In the post, Julie Margetta Morgan, the CFPB’s associate director of research, monitoring and regulations, reminds readers that the top 10 credit card companies alone manage 83% of outstanding credit card debt and that many of the biggest card issuers offer cards that come with the worst terms, the highest interest rates and the steepest late fees.

“By comparison,” she wrote, “smaller credit card companies tended to offer far better deals on interest rates: across all credit tiers, small companies offered rates between eight and 10 percentage points lower than larger companies.”

Although she urges U.S. consumers to at least consider looking into cards issued by “small banks and credit unions,” there are even more types of alternate cards to consider, and PYMNTS Intelligence data indicates that co-branded cards and store cards could also be a possible alternative for consumers.

PYMNTS Intelligence’s recently released “The Role of Strategic Partnerships in Consumer Credit Cards,” a collaboration with Elan, offers an in-depth analysis of both co-branded and store cards — and why consumers gravitate to them.

The differences between co-branded cards and their in-store counterparts are significant. Co-branded credit cards generally feature a company’s logo and brand name alongside that of a card network. In most cases, they function like general-use credit cards and can be used anywhere on the compatible card network, even for purchases unrelated to the brand stamped on the front of the card. Store cards, on the other hand, feature the merchant’s branding exclusively and can only be used with that merchant.

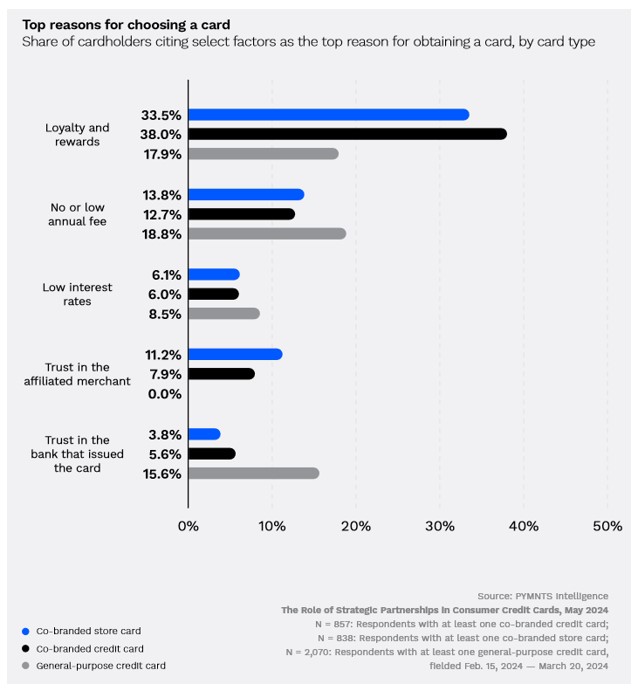

Regardless of the type of card in question, the report — which is based on surveys with more than 3,000 U.S. consumers — found that three main factors drive a consumer’s decision to use a card: loyalty and rewards programs, cost considerations and trust — although those factors weigh differently depending on the consumer and card type.

For those using co-branded cards, loyalty and reward benefits top the list. Thirty-eight percent of respondents with a co-branded credit card and 34% with a store card cite reward programs as their main motivation for obtaining the card. Conversely, just 18% of general-purpose credit card holders prioritize loyalty and rewards.

Cost considerations, meanwhile, play a smaller role for co-branded card holders than they do for general-purpose card users. Just 19% of consumers with co-branded credit cards and 20% of those with store cards say either low annual fees or low interest rates are a top reason for choosing the card; 27% who hold general-purpose cards said the same.

Trust comes third across the board, with between 14% and 16% of those who have co-branded or store cards citing either trust in the affiliated merchant or the issuing bank as their top reason. Notably, trust in the brand displayed on the front of the card tends to matter more than trust in the bank that actually issued the co-branded and store cards.

Additional data indicates that while loyalty programs and costs are important to card holders — regardless of card type — the relative importance consumers place on these two factors varies substantially. When asked what factors would make them more likely to prefer a co-branded card over a general-purpose card, 46% of respondents with a co-branded card said better loyalty programs, while just 26% of those without co-branded cards said the same. Twenty-six percent of those with co-branded cards cited loyalty or rewards as the most important feature, versus just 7.2% without co-branded cards. Lower interest rates are the top factor for those without co-branded cards, though the totals are closer.

CFPB officials would likely welcome the news that lower interest rates are also on the minds of consumers when they select a card. PYMNTS Intelligence data shows that 39% of those who have co-branded cards said lower interest rates was a leading factor in their decision to use a co-branded card over a general-purpose card.

Similarly, consumer watchdogs may be happy to hear that 55% of consumers with in-store cards and 52% of co-branded card holders pay the full balance due each month before interest can accrue, each larger shares than the corresponding 49% of general-purpose card holders who do the same.