Middle-market companies (those with sales from $20 million to $1 billion) have been relatively slow to adopt real-time payment (RTP) technologies, even though they recognize and value the advantages. Their greatest concern about the method of payment is the biggest hurdle to adoption. Yet “Accelerating The Time To Realized Revenue,” a PYMNTS study in collaboration with Mastercard, indicates that this objection may be more myth than fact.

Get the report: Accelerating the Time to Realized Revenue

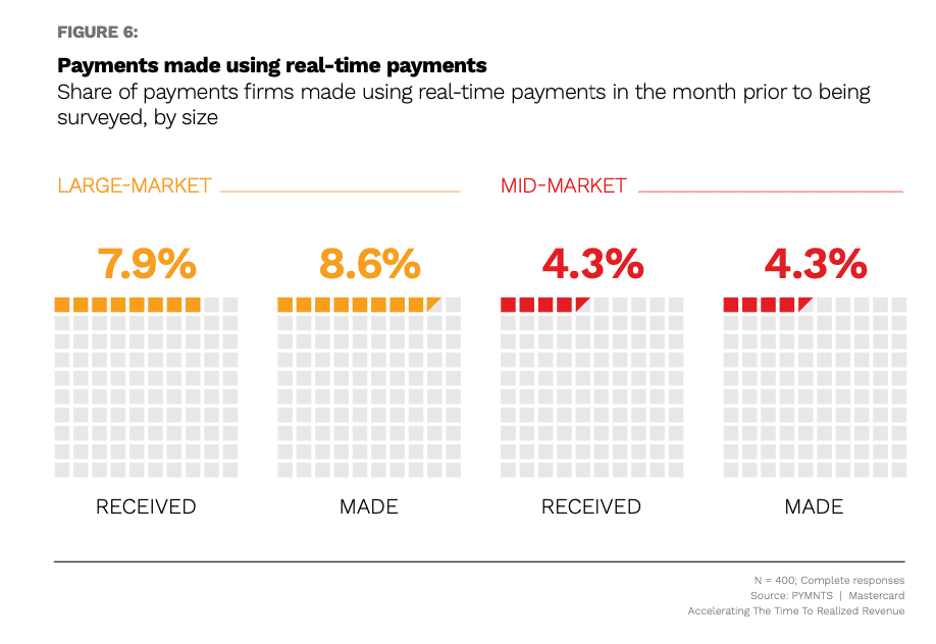

Adoption Trails Behind Larger Competitors

Large-market U.S. firms (those that generate more than $1 billion in annual revenue) use real-time payments to make and receive twice as many business-to-business (B2B) payments as mid-market U.S. firms (which generate between $20 million and $1 billion). On average, large-market businesses use real-time payments in about 8% of the payments received and 9% of the payments made.

By contrast, the average middle-market firm receives 4% and makes 4% of its payments via RTP.

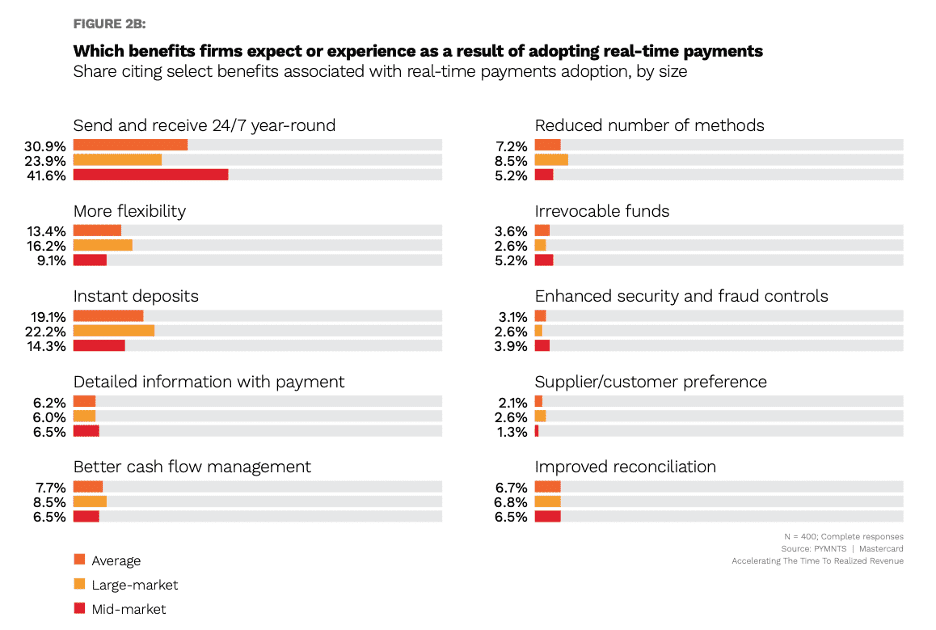

Middle-Market Firms Can reap the Same Benefits as the Bigs

Firms of different sizes get the same benefits from using real-time payments, first and foremost the ability to send and receive payments 24/7 year-round. In fact, this leading value proposition is even more valuable to the U.S. mid-market compared to their larger counterparts, with 42% of of them saying so, compared with 24% of their large-market competitors.

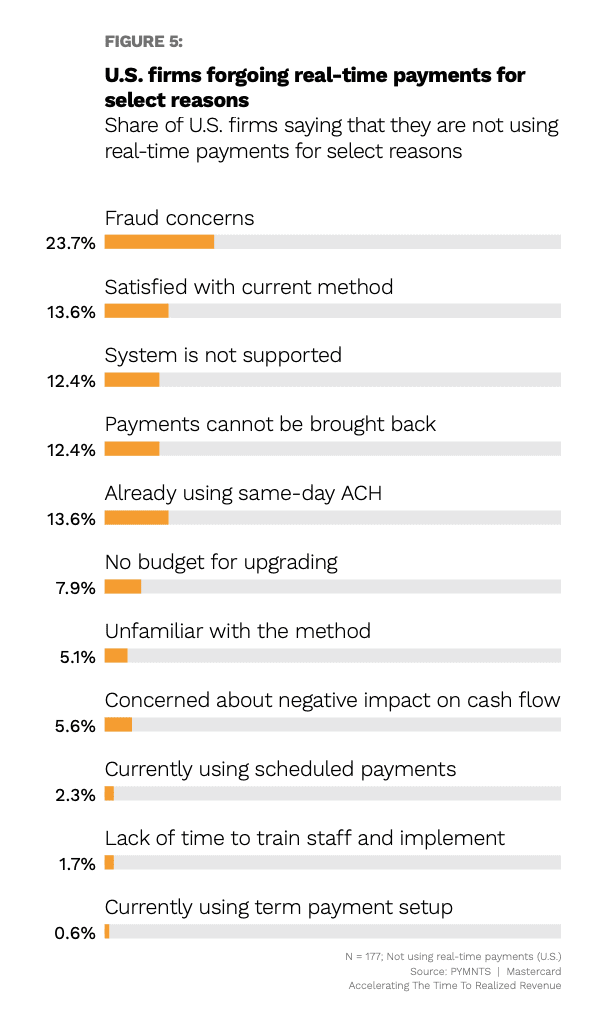

Why Isn’t Adoption Higher?

Many U.S. firms that don’t use RTP are working under the assumption that they might leave them more vulnerable to fraud. This fear is exacerbated by the inarguable fact that such payments are currently irrevocable.

Fact vs Fiction

But businesses that already use them don’t widely share that assumption. According to PYMTS research, real-time payment utilization actually correlates with much lower fraud incidence. It occurs approximately 75% less often among firms that use RTP as it does among those that don’t.

Ready, Aim, Fire — Not Ready, Fire, Aim

The reason for this may be that utilizing real-time payments imposes discipline on the accounts payable function. The irrevocability of this method of payment compared with other methods such as checks, automated clearinghouse, and credit cards is the financial equivalent of working without a net. This focuses the minds of accounts payable (AP) personnel marvelously on rigorously authenticating payee identity.

While regulators are pressuring platforms to address the irrevocability issue, there is no such reform on the horizon. Meanwhile, the watchword must be payor emptor, and they need to bolster internal controls to ensure that appropriate approvals are in place and automated to miminmize payment errors, if not eliminate them completely. This also allows auditing of the entire AP verification process to uncover any legacy issues. The annals of AP are rife with examples of fraudulent payment, regardless of method. RTP adoption represents an opportunity to clean up the entire operation.

Weighing the Fraud Factor

Midmarket firms need to play catch up to avoid ceding competitive advantage with their larger rivals. The benefit equation is a two-sided proposition. While AP streamlining and improved vendor relations are a key part of the value proposition, the accounts receivable (AR) side of the fence holds perhaps even greater benefits. Offering real-time payments to new and existing customers can improve by making customer acquisition and retention easier and improving cash flow — an especially critical imperative given rising costs lately.

The AR side of the operation arguably poses less risk and substantially higher potential rewards for mid-market firms and is perhaps the most urgent competitive arena.

Technology adoption is a two-way street. Receivers can only receive if their senders use RTP, and once payers understand the advantages will increase adoption. Making a “real-time payment” the day the invoice is due is a benefit to the sender — they can wait until the last minute to schedule even though receivers would rather receive real-time and other payments well before the due date.

Despite these complexities, firms testing the waters may want to start there. However, in the current supply chain environment, competitive disadvantages in the purchasing process can also restrict sales growth. And middle-market firms should make a fact-based risk-reward analysis when considering the tradeoffs between adopting and not adopting real-time payments at least on a pilot basis, mindful of the fact that there are risks on each branch of the decision tree.

For all PYMNTS B2B coverage, subscribe to the daily B2B Newsletter.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More