Although this digital shift impacts nearly all aspects of banking and finance, the rise of digital payments stands out. Both individual consumers and companies increasingly use, expect and, in many cases, need digital payment solutions, and they are expecting financial institutions (FIs) to provide them.

However, not all digital payment solutions will do. Informed by the quick, convenient experiences they encounter on the internet, consumers expect similarly seamless, digital-based payments experiences — the kinds that embedded finance can provide. This month, PYMNTS examines how consumers’ and businesses’ digital payments expectations are evolving and how FIs can leverage embedded finance to create better digital payment experiences.

Digital Payment Use Is Strong and Growing

Consumers are using digital payment channels like never before. For example, more consumers are using digital wallets. Of consumers who reported that their payment habits changed due to the pandemic, one-quarter said they are using digital wallets more frequently than they were a year ago.

In another study, 42% of consumers reported having made a payment through a digital wallet, such as Apple Pay, in the past six months. The same study also underscored the widespread use of other digital channels. For example, 23% of consumers made a payment directly through a social media platform, and 19% purchased something within a video game or other virtual space. No matter the channel, consumers want their payment experience to be secure, fast and seamless.

Businesses have similar expectations for digital payments. Like consumers, they want to use digital channels to pay their suppliers and other businesses, and they expect FIs to provide this functionality. Furthermore, with customers wanting to pay for goods and services through seamless digital channels, businesses are looking to provide digital solutions. So far, many have been largely successful. As of October, 61% of merchants were supporting digital wallets at checkout — yet businesses know they need to do more. That is why they want FIs to provide solutions they can easily integrate into their existing infrastructures and product offerings.

Consumers Want Embedded Finance, Whether They Know It or Not

At first glance, it might appear that most consumers do not want or care about embedded payments or embedded finance. For example, nearly half of consumers have never heard the term “embedded payments.” Of the 51% who had heard the term, 23% did not understand what it meant.

Another report found that approximately one in 10 consumers are familiar with embedded finance. Nonetheless, many consumers are currently using embedded experiences whether they know it or not. Nearly one-third of U.S. consumers have used embedded payments just through using rideshare apps, and more than 40% of consumers have used digital wallets — two notable examples of embedded payments.

Embedded Finance Has More to Offer

Although consumers and businesses are already leveraging embedded finance to great effect, it still has more to offer. Many consumers want further functionality that would require embedded finance. For example, nearly half of consumers said they would likely use banking services provided by their streaming providers, internet providers and even their employers. The same study found that more than one-third of consumers are interested in using digital or social brands to send money to their friends.

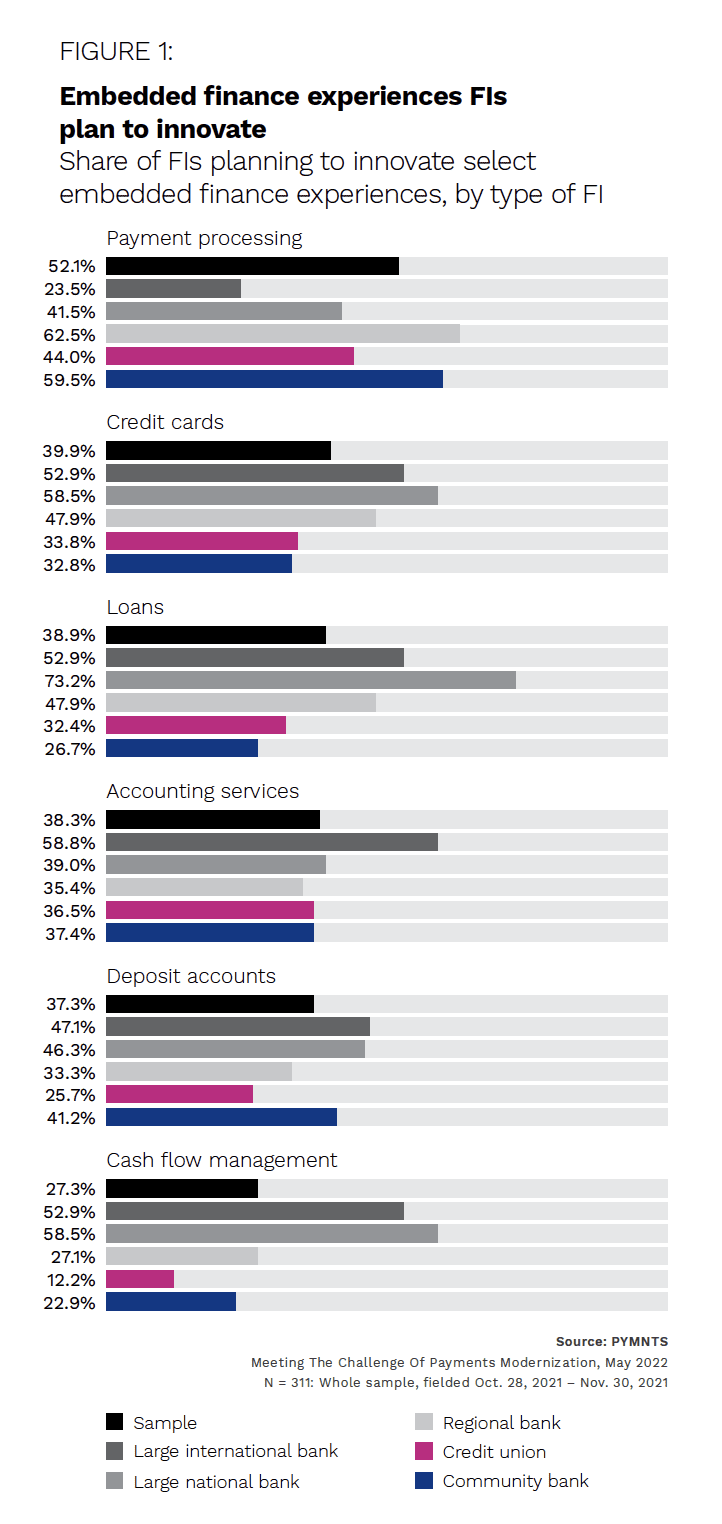

FIs are aware of embedded finances’ potential. According to PYMNTS’ research, 92% of FIs reported they are planning to innovate or are currently innovating embedded finance experiences. As the need for seamless digital experiences continues to grow, embedded finance can and will increasingly be used to provide these types of solutions.

The banking and financial services industry is undergoing a rapid digital transformation. In response to the pandemic and the emergence of new technologies, consumers are rapidly exchanging traditional financial products and services for innovative digital solutions.

The banking and financial services industry is undergoing a rapid digital transformation. In response to the pandemic and the emergence of new technologies, consumers are rapidly exchanging traditional financial products and services for innovative digital solutions.