Stock markets around the globe seem to be in freefall. Interest rates are marching higher. Sears, at least at the time this article, is prepping for bankruptcy. Consumers may feel a pinch (eventually) in the wallet, as credit card debt and mortgages become more expensive.

Beneath the headlines trumpeting the travails of consumers lies risk to the U.S. economy — possibly with ripple effects beyond its own shores, up and down supply chains — in the form of corporate debt. To be specific, those risks lie in non-financial debt. That is, the debt and obligations owed by companies that do not operate in the financial sector, such as household names, the companies that make goods and services for everyday life.

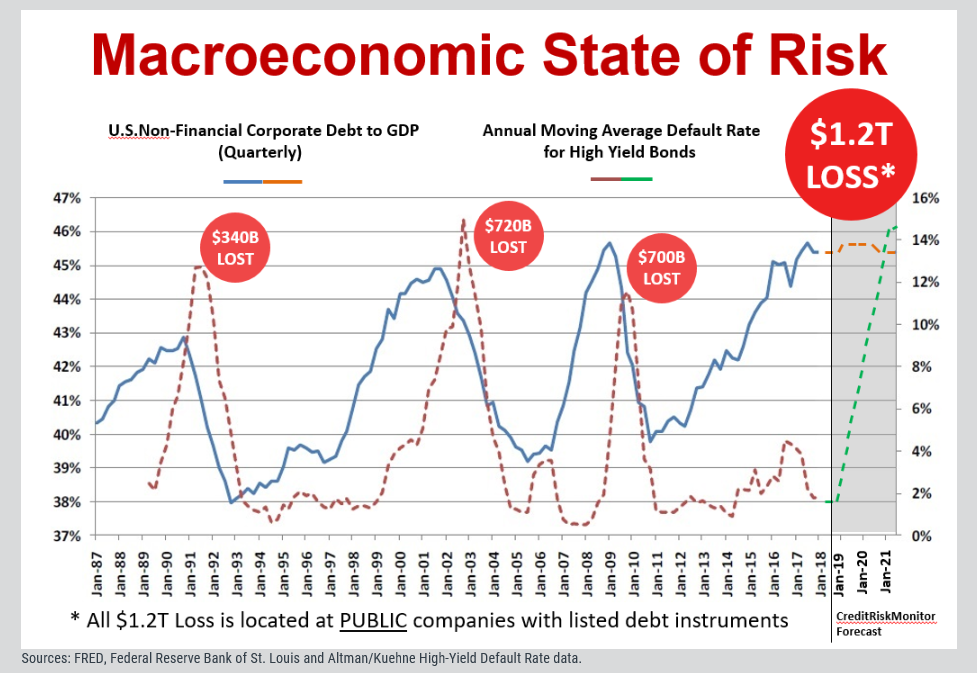

How much risk? Call it the $1.3 trillion ticking time bomb, the corporate debt amount of public companies with listed debt instruments, which Jerry Flum, CEO of CreditRiskMonitor, told Karen Webster is tilting toward default.

“Non-financial corporate debt, as a percentage of [gross domestic product (GDP)], is much higher than it was in 2007 and much higher than it was in 2001 … and, interestingly, much higher than it was in 1929,” he said.

There need be no reminder of what happened after those landmark years — namely, recession and, going back to that last demarcation point, The Great Depression. At those aforementioned peaks, just before the valleys, Flum said, “demand all looked good. [The] interesting thing at the top of stock markets and the [top] of debt markets is that the data looks great.”

First, there is the debt load — dangerously high. Then, there’s the default rate, which has been flashing warning signs, too. As Flum said, when past cycles have imploded, the default rate had reached a range of 12 percent to 15 percent.

In the chart below, which he presented to PYMNTS, that level might be seen (measured as the Annual Moving Average Default Rate for High Yield Bonds) over the next several months. For now, the data looks reasonably OK, he said, even with the debt load of about $9 trillion on the books.

That’s a lot of money, of course. To put it into perspective, the total GDP of the country stands at around $19 trillion dollars.

“I don’t think people truly understand the magnitude of the indebtedness that has gone on,” he surmised.

Where The Risk Is … And Where It Isn’t

The CreditRiskMonitor forecast comes as companies are borrowing too much so they may conduct operations, make sales and meet expenses. It’s known as working capital and, as Flum told Webster, the risk lies with public companies, not the smaller private firms that investors and observers may look to when they think about risk.

The smaller enterprises, he said, don’t have the size, or five years of certified financials, so that they can take on significant borrowings.

The story becomes one of misperception and miscalculation over the size and magnitude of the debt, and the size of the defaults that loom — “and there is very little one can do about it,” he cautioned Webster. When a company misses an interest payment or a principal payment, bankruptcy suddenly becomes a real option.

Why They Take On Debt

In terms of standard practices, he said, credit managers at the larger corporations are the ones who control working capital, using debt because inventory is not easily converted to cash, and they ship on credit. Credit is the bulk of working capital. When the supply chain or individual business partners decide they do not want to extend credit, “they can make life miserable for a company and put it out of business very quickly.”

Now: How We Grow And The Third Variable

Looking at the present and near term, Flum noted the debt levels are so high that, “no matter how good things look, the underlying assets cannot handle the debt that’s been laid on” during expansion and generally good economic times. To get to those good times, GDP grows by three variables, he told Webster.

First, there is population growth (at an average of 1 percent here in the U.S., measured annually), which can increase demand for, say, more cars on the road. Second, there is efficiency of production, which grows about 1 percent to 1.5 percent a year. Last, there is debt, the third variable. Debt allows people or companies to take money and go make a future purchase — a car, for example, to use the aforementioned case — that they do not have enough income or savings to acquire otherwise. It’s future demand, moved into the present tense.

“They are stealing a little bit of the demand a couple of years out,” he said, while overstating demand in the present tense. The incremental debt is the driver. He added, “At some point, it takes more and more debt to produce an incremental dollar of GDP. It may take a couple of dollars to bring an incremental dollar of GDP, and it is unsustainable.”

That has been possible into the present day because governments have kept rates artificially low, below what the markets would determine to be a risk-adjusted rate of return.

However, “trees do not grow to the moon,” said Flum. “Huge stability creates instability. It’s [an] art of the human condition, and happens every 70 or 80 years, going back a few thousand years.”

When The Music Stops

So, what happens if it’s all unsustainable? Picture the Road Runner cartoon — and the hapless coyote who always overshoots the canyon in pursuit of his prey, looks down and … that’s when the fall happens.

“We are over the side of the canyon,” Flum said, with a nod to the “Looney Tunes.”

Pinpointing exact timing is elusive, due in part to the madness of crowds (witness the stock market where people buy high and higher, yet buy less shares as they go down). When the consequence is losing the hose or the business, one needs to be less concerned with when.

“There is no one who has lived through where we are today,” he told Webster, as interest rates are effectively negative on the debt. “Negative interest rates have never happened before in recorded history.”

The argument for those rates is a deflationary depression, he said. There’s $8 trillion of that debt sloshing around the system now, held by sophisticated professionals.

The Read Across

The read across is that managers, and those who manage lending portfolios, must make adjustments as they conduct day-to-day commerce on how they manage their goals and to whom they lend. They also need to know who is risky and should not be lent money.

For the credit manager, the principle is good faith — that they will get paid 60 days later. They haven’t changed their actions, and if they do not, they’ll get hurt, he said.

Sears is a prime example, with a possible bankruptcy at this writing. The beleaguered retailer’s suppliers know that in a possible Chapter 11, when the company reorganizes (this is, of course, hypothetical), the firm will not deal with those who abandoned it. That means those suppliers lose presence on the shelves, so they will be satisfied with being paid pennies on the dollar, if at all … and the ripple effect goes up and down the supply chain.

“Wherever we are [at any] point in the future, the [company will divide] whatever assets, whether trade-credit-extended stock prices, the price of bonds or the price of loans. All of those things will come down dramatically in value and that will be the bottom. That is the time that we should be extending more trade credit,” Flum said, “and forming automatic payment programs, because the end person guaranteeing that payment is still going to be around. … In the meantime, you need to stay out of the way of people who can hurt you.”

Watch for the fall, he said. The heavily indebted companies are the ones that are going to collapse. However, before they do, they are going to cut their prices and a shakeout is in the offing.

“Debt is the catalyst of all this,” he said.