According to a PYMNTS Intelligence report, “BNPL and Embedded Finance Reshaping Consumers’ Credit Choices,” these options are reshaping how consumers manage everyday expenses and larger purchases, as more than half of consumers now use credit to buy groceries.

The Rise of New Credit Products

Consumers have a wider range of credit products at their disposal, thanks to the rise of embedded finance, which makes personal loans more accessible, and the popularity of BNPL. These newer credit offerings are impacting consumer spending patterns, especially in essential categories like groceries and dining out. For example, 52% of consumers reported using credit to buy groceries in the past 90 days, highlighting how credit products have moved beyond just large purchases to cover daily needs.

Different credit products appeal to consumers for various reasons. Credit card users often prioritize rewards, with 35% citing rewards as their main motivator for using credit cards for essential purchases. In contrast, BNPL users tend to choose this option for its familiarity, with 41% of BNPL users selecting it for essential expenses because they are comfortable with the product. Personal loan users, especially for necessities, place more emphasis on trust, with nearly a third saying they use personal loans because they trust the provider.

Essentials and Beyond

Consumers are turning to credit for not just discretionary spending, but essential purchases as well. The use of credit to purchase groceries, dining out, and clothing has become commonplace, with 40% of consumers using credit to pay for food from restaurants and 36% using it for clothing. These everyday expenses are often paid for through credit cards due to the convenience and rewards they offer, with 46% of credit card users citing convenience as a key reason for their choice.

While credit cards dominate for essentials, personal loans and BNPL are more likely to be used for larger or less frequent purchases. Notably, 16% of consumers used credit for household furnishings, while 15% used it for electronics and appliances. The adoption of credit across a range of purchases shows how essential financial flexibility has become in modern consumer habits.

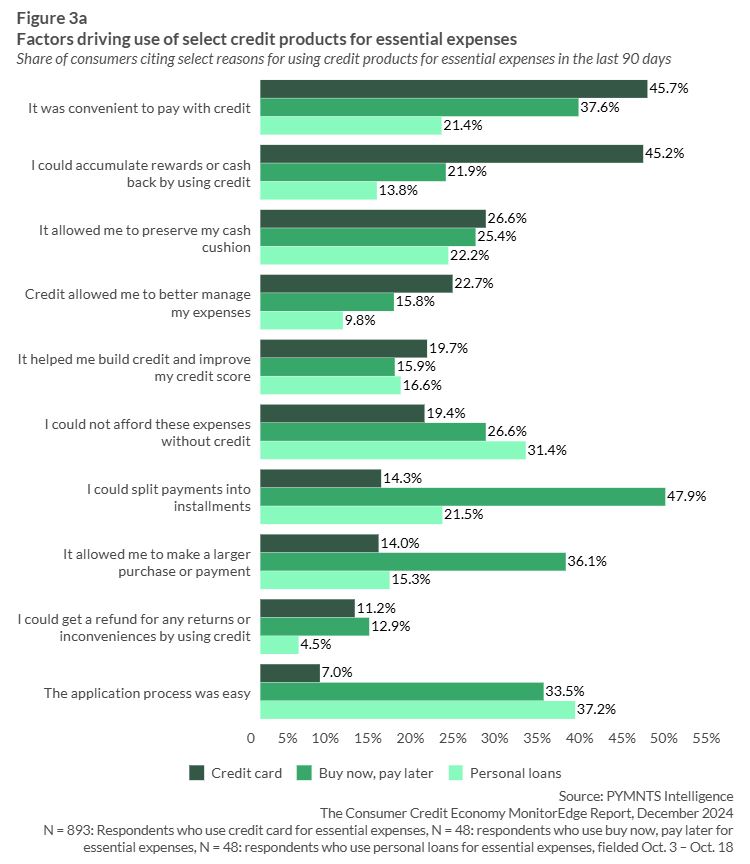

Motivation Behind Credit Usage

The reasons behind choosing a particular credit product vary depending on the nature of the purchase. For essentials, 46% of credit card users say convenience is a major factor, while 45% highlight the ability to earn rewards or cash back. Personal loan users often rely on loans for necessities they cannot afford otherwise, with nearly one-third of respondents citing financial need as the primary motivator.

BNPL users are more likely than other credit users to leverage this option for larger purchases. Consider 36% of BNPL users for essentials reported using it to make higher-value payments, showing that BNPL can spread out costs without impacting cash flow. This trend holds for nonessential purchases as well, with BNPL helping consumers preserve their cash cushion while making larger buys.