Why Restaurants Should Be Worried

The true measure of innovation is when no one has come up with anything better a couple of centuries later.

Nearly 300 years ago, an entrepreneur in Paris introduced the world to an innovation in dining that has remained the backbone of the restaurant industry ever since.

The concept, by today’s standards, seems so simple: Give consumers a choice of what to eat, choice of what time to eat it and a private place to sit in a dining establishment outside of their own home.

The innovation itself seems simple – in part because it is so familiar: a reservation system, a menu and a dining room format with separate tables for parties to sit together, but apart from others who are dining at the same time.

According to Yale historian Paul Freedman, Delmonico’s in New York was the first establishment to offer that innovative experience to Americans in the 1830s. He devoted a full chapter to it in his book, Ten Restaurants That Changed America, (Liveright, 2016) – a highly recommended read on the impact of restaurants on food culture and vice versa.

Over the next couple of centuries, there have been many variations on that basic theme.

Food options on menus now reflect the broad and changing tastes of consumers.

Tens of thousands of restaurants now include everything from the fancy to the fast casual to the coffee shops and cafes that offer a more “grab-and-go” experience.

Search engines help consumers discover new places to eat, software platforms eliminate the friction from making reservations at desired times.

Mobile devices make those options more accessible, and the opportunities to dine out more spontaneous. Buy buttons and credentials on file expand restaurant sales channels.

New business models and new tech drive standardization, consistency and scale for restaurant operators.

But the basic concept – giving the consumer the ability to choose food from a menu at a place of their preference at a time that’s most convenient for them remains the fundamental innovation behind the restaurant experience.

It’s also the source of its biggest disruption today and in the decade to come.

Back to the Future

Eating meals outside of the home wasn’t always a thing.

At the turn of the 20th century, about 60 or so years after the restaurant concept was introduced in the U.S., eating at a restaurant was still very much a novelty. At that time, dinner was almost always eaten at home – or at someone else’s home.

For the well-heeled, dinner was a ritual in which a couple of hours were spent sitting at a dining table with courses served by waitstaff. For the working class, dinner was much less a ritual and much more an act of sustenance. In the early to late 1800s, most meals outside of the home were eaten by tradesmen sitting at communal tables at inns and taverns, eating whatever the proprietor felt like cooking that day. Eating at fancy restaurants like Delmonico’s was a rarity.

Restaurants became more popular as the economy revved into high gear and the nature of work shifted from farming to manufacturing. It was no longer practical or convenient for workers to go home to eat lunch, and restaurants emerged to fill that void. They also became places where men – along with their wives and families – gathered for a night on the town.

Americans’ love affair with cars and driving in the 50s and 60s gave birth to fast casual establishments and, of course, the massive QSR economy that now accounts for 52 percent of all restaurant orders.

Still, having a meal at a restaurant wasn’t done all that often.

Most women didn’t work outside of the home and prepared the meals eaten by the family. Growing up, I don’t really remember going “out to eat” with my family aside from very special occasions, and the occasional Sunday drive “in the country.” The occasional trip to McDonald’s or Burger King was a really big deal for my brother and me, much to the disappointment of my mom, who took great pride in her home-cooked meals.

Times have obviously changed.

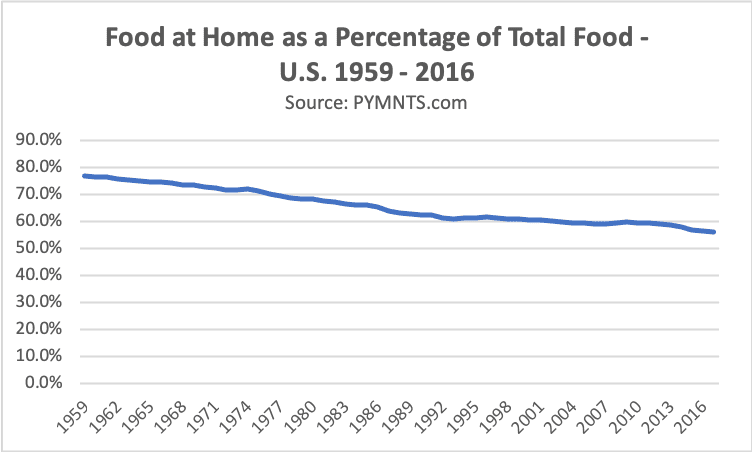

Over the last several decades, the composition of the workforce and demands on the family unit have shifted rather dramatically, and the restaurant industry has flexed to accommodate those changing times. Consumer spend has shifted, too, but more slowly. It wouldn’t be until 2002 – 162 or so years after the first true restaurant opened in the U.S. – before consumers gravitated to options outside of their own kitchens to make and eat their food and food dollars spent at grocery stores would dip below 60 percent.

For the restaurant industry, that’s the “glass half-full” part of the story.

When the Home Becomes the Restaurant

Today, 56 percent of U.S. consumer food spend remains grocery store-based. But there’s an important catch to the 44 percent of spend allocated to eating outside the home. Since restaurant meals are more expensive than eating at home (not counting the time to make them), the spend doesn’t mean that 44 percent of meals are eaten at restaurants. It just means that eating out costs more than eating in.

In fact, according to restaurant analyst NPD, more than 80 percent of dinners in the U.S. are eaten at home, up from 75 percent a decade ago. In 2018, they report that totaled 100 billion dinners – up, they say, from 75 percent a decade ago. Visits to restaurants dropped to a 28-year low in 2018.

Millennials are part of that story.

A decade ago, millennials ate outside the home 257 times a year; in 2018, that number dipped to 241 times a year.

Millennials, though, aren’t the entire story. Consumers, overall, have stopped frequenting restaurants at the pace they once did. In 2000, according to NPD, consumers ate outside the home 216 times a year; in 2018, that number declined 15 percent to 185 times a year.

There’s a catch here, too.

Just because more people are eating at home doesn’t mean more people are cooking at home.

Of the 100 billion dinners who ate at home in 2018, only 37 percent of those meals were made from scratch.

That means more competition among the growing list of players vying for the 63 percent of spend on food that is eaten at home, but purchased somewhere else.

Maybe that’s directly from a restaurant’s app or via a telephone order. But increasingly, that’s the grocery store’s prepared foods section, or a delivery aggregator like Uber Eats or Grubhub.

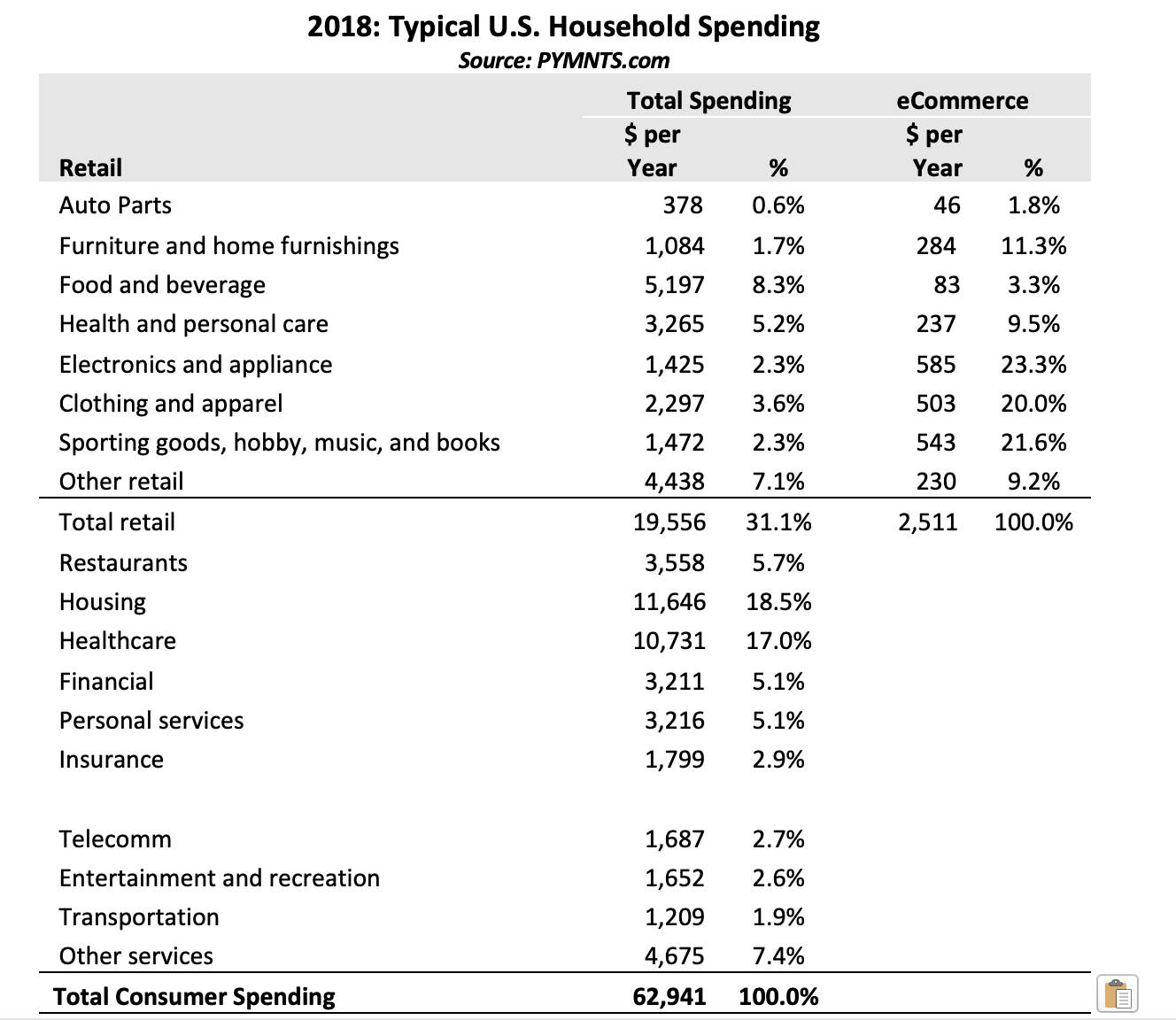

To put that in dollars and sense, that also means restaurant stakeholders are now competing not for the $3,558 that consumers spent last year on food eaten at restaurants, but for the $8,755 that the typical American consumer spends on food over the course of the year.

That could very well be the “glass half-empty” side of the restaurant story.

Consumers Are Redefining Fast Food

The innovations that gave birth to the restaurant industry – a reservation, a menu with options and a private table at which to eat food – are the very same tools that innovators are using 300 years later to reinvent the experience.

But now, instead of using those tools to drive more spend to restaurant operators, they’re using them to recreate the restaurant experience inside the consumer’s own home.

The friction for which each of these matchmakers is solving is well-known and well-defined: a time-starved consumer with little time to prep and cook a meal from scratch — or to sit and wait for food to be served at a restaurant.

These time-starved consumers are allocating less of their day to eating.

Long gone are the days of the two-hour dinner – perhaps even the half-hour dinner.

A study of consumers over two periods (2006 through 2008 and 2014 through 2016) reports that consumers now spend 5 percent less time eating over the course of a day. In 2016, that was roughly 64 minutes a day to eat all three meals. The study also found that nearly 17 minutes each day is spent eating while doing other things – working, helping kids with homework, talking on the phone, watching TV.

Three years later, who knows how much further it might have dropped.

Takeout, delivery, grab-and-go to heat up and eat later are now at the top of the consumer’s menu when it comes to getting a meal to eat at home.

Today, we have a ringside seat as a whole new crop of innovators use their scale to compete for the biggest consumer expenditure, outside of healthcare and housing, and force restaurants to change how they view their market and compete to stay relevant.

These innovators are taking a page out of the classic matchmaker’s playbook and introducing perhaps the first real innovation to hit the consumer-facing part of the restaurant experience in the last 300 years: logistics that power delivery at scale.

The Battle for the Food Dollar

Grocery stores, which already capture a big chunk of the consumer’s food dollars, see the opportunity to cash in even more. They’re stepping up by expanding their selection and quality of prepared foods, including from restaurant brands, and creating “grocerants” where for people can eat what they buy in the store. Investments in logistics have ramped up both curbside pickup and delivery orders that are increasingly being placed by commuters driving home from work.

Some grocery stores themselves have decided to become matchmakers by bringing restaurant brands — which might otherwise compete for their food spend outside of the store — inside their own four walls.

ShopRite grocery stores in Philly recently did a deal with Saladworks, a fast casual salad chain, to bring its restaurant experience inside of their stores; after a successful pilot, there are now plans for the eatery to expand into more supermarket locations.

Then, of course, there are the aggregators that give consumers the mashup of convenience and restaurant-quality food, serving as a one-stop ordering and delivery platform for the restaurant brands they know and love.

Over the last several years, these aggregators have built a critical mass of consumers — and secured their loyalty — by assembling a critical mass of restaurant brands ready to fulfill their orders. Restaurants sign on because they see it as a way to get orders, even though they run the risk of losing consumer loyalty to their brand and perhaps even the consumer herself as aggregators inevitably pivot their platforms — and their platform economics — to create their own branded food experiences.

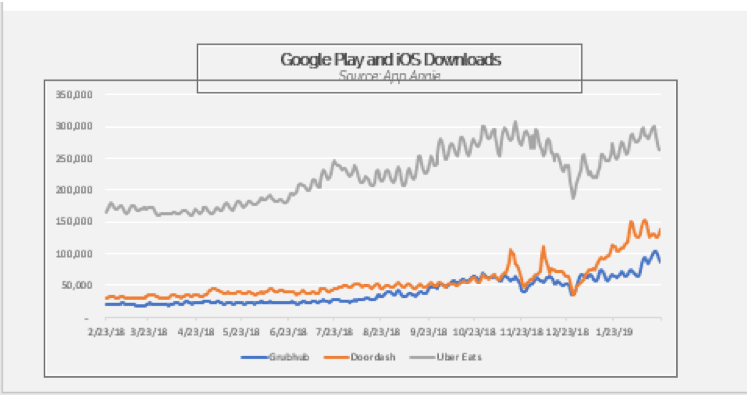

Although Grubhub tends to get the lion’s share of the headlines in that regard, the numbers tell a different story: Uber Eats appears to be the 800-pound gorilla in the space.

Not only do their mobile app downloads and usage dwarf that of Grubhub, UberEats leverages the platform adjacencies of Uber’s massive driver network to nail logistics and economics of delivery, now to more than 100,000 U.S. cities.

Not only do their mobile app downloads and usage dwarf that of Grubhub, UberEats leverages the platform adjacencies of Uber’s massive driver network to nail logistics and economics of delivery, now to more than 100,000 U.S. cities.

Uber Eats is also using its data on consumer food preferences to persuade restaurants on its platform to create digital-only “pop ups” inside of those establishments with limited, cheaper menu options and a stand-alone brand.

Restaurants say they like the idea because the marginal costs of serving those consumers can add incremental profits to the mix. Consumers say they like the idea because the quality is good but cheaper to buy.

Uber Eats really likes the idea because they are, in essence, setting up test kitchens inside existing restaurants that can, in theory, be used to bolster their own restaurant platforms with a built-in customer base at some point down the road.

And they are doing it, not by leveraging their expertise in operating restaurants, but their expertise in logistics wrapped around giving consumers a choice of what to eat and when and where to eat it.

Then there’s the two other 800 pound gorillas in the space — Amazon and Google — whose restaurant glass-half-full or glass-half-empty story remains to be told.

Amazon takes logistics and ups the ante further with voice via Alexa and payments via Amazon Pay, all inside of an expanding and expansive ecosystem of food ordering and delivery options, physical grocery and convenience stores and 100 million Prime Members who buy regularly from them.

Google has voice too, but also an important asset called search in a retail sector where search still matters and could be used to create a competitive advantage to help restaurant establishments reclaim control over their brand and the consumer’s loyalty to it.

Collaboration with platforms that can marry search with logistics to connect consumers directly with a restaurant could turn them into an intermediary that helps restaurants hold their own in a world in which competition for the consumer’s attention and food dollar will only intensify.

The Matchmaker Is In The Consumer’s Control.

According to a study of consumers done earlier this year, consumers just want what they have always wanted from a restaurant – good food, delivered when they want to eat it, where they want to eat it. It’s the same three things that a menu, a reservation and a dining establishment called Delmonico’s innovated and delivered more than 300 years ago in Paris and 200 years ago in the U.S.

Meanwhile, innovators, the matchmakers building their digital platforms, are blurring the bright lines that once divided how consumers thought about and purchased food at and away from home — now it’s all just food.

Just as they have done with retail. Soon the lines between food eaten in or out will seem as arbitrary as those between buying online or in the store.

But that’s what matchmakers do – step in to solve big problems for key stakeholders using a variety of platform design and pricing principles to create critical mass and drive profits.

Successful matchmakers do that at scale.

Really successful matchmakers leverage their platform assets into adjacent businesses and recast the dynamics of the sector.

What we’re seeing now is some of the most disruptive innovation in dining since the very first restaurant opened. The key problem for the consumer stakeholder is time. The platform asset matchmakers bring is logistics — restaurants have already done a great job of delivering choice through the design of menu options that cater to the diverse tastes of the consumer. Their value to the consumer is to shorten the distance between a hungry, time-starved consumer and food at a table of their choosing – which is now increasingly their home.

What we are starting to see is how some of those matchmakers and those dynamics are changing and who’s driving that shift.

It’s not just restaurants that will feel the impact. Almost everything about how people eat in or outside the home will change.

It’s why food is such a bellwether for how the rest of retail may evolve. And why for whom the glass is half-empty or half-full remains to be seen.