Just a few weeks from now, federal student loan payments resume, ending a moratorium that had been in place since the onset of the pandemic in March of 2020.

And as October looms, borrowers are girding for the impact of carrying hundreds of dollars of more in monthly expenses tied to those obligations.

Wall Street’s girding for the impact too — particularly when it comes to companies that are reliant on discretionary spending from those borrowers.

As PYMNTS reporting has shown, 90% of consumers with student loans expressed concern about payments resuming, with nearly all of those owing more than $100,000 likely to feel some outsized impact.

Disposable Income Hit — and a Savings Pinch, Too

Key to those concerns is reduction in disposable income, and the hit to savings that are likely to be twin pressures on consumers’ ability to keep spending at their favored merchants. In the case of the latter, we’ve found that 46% of consumers with loans who are concerned about repayments resuming anticipated that saving money will become more challenging. Additionally, 43% expressed worries about their financial stability, while 36% were concerned about paying monthly bills.

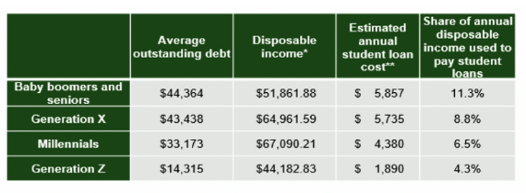

In reference to the disposable income “hit,” separate PYMNTS research has estimated that all demographics will see some hobbling of their spending firepower. Government data shows that 45.9 million individuals in the U.S. — 17.6% of the total population — have student loans, equating to $1.7 trillion in debt. Our chart below shows that there’s an average of $44,000 per borrower for older generations, and where more than 11% of their disposable income goes to satisfy that obligation. Millennials and Generation X have more disposable income, and so the debt obligations run to a range of 6.5% to 8.8% of disposable income.

Wall Street’s Caution

Sell-side firms on Wall Street have been downgrading their assessments — the ratings and the target prices — of select names that may endure some revenue headwinds in the months ahead, and right into the holiday shopping season.

In one example, from late last week, Moffet Nathanson downgraded DoorDash. As Investor’s Business Daily reported, analyst Michael Morton downgraded the name to “market perform” from “outperform” and wrote that “we consider food delivery, at a (roughly) 60% price premium to picking up an order in store, to be one of the most discretionary behaviors of an average consumer,” and added that “the average student loan bearing consumer is about to experience a 14% to 19% hit to their discretionary spending power, resulting in near- to medium-term risks to DoorDash’s bookings.” Most of DoorDash’s key demographic — at ages 25 to 44 — are going to be shouldering a renewed debt repayment schedule.

And as noted here last month, consensus estimates and various ratings had already been coming down in the weeks ahead of Target’s earnings, tied in part to caution over student loans. The company saw its second-quarter comparable sales decline 5.4%, mainly in discretionary categories. And back in July, Piper Sandler downgraded American Express stock to underweight from neutral. “We expect a sharp change in spending habits which ultimately will accelerate the slowdown in spending we have observed” in 2023 and “make it increasingly difficult” for the company to meet its annual target of 10% revenue growth in 2024 and 2025, per the note penned by analyst Kevin Barker.