Cross-channel integration has become table stakes for financial institutions (FIs), as consumers expect to find it easy to transact, make payments and see transaction histories across accounts and channels.

By and large, most FIs seem to be delivering what’s needed, according to “The Future of Authentication in Financial Services,” a PYMNTS and Entersekt collaboration.

Get the report: The Future of Authentication in Financial Services

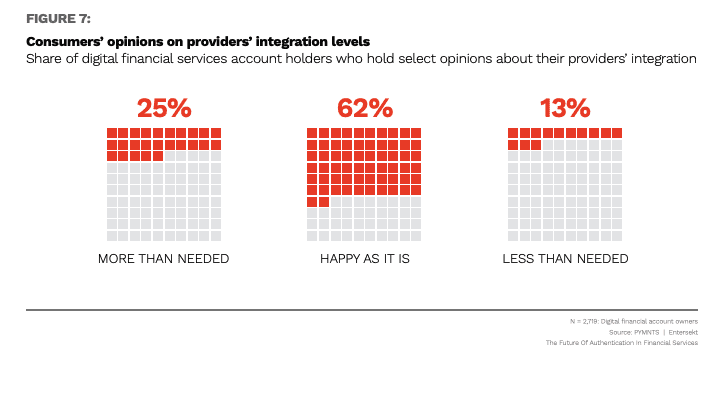

Sixty-two percent of consumers said they believe that their FIs provide the right amount of cross-device account integration, explaining they’re “happy as it is.”

Just 13% of consumers said they want deeper integration, while 25% of consumers said their providers’ integration levels are more than needed.

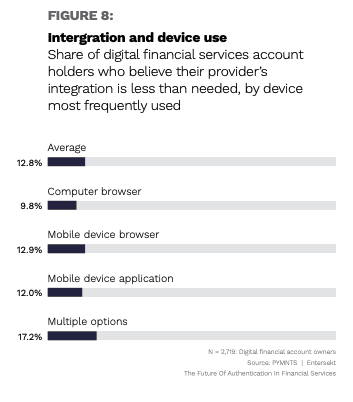

The demand for deeper integration changes based on the type of devices consumers use to access their digital financial services accounts.

The demand for deeper integration changes based on the type of devices consumers use to access their digital financial services accounts.

Those who most frequently use a computer browser to access their accounts are most satisfied, with only 10% saying their providers’ integration is less than needed.

Consumers using a mobile device application are slightly more satisfied than average, with 12% saying the integration is less than needed.

Users of mobile device browsers align with the average, as 13% said they’d like to see deeper integration.

Consumers who use multiple channels to access their online financial accounts are most likely to wish to see more integration from their providers. Seventeen percent of these consumers said their current levels of integration are lower than what is needed — exceeding by four percentage points the average share of 13%.

The ability to view accounts anywhere and at any time is more than just nice to have — it is an absolute must for modern consumers — so financial services providers should offer the tools consumers want to use.

Whether considering a browser from a computer, an app on a mobile device or multiple methods in concert, these providers will be judged on their integration between methods of account access and their ability for consumers to easily view account information whenever, wherever and however they want.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More