The extent of paycheck-to-paycheck living — and the nuances within that broad categorization — are becoming more relevant and critical to consumers now than at any point in decades given a painful convergence of economic recovery slowed by war, disease and economics.

Reaching from lower five-digit incomes to those of $250,000 per year or more, the ranks of consumers whose finances are stretched are increasing, as is the need for awareness of alternatives and financial tools that help when every single paycheck is a lifeline for households.

In “New Reality Check: The Paycheck-to-Paycheck Report – The High Earners Edition,” a PYMNTS and LendingClub collaboration, PYMNTS surveyed over 4,000 U.S. consumers and found the problem widespread, and with interesting variations in how the affluent approach the issue.

The following data points are expanded in the full report.

Get the report: The Paycheck-to-Paycheck Report – The High Earners Edition

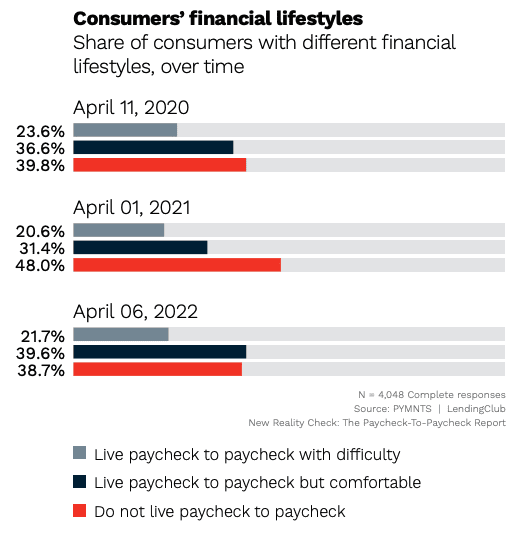

- In April, 61% of consumers lived paycheck to paycheck.

While April saw a slight improvement in the number of consumers living paycheck to paycheck on a month-to-month basis, the more concerning number is the year-over-year comparisons and the trend seen there.

As the study stated, although “consumers living paycheck to paycheck decreased slightly in April 2022, it has risen year over year. Forty-two percent of consumers earning more than $100,000 per year reported living paycheck to paycheck in April 2022, a decrease from 49% in March, but an increase from 40% in April 2021.”

Close to one in four (36%) earning $250,000 or more annually lived paycheck to paycheck “as did those earning between $200,000 and $250,000 per year.”

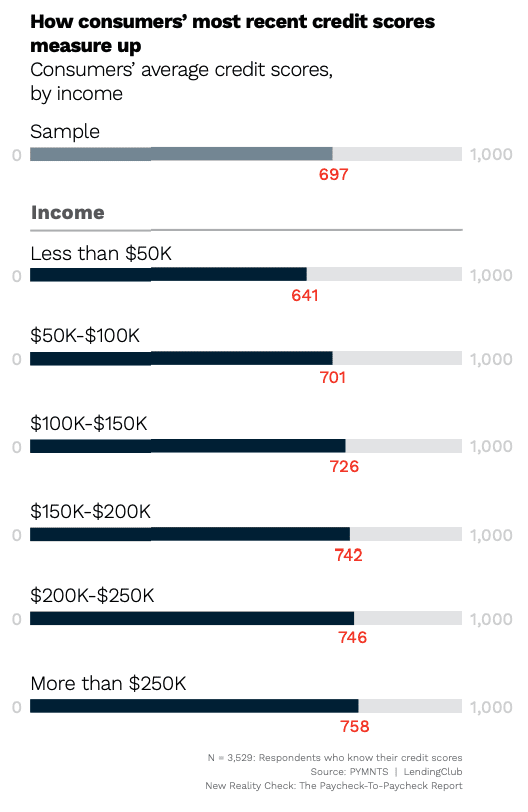

- Only 18% of those earning less than $50,000 have an above-average credit score.

Finding a powerful and not unexpected correlation between annual earnings and credit scores, The High Earners Edition of this study series noted that “63% of those earning more than $250,000 a year report having an above average credit score. The average credit score for these respondents is 758. Yet, our data also finds that 18% of consumers earning more than $250,000 a year report having an average credit score, while 13% report having a below average credit score.”

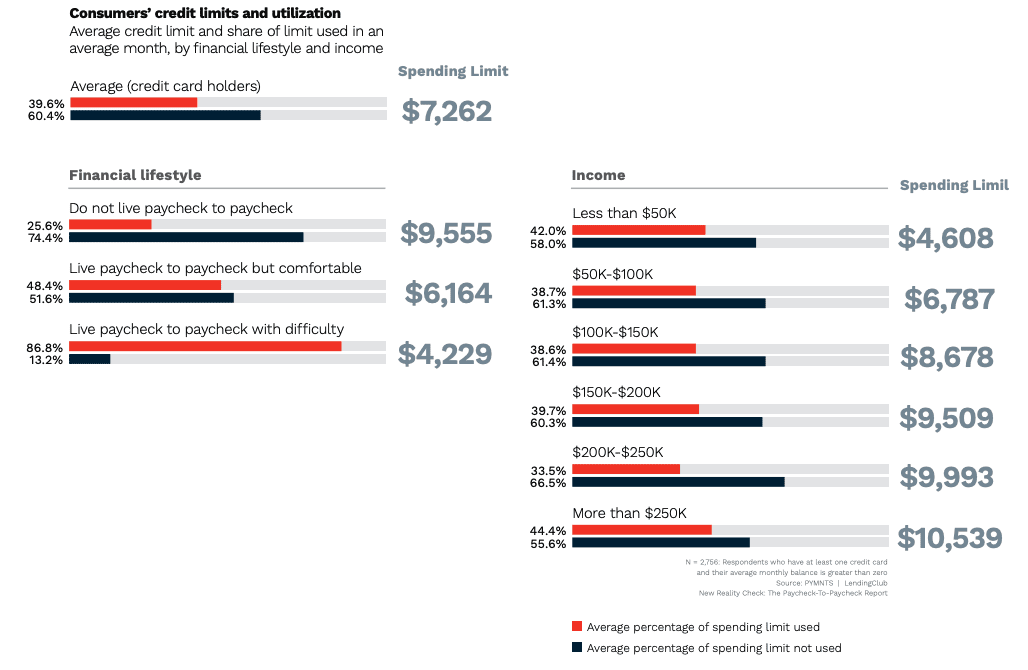

- The average U.S. consumer uses 40% of their available credit card limit monthly.

Americans use 40% of their monthly credit card limit, which “is higher than the 30% recommended for perceived creditworthiness,” the study stated. “With an average credit limit of $7,300, the average U.S. consumer spends $2,900 per month across two credit cards.”

Things shift considerably among those earning $200,000 a year and above, as PYMNTS data shows that at least 60% of paycheck-to-paycheck consumers who earn over $200,000 “never” or “rarely” revolve their credit balances, “compared to 51% of paycheck-to-paycheck consumers who earn between $150,000 and $200,000 and less than half of paycheck-to-paycheck consumers who earn less than $150,000.”

Get the report: The Paycheck-to-Paycheck Report – The High Earners Edition