The pandemic has thrust virtual channels into the spotlight as consumers all over the world have migrated online during shutdowns and operational restrictions. This digital shift has highlighted the many conveniences of eCommerce transactions, leading to permanent behavioral changes among merchants and consumers alike. For example, 64% of B2B buyers expect the ability to pay for their purchases online, and 56% demand several payment options.

Virtual cards are one notable payment option, and their growing momentum in the business-to-business (B2B) space cannot be ignored. Companies can incorporate virtual cards into their B2B payment processes to improve cash flow, enhance security and enable accounts payable (AP) automation more seamlessly than when they rely on clunky, antiquated methods such as paper checks. Enabling virtual card acceptance through accounts receivable (AR) automation also can increase efficiency and help businesses capture large spend opportunities.

B2B transactions will account for 71% of virtual card transactions, even though B2B sales will represent a mere 1% of all transaction volume. The few transactions that do occur are very high value, however, making them enticing fraud targets and higher stakes transactions for B2B companies. As such, B2B sellers and their vendors would be wise to automate and secure these features to accelerate larger payments as safely and proficiently as possible.

Vendor Payments Drive up Fraud, Operational Inefficiencies

Bad actors have taken advantage of the uptick in digital transactions since the pandemic’s onset to launch numerous schemes. In fact, business email compromise (BEC) fraud attacks targeting invoices and payments rose 155% between Q2 and Q3 2020. A recent survey also revealed that nearly half of all organizations reported severe fraud attempts on their systems in 2021, and 15% suffered major financial losses as a result. Inadequate AP processes contributed heavily to such attacks, with 54% of firms reporting that their AP departments were targeted. Perhaps most shockingly, 69% of these attacks were carried out by bad actors impersonating existing or new vendors.

Vendor payments remain a major pain point for B2B companies, especially for those still using time-intensive, inefficient and often error-prone manual processes. One-quarter of AP professionals report that manual administration negatively affects their relationships with third-party vendors, yet nearly 25% of all B2B payments still are being made via paper checks. While it is true that a growing number of businesses are leaning favorably toward digital payment methods, a significant portion of organizations continue to forgo digital options that could help them better meet their vendors’ payment expectations.

Digitization Leads to Increased Frequency of Virtual Card Use

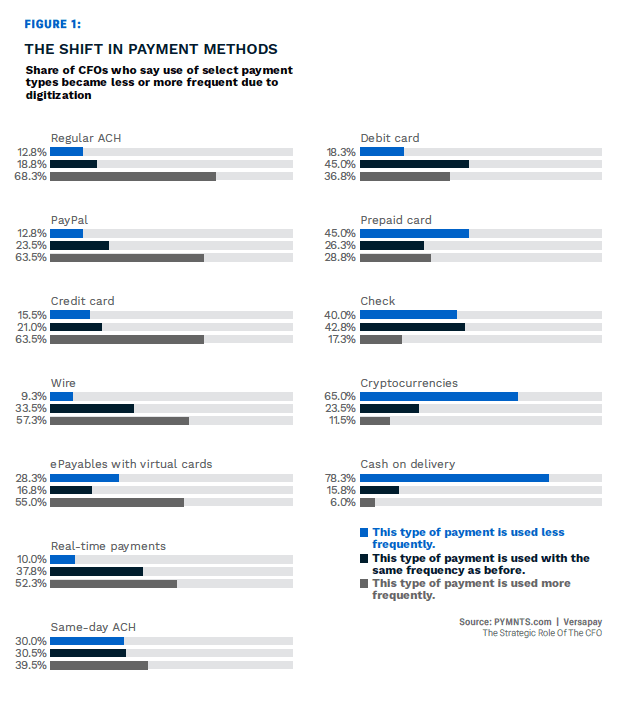

Accelerated digitization inspired a series of financial experiments, many of which have pro ven staying power. Cash, checks and physical debit or credit cards were the most commonly used payment methods before the pandemic, but 55% of CFOs now say ePayables with virtual cards are used more frequently because of digital innovation, for example. Use of manual methods is trending in the opposite direction, with 78% using cash on delivery less frequently and 40% reducing their paper check usage.

ven staying power. Cash, checks and physical debit or credit cards were the most commonly used payment methods before the pandemic, but 55% of CFOs now say ePayables with virtual cards are used more frequently because of digital innovation, for example. Use of manual methods is trending in the opposite direction, with 78% using cash on delivery less frequently and 40% reducing their paper check usage.

Digital cards also continue to gain traction in the AP arena, driven in part by hospitality sector businesses and their recognition of the convenience of card-on-file procedures for their vendors. PYMNTS’ data shows that electronic B2B payments within the hospitality industry increased 300% between January 2020 and May 2021, with more suppliers accepting physical or virtual card transactions as well as non-card-based options, such as ACH transfers. This trend extends far beyond restaurants and hotels, however. Approximately 64% of all companies are making more than half of their B2B payments electronically, and only 28% still are processing transactions manually.

B2B executives have expressed growing confidence in electronic payment methods, with 47% citing efficiency as the driving force behind their adoption of new automated payments solutions. ACH remains the most sought-after electronic payment processing tool, but 28% of company leaders also plan to invest in virtual cards in the near future. Such investments can help AP departments ensure their vendors are paid in a timely manner despite pandemic-related operational hiccups.

One feature that sets virtual cards apart from other electronic payment methods, however, is their ability to offer integrated security features. Unlike traditional debit or credit cards, digital cards rely on tokenization to process the cardholder’s transactions, creating a unique and randomly generated single-use code to process each payment. The risk of fraudsters acquiring the data used to conduct a virtual card payment — and being able to leverage these details if they do — is astronomically low compared to physical card transactions, and its digital footprint makes suspicious activities easier to track. This is particularly meaningful for businesses, because high traffic can often result in difficulties detecting fraudulent behaviors.

Virtual cards have a promising future as a secure, convenient B2B payment method, even when compared to debit-based ACH, which currently is the frontrunner in the electronic payments space — ACH debit accounted for 34% of payment fraud in 2020, while virtual cards accounted for a mere 3%. B2B companies that have not done so already should consider incorporating virtual cards into their daily operations to decrease fraud, improve vendor relationships and provide more insight into companywide spending.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More