It was Irish playwright G.B. Shaw who purportedly said, “the United States and Great Britain are two countries separated by a common language.” We can now add payments to Shaw’s dictum.

Innovating Cross-Border Payments: What US and UK Businesses Need to Know, a PYMNTS and Visa collaboration, is based on a study of 456 businesses in the U.S. and U.K. that either sent or received cross-border payments between Nov. 12, 2020 and Dec. 4, 2020. Researchers found that U.S. and U.K. businesses have much in common — not all of it good.

“Cross-border payments take far longer to receive than domestic payments” in both countries, per the study, “potentially putting a strain on cash flow for those businesses that increasingly rely on sales outside their domestic markets. The average days sales outstanding (DSO) reported for domestic B2B payments received by the businesses in our sample was 21 days; for cross-border business payments it is 32 days — 55 percent longer.”

What’s more, U.S. businesses wait an average of three days longer than their U.K. counterparts — averaging 33 days for U.S. firms compared to 30 days in the U.K. — “highlighting the differences in the payments rails and infrastructures that are available to businesses and their trading partners to move money between bank accounts across borders.”

Frictions clearly persist in a payments ecosystem that craves speed and certitude. Cross-border pain points causing lags are firmly in the crosshairs of corporates as they turn to real-time rails, application programming interfaces (APIs) and unified platforms to nudge funds along.

Transaction Clarity Rises To The Challenge

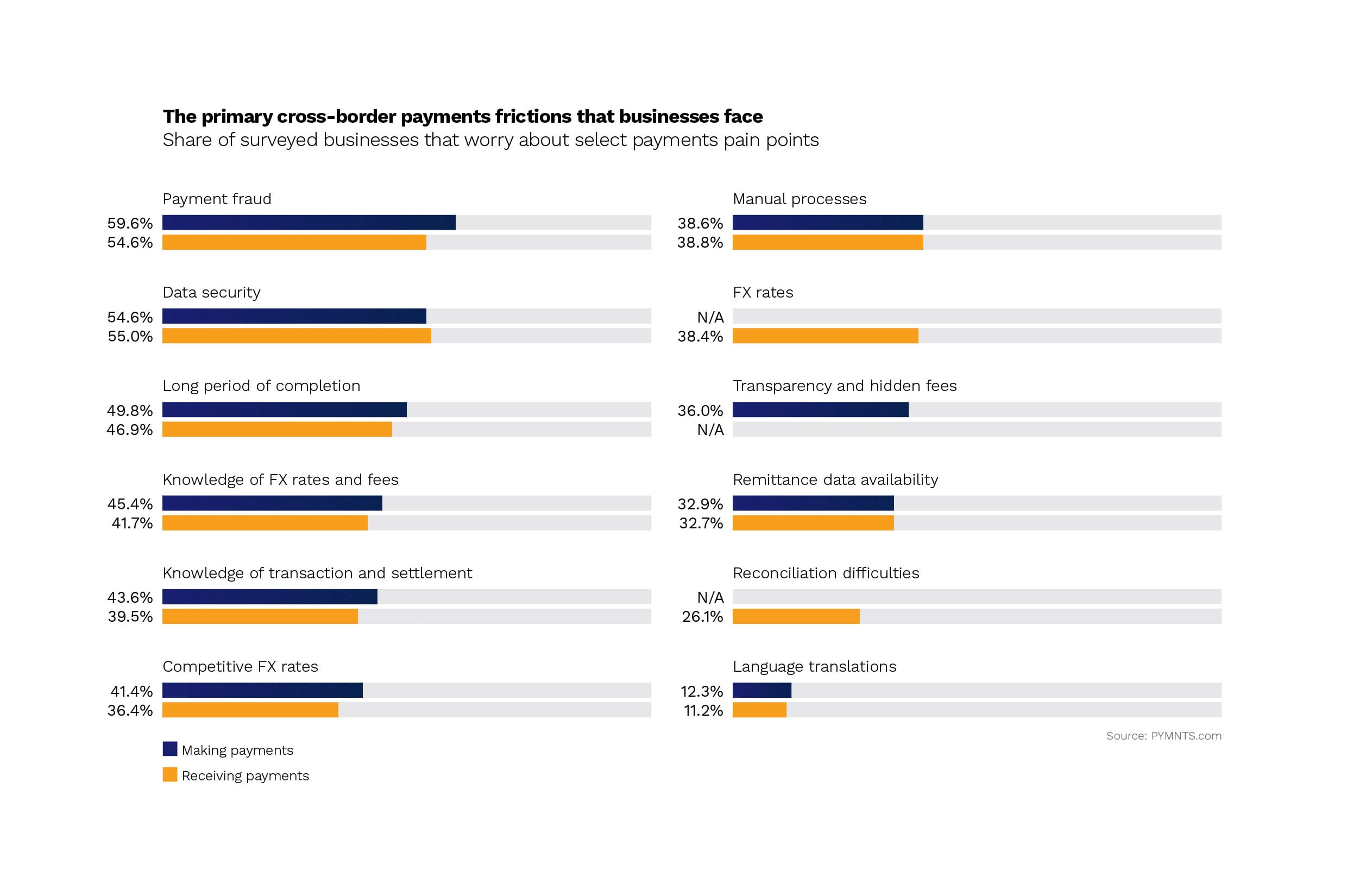

Correspondent banking is responsible for some of the more serious delays, with Innovating Cross-Border Payments finding that it “increases days sales outstanding by seven days for suppliers and is an acute pain point for smaller U.S. businesses,” adding that the extra time and effort it takes to transfer funds “through a web of correspondent banks also increases their FX risk, and the U.S. and U.K. businesses in our study that cite FX rates as a payments friction also report waiting seven days longer to receive payments than average.”

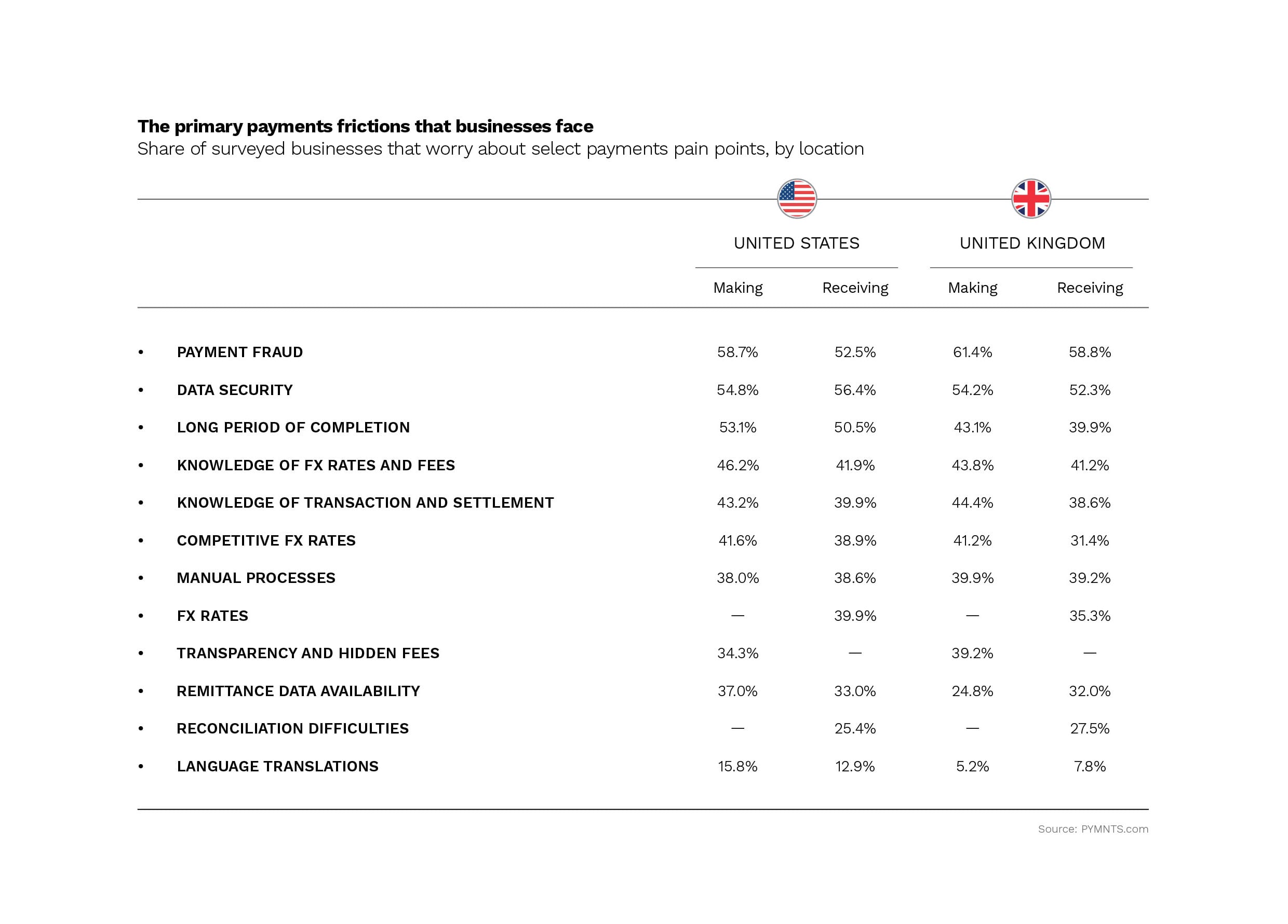

More than a third of mid-sized businesses in both countries said the inability to attach detailed remittance data to a payment, and the time spent reconciling to invoices, creates yet more drag. That puts transaction clarity front and center for businesses and consumers in 2021.

“A lack of transparency into the payments experience can also exacerbate cross-border frictions for businesses in both countries, leading to uncertainty for payment decision-makers who, absent that visibility, are unable to accurately forecast their cash positions,” Innovating Cross-Border Payments states. “Correspondent banking fees and FX fluctuations can also contribute to this lack of clarity, and each friction was noted as a concern by 42 percent of U.S. businesses and 41 percent of those in the U.K. when receiving payments.”

Real-Time Roadmaps

With 2021 emerging as the unofficial year of cross-border payments, businesses on both sides of the pond are zeroing in on processes that emphasize security, efficiency and velocity.

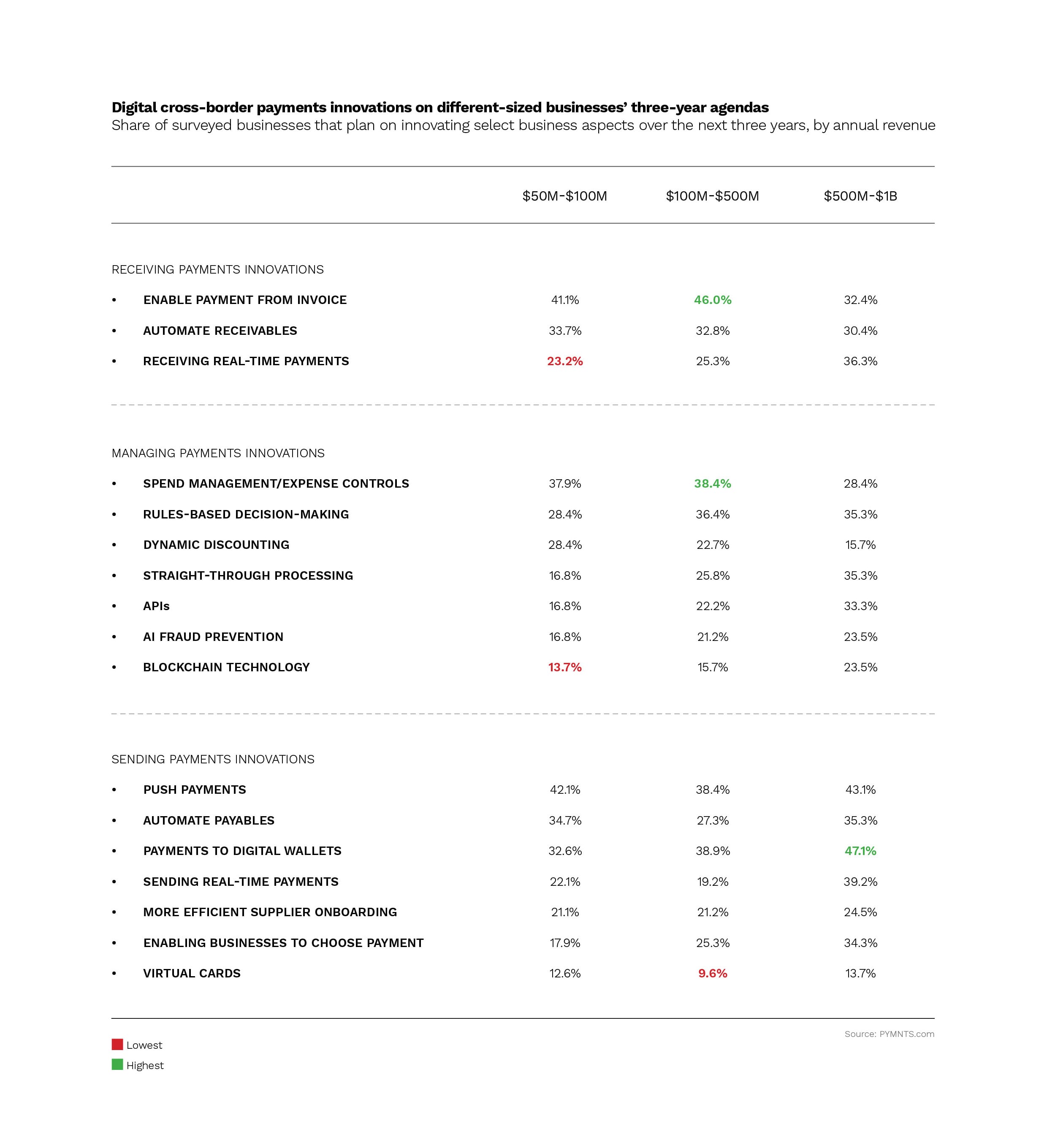

According to Innovating Cross-Border Payments: What US And UK Businesses Need To Know, “44 percent of the largest businesses in our sample report plans to offer real-time payments in the next 12 months but has not yet begun implementing them. Meanwhile, 25 percent of the largest U.S. businesses and 33 percent of the largest U.K. businesses say their implementations are already underway or live.”

A three-year roadmap for innovation laid out in Innovating Cross-Border Payments finds that larger companies in the U.S. and U.K. focus primarily on real-time and API integrations — 33 percent of larger businesses plan to optimize and use APIs within the next three years, while 22 percent of mid-sized businesses and 17 percent of smaller businesses plan to do the same.

Small and medium businesses (SMBs) have a slightly different agenda for modernizing cross-border payments, with the report noting that SMBs tend to focus on automated receivables and dynamic discounting. “Businesses generating less than $50 million in annual sales are the most likely to invest in automated receivables and dynamic discounting in an effort to automate early-payment discounts for their suppliers.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More