While all financial institutions (FIs) operate on customer relationships, trust and loyalty can play a larger role for credit unions. According to PYMNTS’ Credit Union Innovation Index, 65 percent of credit union members said they chose a credit union (CU) as their primary because they trusted it, as opposed to 45 percent of non-CU members who said the same.

The latest Credit Union Tracker explores recent developments in the world of credit unions, and how open banking could change how credit unions do business and increase customer loyalty in the process.

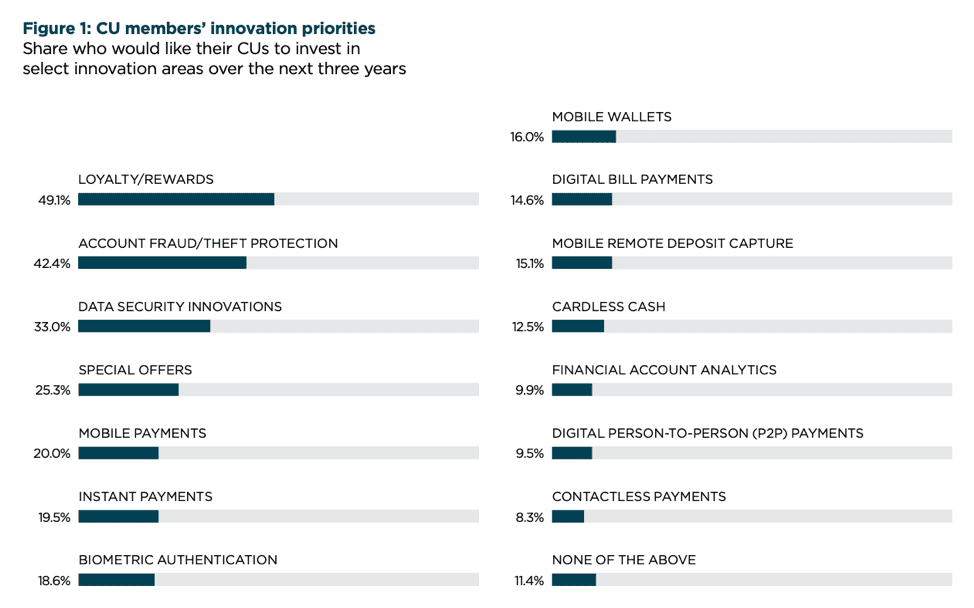

In fact, loyalty programs are members’ most loved feature. Nearly half (49.1 percent) cite loyalty and rewards as the area in which they want to see greater innovation over the next three years.

The same study, though, found that loyalty and rewards were only the seventh-most important priority among CUs, which are instead focusing on open banking options that offer anti-money laundering (AML), data security and instant payment technology.

A majority (62.7 percent) cited data security and 60.8 percent noted anti-fraud initiatives as top innovation priorities.

Open Banking Benefits

Member and CU priorities might seem at odds on the surface, though 42.4 percent of members want their CUs to invest more in security and 19.5 percent want instant payments innovations. Open banking is a solution that can solve security issues and instant payments.

The benefits of open banking are many, the most obvious being the speed of payments between FIs. Open banking is typically achieved via APIs that allow third-party developers to create tools based on the specific services and information FIs offer, ensuring that they are compatible with other banks’ procedures.

And by many measures, it appears that both CUs and members are on board with open banking.

A study found that 61 percent of consumers are willing to allow open access to their financial information in exchange for easier banking, while 77 percent of U.S. banks plan to invest in open banking initiatives this year.

Europe is ahead of the U.S., largely due to the revised Payment Services Directive (PSD2) that requires European Union (EU) banks to provide each other access to transaction data and account information. Roughly 75 percent of FIs in Europe see open banking as core to their digital transformation.

Security Issues

As cited above, a significant number of members want CUs to invest more in security. And security concerns aren’t unfounded when it comes to open banking.

Technically, releasing users’ data to third parties violates agreements between banks and customers currently, but open banking could change this or even transform security practices and create more stringent standards.

Jack Lynch, chief risk officer at PSCU, spoke with PYMNTS about how credit unions can balance the need for fraud protection without unduly inconveniencing their members. Education is part of the equation. “The more members know about changes in security and expectations for their day-to-day account activities and how their credit union is working to keep their information protected, the more seamless the experience will be for both parties,” he said.

Like many FIs, credit unions are also exploring biometrics and other new authentication and artificial intelligence (AI) technologies. CCCU recently implemented a security system that utilizes AI and pattern recognition to examine and identify fraudulent transactions. Suspicious activities are flagged for human analysts for review.

“What this system [does] is essentially tap into our operational data store, which is a copy of our core that will allow us to detect, in near real time, different anomalies with a pattern of transaction,” said CCCU’s Moran.

Beyond the never-ending battle against fraud, AI can, and already is, helping to transform the way people interact with their credit unions — from using voice assistants for customer service to chatbots for engagement.

AI-powered chatbots can create revenue-saving potential for credit unions. These automated services are on track to save roughly $8 billion annually by 2022, by some estimates.