In another PYMNTS first, we’re going to bring you weekly scoop on ALL of the investments in the payments space – VC funding, strategic investments, buybacks, acquisitions – for both retail and commercial payments. This week we summarize all that happened in the month of June (Psst….there was $6.37 Billion flying around in investment activity).

In another PYMNTS first, we’re going to be reporting investments in retail and commercial payments companies and in particular who’s getting funding, from whom, and how much; and who’s getting acquired, by whom, and how much. There’s nothing out there like this. Every week we’re going to consolidate a number of reports on the financial doings of the sectors that are innovating and reinventing right before our very eyes.

Here’s what happened in the month of June:

The Big Takeaways for Payments and Commerce

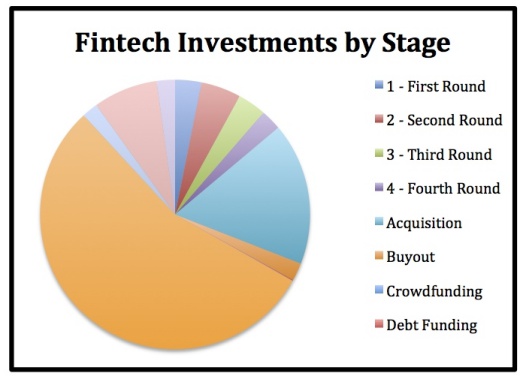

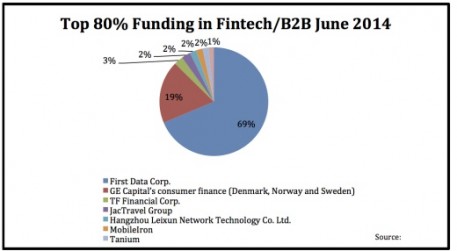

- $6.37 Billion in financial activity was observed across a variety of investment types – VC funding, private placements, etc. Of that total, $2.1 billion was the driven by strategic or venture –backed investments; $4.4 Billion was attributed to 2 big transactions – an acquisition by Santander in Europe ($952 Million for GE Capital’s Consumer Finance Group in the Netherlands) and investments into First Data by KKR ($1.2 Billion ) and private investors ($2.3 Billion) in the US.

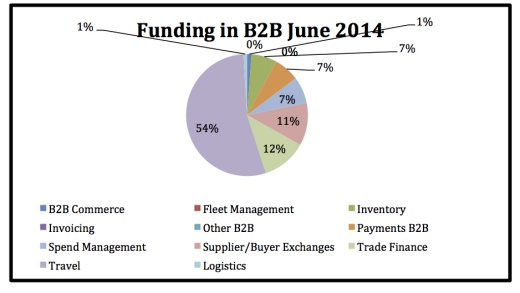

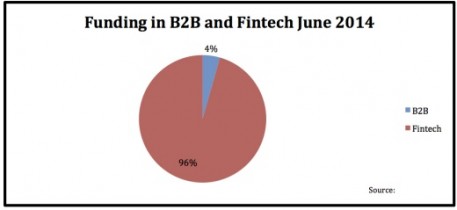

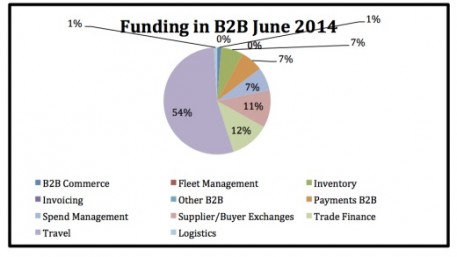

- Perhaps not surprisingly, as a result of that activity, 96 percent of the month’s activity was concentrated on the retail payments side. The bulk of the activity overall was therefore, concentrated in the alt.banking/credit/payments on the retail payments side (80 percent). Travel/spend management drove the investments on the commercial payments side (54 percent).

- Venture backed and strategic investments on the retail payments side accounted for ~$1.5 Billion of the total investment activity in June. Of that, nearly as much was considered strategic investments and not tied to a capital raise ($492 Million) than Series A and B capital raises combined ($523 Million).

- Interestingly, most of the venture and strategic backed investments were in the data analytics and security areas accounting for 58 percent of the total. Mobile money ($9.6M), digital wallets ($33M), POS systems ($4.6) and prepaid($1.8) reflected the least amount of investment activity.

- The most active VCs included Andreessen ($123 Million), Vitruvian Partners ($135.7 Million) and Index Ventures ($108 Million).

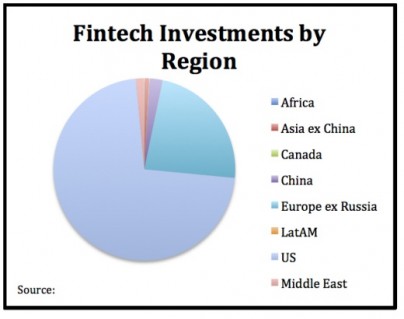

- From a geographic perspective, China was the least active geography and the US was the most active.

- The median investment amount was $4 Million.

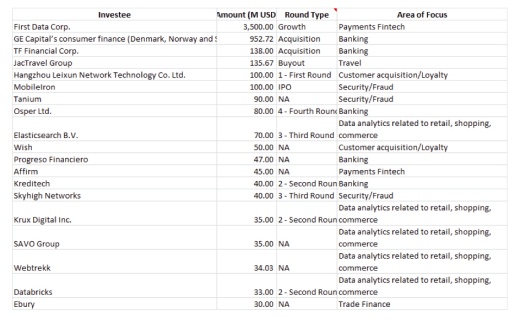

The Retail and Commercial Payments Top 20

Here are the top 20 investments that drove 80 percent of the funding activity in June 2014.