Authorized push payment (APP) fraud, identity theft, synthetic account fraud and first-party misuse are all growing problems for many industries and countries. In the United Kingdom, financial loss from APP scams, which involve fraudsters deceiving individuals into sending payments to bank accounts that the fraudsters control, increased 39% year over year in 2021. For the first time, APP overtook credit card fraud in terms of the most money stolen, with cases skyrocketing 71% through the first half of last year.

Fraud using stolen identities to open new bank accounts grew by 64% in 2021. Synthetic account fraud, a newer form of identity fraud in which bad actors open accounts using a combination of stolen and fabricated identities — such as an actual Social Security number under a fake name — represents one of the fastest-growing financial crimes in the United States. First-party misuse, such as credit card chargebacks, can plague merchants with lost revenue. PYMNTS research found that 50% of merchants say costs incurred from chargebacks are the biggest problem they face.

Digital Authentication Solutions Aim to Deliver Trust, Reliability

Digital authentication technology is crucial in the fight against fraud, especially for APP and synthetic identity fraud. PYMNTS research found that acquiring banks are especially interested in artificial intelligence (AI), with 60% saying that AI is their most important technology for detecting fraudulent transactions. They are using other technologies as well, with 27% citing rules-based algorithms as their most important anti-fraud tool.

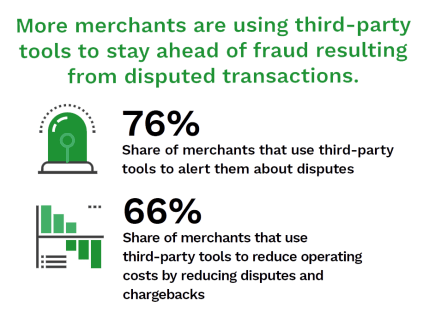

Specialized third-party tools can also help merchants resolve disputed transactions resulting from first-party misuse in ways that internal solutions cannot. Third-party tools’ advanced dispute resolution capabilities help limit merchant losses to 0.32% of annual revenues compared to 0.46% of revenues lost by merchants that rely solely on in-house systems.

Biometrics has exploded in recent years. A study found that the number of U.S. businesses using biometric authentication to prevent fraud has nearly tripled from 27% in 2019 to 79% this year. Consumers have also become believers, with 58% saying that biometric methods are faster and more convenient than other login methods and 55% saying they trust biometrics more than these alternatives.

Consumers and Regulators Want More Security, but What About Convenience?

PYMNTS research found that security is highly important for 83% of consumers, while 53% said consistent experiences across different platforms have a very or extremely big impact on their trust in financial institutions. These sentiments are shared by regulators, who are increasingly issuing guidelines for uses of authentication technology. Some industry representatives worry, however, that government regulations that focus too heavily on security could handcuff their ability to deliver convenience.

According to recent data, six out of 10 consumers who use peer-to-peer (P2P) payment platforms cited ease of payment as the leading reason, but the more they use P2P services, the more likely security becomes an issue. P2P users are 47% more likely to have been the victims of scams when they use the platform multiple times per week. Regulators are homing in on the issue of consumer fraud losses, but the banking industry is concerned that stiffer regulations could stifle innovation or create more friction for users.