While panning PYMNTS’ weekly stream of research and surveys, an unexpected thread of mistrust, misperception and misuse emerged, involving both consumers and businesses, that wove through a range of seemingly disparate topics.

Whether it’s the cool embrace of fully digital banks, the unavailability of instant payments or wanton cheating within the subscription sector, a distinct “tech disconnect” was revealed that showed the uneven, inconsistent and often inexplicable relationship we have with our increasingly digital, connected world.

It’s a weird confluence to be sure though not unexpected at a time of rampant economic uncertainty, and ample data shows that consumers and businesses alike are still treading lightly in some aspects of their digital transformations, while moving, perhaps, too quickly in others.

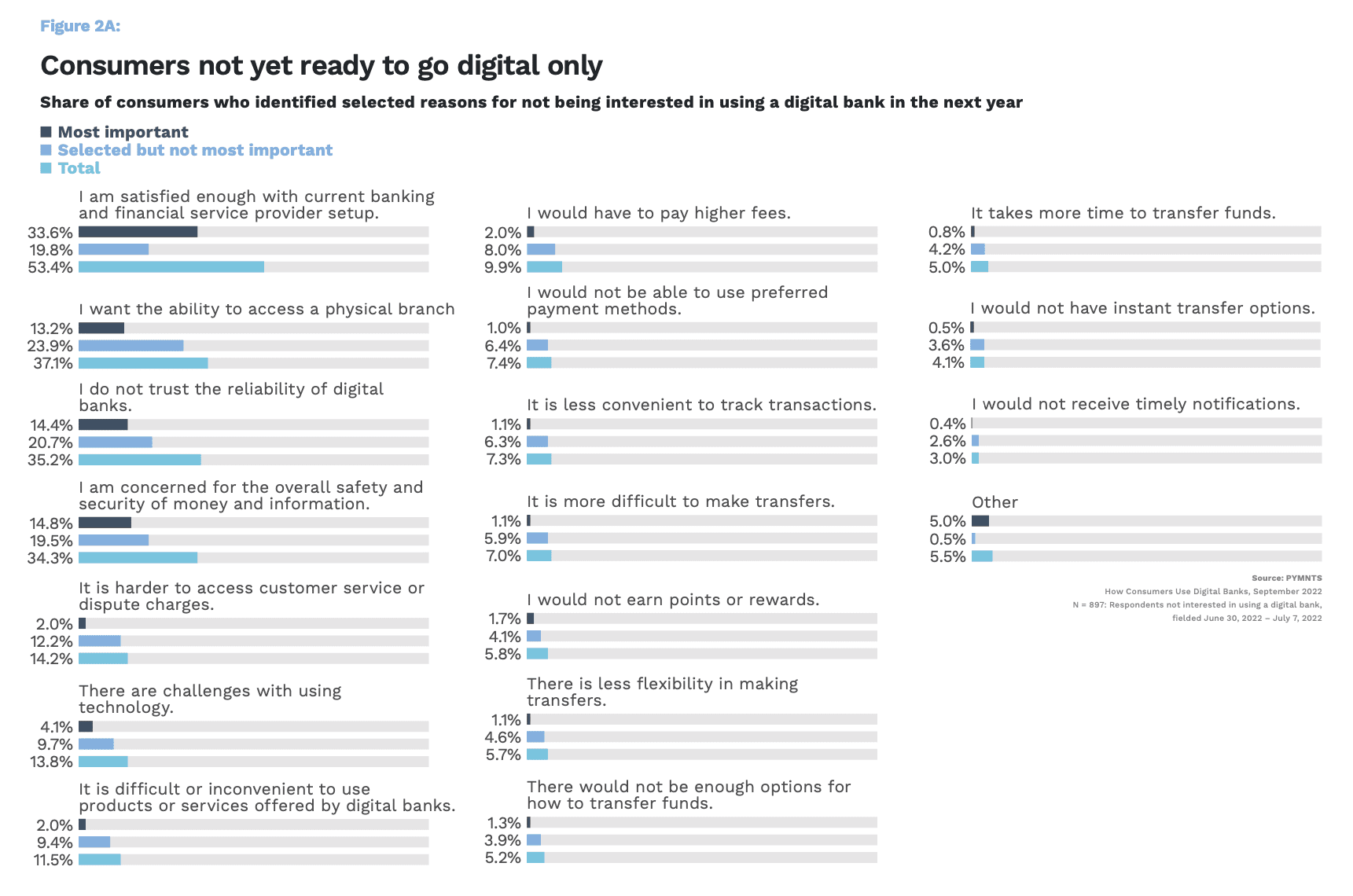

Let’s start with FinTechs and fully-digital online financials, and the study “How Consumers Use Digital Banks,” a PYMNTS and Treasury Prime collaboration, which surveyed over 2,100 U.S. consumers and found that despite growing familiarity — especially among younger demographics — the embrace of fully digital banks is taking the slow road.

To be clear, a “digital bank” is quite different than “digital banking” in that the former is a financial entity — a FinTech — without a physical branch that exists and interacts solely online, while the latter (digital banking) consists of the widely used and loved collection of electronic transactions, payments, mobile wallets etc. that most consumers couldn’t live without.

What was surprising, however, is that PYMNTS data found that while two-thirds of consumers, including 84% of younger customers, already use FinTech banking services in some form, just 9.3% of respondents were comfortable enough to have their primary account with a digital bank. Clearly a massive tech disconnect, and clearly more work to be done to shore-up public trust and confidence.

When Will Real-Time Get Real?

And it’s not just digital banks as this duel perception also appeared in our latest study of real time payments, or RTPs. According to “Real-Time Payments: How Speed Is Changing The Mix Of Business Payments, report” done by PYMNTS and The Clearing House, we saw that large firms were overwhelmingly comfortable with instant payments, had the pipes to handle them, and were also familiar with the benefits they offer, they’re actual usage of RTPs remains remains stubbornly low.

Based on a survey of 100 executives at companies generating over $250 Million in annual revenues that use real-time payments for at least one payment type, the study found that “61% of these firms believed real-time payments offer competitive advantages, with large shares also citing increased accounting efficiency and reduced risk of payment failure as key benefits.”

And then comes the weird part.

“However, real-time payments account for only 8.2% of payments received and 6.4% of payments sent,” the study found with only a slight usage bias in favor or bigger companies.

Businesses with real-time payments capabilities were also more likely to do consumer payouts using these rails than they were to use them for B2B payments, with 12% of payments made to individuals now being done in real-time, versus 8.6% of business-to-business (B2B) sent via this method.

Another mile-wide disparity that points to the huge room for growth and uptake that exists with RTPs, but not the only such oddity we unearthed this week.

Instant Frustrating

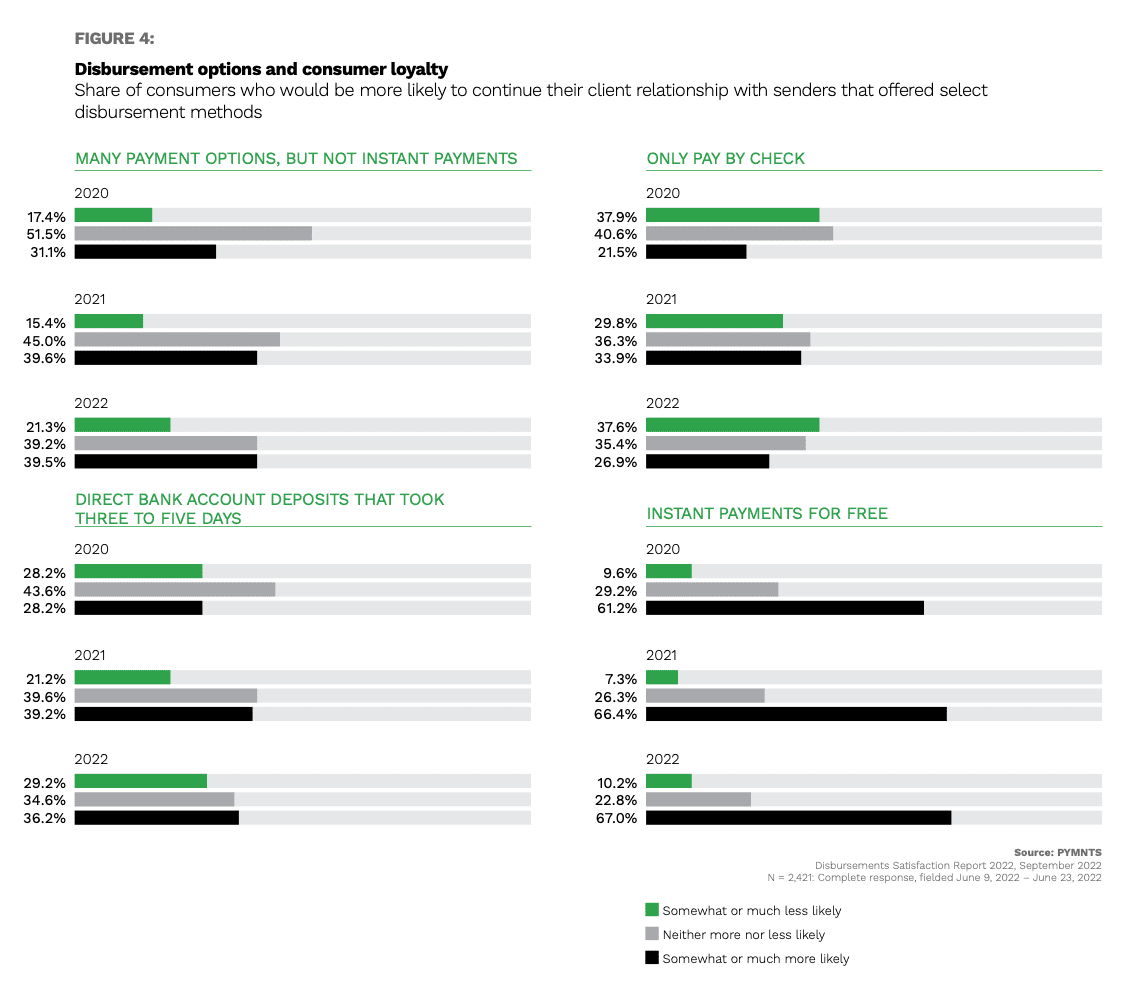

PYMNTS research also uncovered a reluctance on the part of business to use instant payments that was in polar contrast with how their customers said they’d prefer to receive funds. The findings came in the new “Disbursements Satisfaction Report,” a collaboration with Ingo Money that included survey responses from more than 3,600 consumers.

Getting right to the point, the study notes, “Nearly half of U.S. consumers who receive disbursements would choose to receive them via instant payment rails if they could, but many recipients are never given the choice. PYMNTS’ data shows that 17% of the consumers who received disbursements last year received them via instant rails — more than ever before, yet still far less than the share who want to receive them.”

That’s not only a major missed opportunity to bolster loyalty, as the study found that instant disbursements are a loyalty-lock for two-thirds of the survey sample, but is also a flight risk of sorts.

“No other payment option has such a drastic impact on consumers’ willingness to do business with the organizations from which they receive disbursements,” per the study. “Only 36% of consumers would continue a relationship with senders that only offered direct deposits, and only 40% would continue client relations with senders that offered a wide array of payments choice, but not instant.”

Again, a third behavioral chasm was revealed in the same weekly collection of research and analysis.

Cheaters Never Win, but They Do Score

Given this level of uncertainty and mistrust combined with hurricane-force economic headwinds of 2022, it’s not entirely unexpected to find consumers distorting the benefits of tech to cut corners and knowingly cheat the system — as in using subscription services they didn’t pay for.

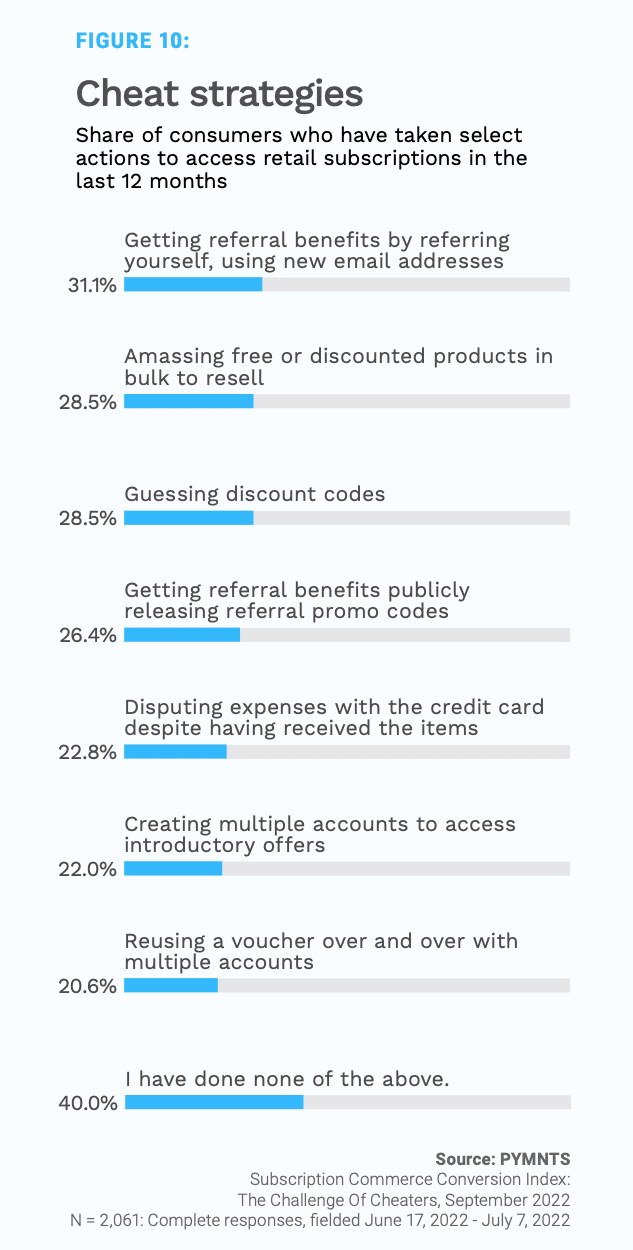

For “The Subscription Commerce Conversion Index: The Challenge Of Cheaters,” a PYMNTS and sticky.io collaboration, we surveyed over 2,000 consumers and found that among the legions of legitimate subscribers driving this form of commerce to record heights, there also exists an alarmingly high degree of illegitimate use and access abusers.

“Elevated inflation and fears of recession are prompting consumers to tighten their belts. One strategy that many are adopting is to ‘cheat’ the subscription game: 60% of subscribers admit to at least occasionally exploiting subscription benefits — such as introductory offers and referral codes — in ways providers do not intend,” the study found. Sixty percent.

Taken together, these four far-flung findings not only express to dichotomy of realities that personal and professional users of technology are still wrangling with, but also serve as a reminder that while much ground has been covered in a relatively short period of time, the embrace and uptake of the ConnectedEconomy is still quite new, with countless gains, pains and adjustments still to come.