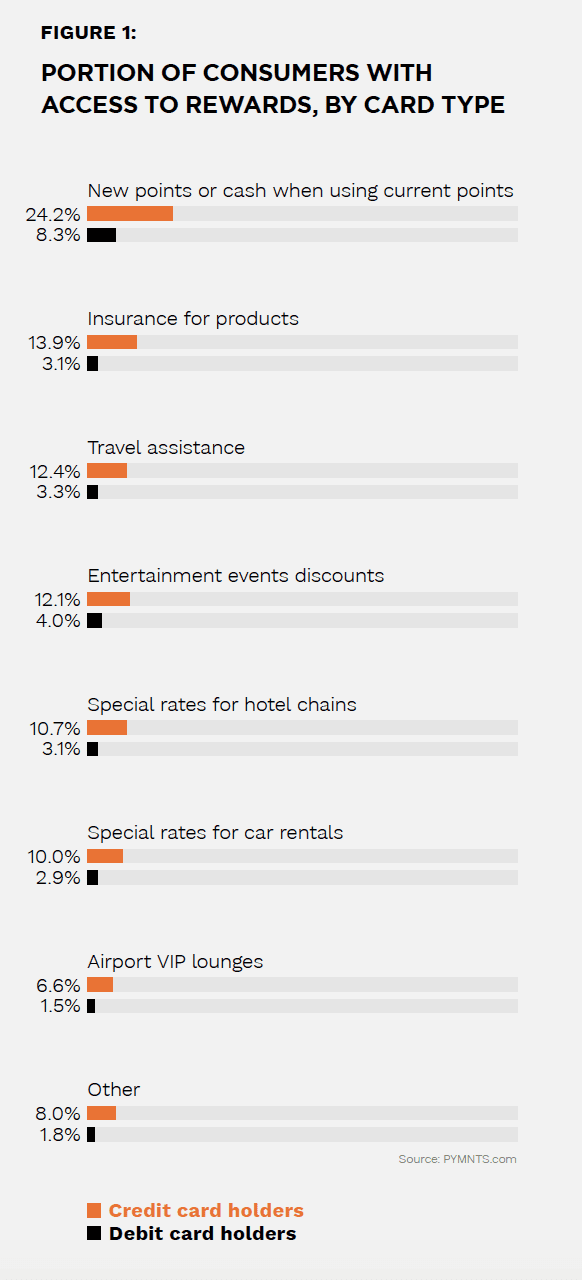

Some merchants may be unfamiliar with debit rewards and their potential financial benefits because these types of offerings have become relatively scarce at U.S. banks since the 2008 recession and the passage of the Durbin Amendment. The 2010 amendment capped interchange fees for debit cards, a move that dampened banks’ debit revenue and caused them to reduce or remove the customer benefits or rewards programs they offered prior to its passing. Recent PYMNTS research found that access to debit rewards is much rarer for consumers than credit benefits — only a little over 8 percent of debit card holders can gain points or cash back when making purchases, compared to the 24 percent of credit card holders who said the same.

Recent developments have led to a resurgence in consumer interest in programs that can provide them with cash back or other benefits as many shoppers begin to eye rewards features as tools for managing their finances. Twenty-nine percent of credit card holders surveyed in one study said they view their rewards balances as a way to extend their budgets. This has not gone unnoticed by the financial industry: While legacy FIs have taken a step back from debit rewards for a decade, FinTechs and challenger banks have recently moved to take advantage of this gap in the financial market. Digital-only players Current, N26 and Upgrade launched or expanded debit-linked rewards programs in recent months as more consumers migrated to debit for a higher portion of their banking and shopping. These programs are all aimed at different demographics, targeting both higher- and lower-income as well as multiple age brackets, indicating their universal appeal.

It is important for retailers to note consumers’ growing scrutiny of rewards benefits as they shift from credit to debit for more of their spending. Research suggests that the increases in both online shopping and the use of contactless payment methods are driving this shift, with more shoppers tapping digital retailers in areas where debit already dominates, such as groceries. Tying rewards to the growing preference for debit presents a compelling opportunity for merchants to gain consumers’ loyalty — making participation in debit rewards programs a much more attractive prospect.

Debit Rewards And The Next-Gen Payment World

The draw of debit rewards programs could also be compounded for merchants as more consumers begin to use mobile or digital wallets to make payments more frequently. Digital wallets are becoming a more popular way to pay for eCommerce as well as in-store purchases, with recent PYMNTS data finding that 42 percent of bridge millennials — those between 33 and 43 years old — use these tools to pay online. Consumers are also indicating a desire for rewards linked to such payment solutions. One recent study found that 60 percent of consumers would be more willing to use peer-to-peer (P2P) mobile app Venmo as a payment method if it offered rewards, for example.

Merchants must keep a careful watch on how rewards could impact consumers’ use of debit-connected P2P or contactless payment apps. Debit rewards could be a key strategy for retailers looking to compete as the future of payments becomes more digital and personalized.