The PYMNTS Intelligence report “The Role of Strategic Partnerships in Consumer Credit Cards” found that across the board, the popularity of specialized cards — especially among younger consumers — is growing. Approximately 30% of millennials and Generation Xers use co-branded cards, while 28% of those two demographic segments also carry store cards.

Generation Z consumers, on the other hand, lag behind their older peers when it comes to owning co-branded and store cards, as less than 16% of them carry either, while 59% of them own general-purpose credit cards.

How do these specialized cards differ? Co-branded cards function much the same as general-purpose credit cards, but they display a company’s brand name alongside the logo of its card network. Store cards, meanwhile, display a merchant’s branding exclusively and can only be used with that merchant.

The report, based on surveys with more than 3,000 U.S. consumers, showed that when it comes to co-branded cards, loyalty points and rewards granted in exchange for using the cards are the biggest draw for bargain-hunting consumers. As such, shoppers tend to gravitate toward co-branded cards from big-box retailers such as Amazon, Costco and Target.

Among respondents who own co-branded cards, 60% most heavily use one from a retailer affiliate —19% alone use an Amazon-issued card. Another 19% use cards affiliated with the travel industry, such as airlines and hotels.

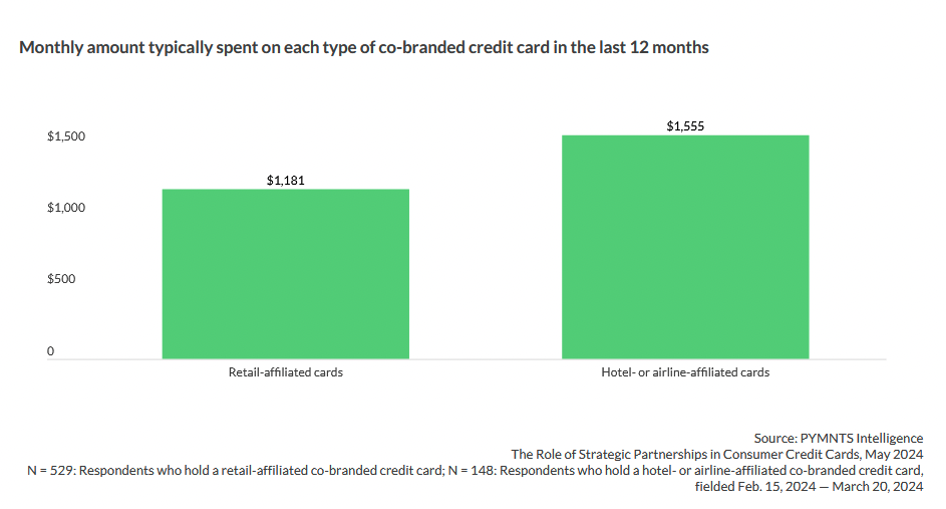

Although retail cards are more popular, travel cards garner far higher average spending. Over a 12-month period, consumers with travel-affiliated cards spent $1,555 per month, on average — 32% more than the $1,181 consumers spent using retailer-affiliated cards.

Consumers with higher incomes disproportionately hold travel cards, suggesting that well-healed consumers place an especially high value on the loyalty programs that airlines and hotels offer. These programs generally provide perks, including flights and accommodations, upgrades and lounge access, helping to reduce travel costs and deliver greater value to cardholders.

However, it is important to keep these spending levels in perspective. As the report showed, general-purpose credit cards still capture higher average spending than even travel-affiliated co-branded cards, particularly among consumers with higher incomes. Consumers with general-purpose cards spent $1,706 per month compared to $1,248 on co-branded credit cards and $761 on store cards. The gaps are even more pronounced for consumers earning more than $100,000. They spend, on average, $2,344 per month on general-use cards, $1,450 on co-branded credit cards and $1,074 on store cards.

However, it is important to keep these spending levels in perspective. As the report showed, general-purpose credit cards still capture higher average spending than even travel-affiliated co-branded cards, particularly among consumers with higher incomes. Consumers with general-purpose cards spent $1,706 per month compared to $1,248 on co-branded credit cards and $761 on store cards. The gaps are even more pronounced for consumers earning more than $100,000. They spend, on average, $2,344 per month on general-use cards, $1,450 on co-branded credit cards and $1,074 on store cards.

Retailer-affiliated cards may still hold the widest appeal among consumers — thanks largely to the rewards and other benefits they offer — but travel cards attract the highest spending levels.